All Activity

- Past hour

-

Related: Is a squarish or narrow layout better for an office unit What key factors should I consider Does this also apply to homes - Feng Shui for Business - FengShui.Geomancy.Net

-

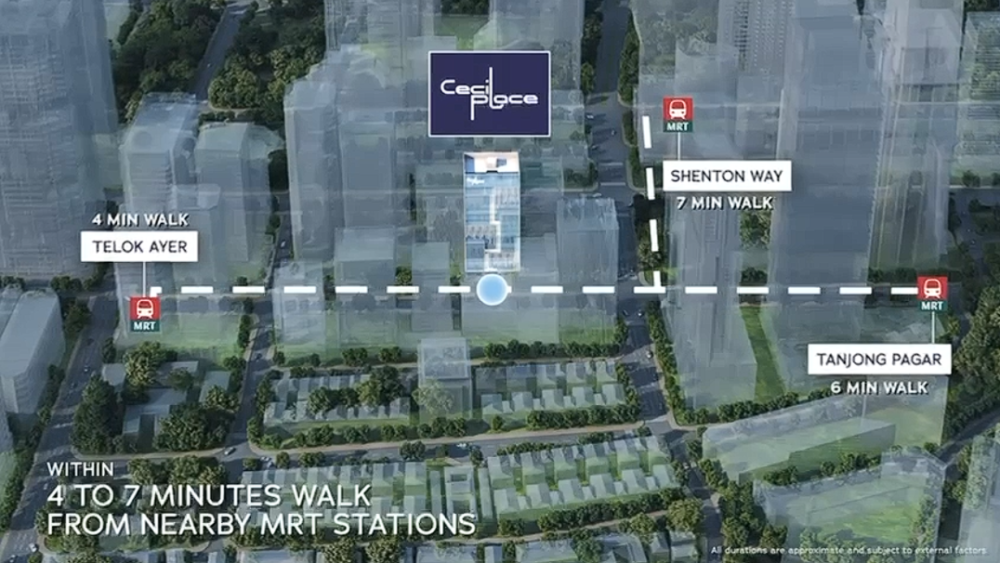

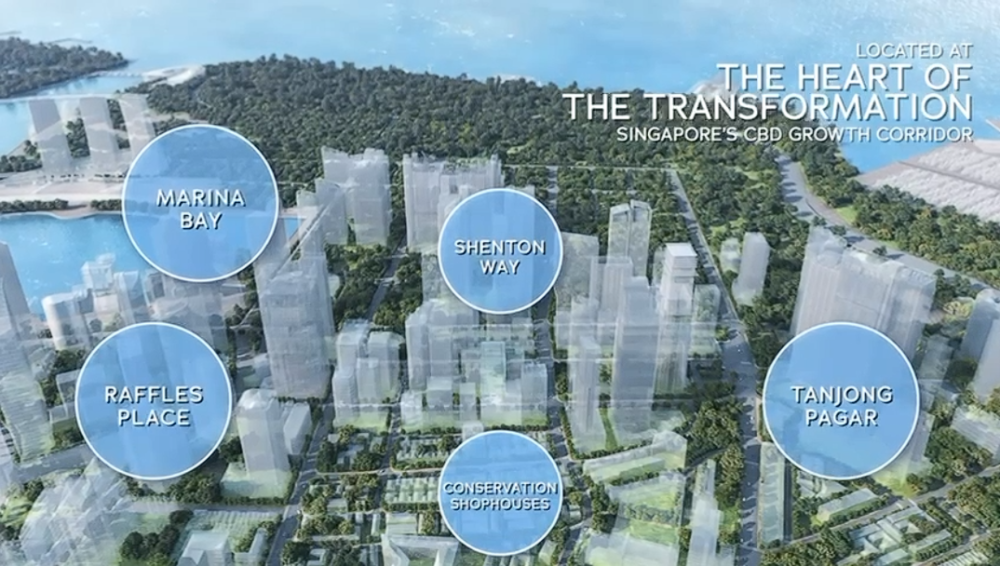

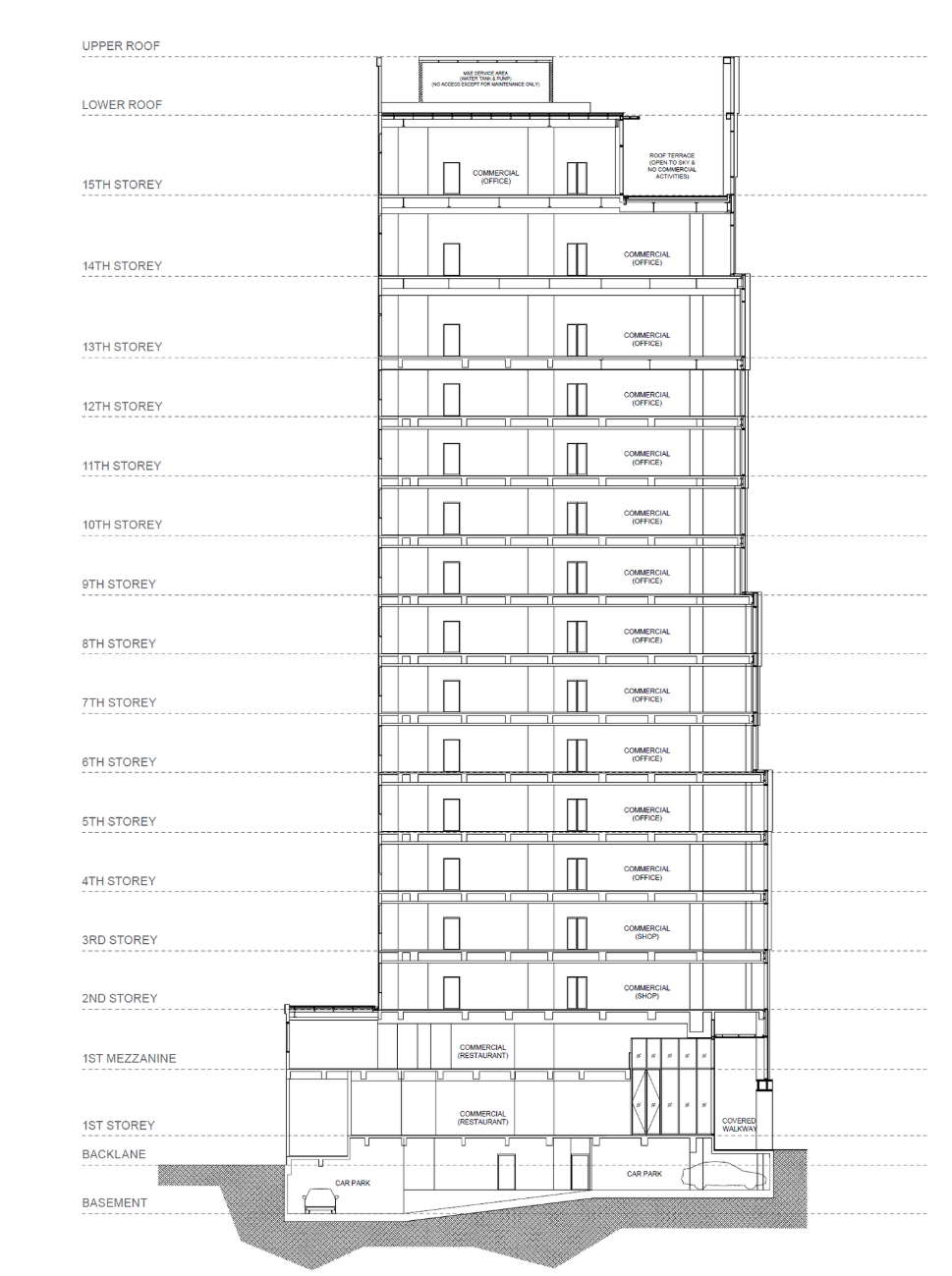

CECIL PLACECECIL PLACE is a Freehold development located at 137 Cecil Street in D01 - Boat Quay / Raffles Place of Singapore. The development is brought to you by Cecil Pte Ltd. CECIL PLACE comprises a total of 30 units. CECIL PLACE is targeted to be completed in 30/03/2027

- Today

HDB Lease Decay By 2030, close to 500,000 HDB flats will be older than 40 years. That means about 40% of all HDB flats will be reaching an age where “lease decay” becomes a bigger concern i.e., the remaining lease is shorter, which can reduce the flat’s value, make financing harder, and affect resale demand. What this means If you’re an existing owner (especially if your flat is already 30+ years old) - Track remaining lease, not just flat age. The key issue is how many years are left on the lease relative to your timeline (retirement, selling, upgrading). - Plan earlier for exit options. Older flats can take longer to sell and may face price pressure; consider whether you intend to hold long-term or sell while demand/financing is still strong. - Factor in renovation vs. horizon. Big renovation spending is harder to justify if you may sell in a few years or if the flat’s marketability will decline with lease. - Watch policy pathways. Outcomes may include upgrades, redevelopment schemes, or targeted support, but these are not guaranteed for any specific block—avoid planning on redevelopment as a certainty. If you’re buying a resale flat - Do the “remaining lease check” first. Ensure the remaining lease supports: - your intended holding period, and - financing/CPF usage rules (which typically become tighter as remaining lease falls). - Price in lease decay. If you buy older, you should generally expect slower appreciation and potentially sharper depreciation later. - Choose micro-location and attributes carefully. For older flats, fundamentals (near MRT, amenities, good layout, popular town) matter more for resale resilience. If you’re a policymaker / planner (high-level implication) - The statement signals a system-wide aging stock issue, suggesting growing need for coordinated strategies across upgrading, redevelopment, housing options for seniors, and market stability measures. A simple rule of thumb Treat “danger zone” as a risk flag, not a guarantee of loss: the impact depends on remaining lease, location, flat type, and your personal timeline. If you share the flat’s town, flat type, remaining lease, and whether you’re buying or selling (and your timeline), I can give more tailored, scenario-based advice. +++ The Silver Tsunami refers to the aging population. Most of them own their own homes. Most of their children already own homes too. Since they can’t own two HDB flats, their children are expected to sell these flats. This can add extra supply of flats to compete with such flats. +++ Danger zone isn’t an official HDB term, but in practice people use it to mean the point where the remaining lease starts materially restricting buyers, mainly through CPF usage and loan financing, which then pressures resale demand and price. Practical “danger zone” thresholds (remaining lease) 1) ~60 years remaining (common rule-of-thumb danger zone) - Why it matters: a flat that is 40 years old has ~**59 years left** on a 99-year lease, and around this level the market starts worrying about: - smaller future buyer pool - harder/shorter financing - weaker price support over time 2) Below the “covers buyer to age 95” line (CPF/loan constraints kick in) CPF usage is strongly affected by whether the remaining lease can last the youngest buyer to age 95: - If it covers to age 95: generally no CPF restriction (relative to the standard rules). - If it does not cover to age 95: CPF usage is reduced (pro-rated), which can reduce affordability for many buyers. This threshold depends on the buyer’s age, so the same flat can be “safe” for an older buyer but “danger zone” for a younger buyer. 3) < 50 years remaining (higher-risk zone) - Typically sees much tighter buyer affordability (more CPF/loan limitations for many households) and more noticeable resale price pressure. 4) < 20 years remaining (critical zone) - CPF cannot be used for the purchase if the remaining lease is under 20 years (major demand cliff). Simple way to think about it - Market danger zone (broad): around < 60 years remaining - Buyer-specific danger zone (more accurate): when the lease won’t last the youngest buyer to age 95 - **Severe constraints:** < 50 years, and especially < 20 years

Check with you. Is this design acceptable: The overhead beams These beams: Master Cecil Lee: In my view, at least 7 out of 10 Chinese people don’t like overhead beams. And if you have several visitors making unfriendly remarks about it, it’s understandable that someone might feel upset. And also, if you mentioned that your FS master says it’s okay… I really have no choice but to deny that I ever said I was “okay” with it. Honestly, your ceiling is already about 2.5 metres, and beams like that can be quite an eyesore. If they are truly heavy beams… then I’d really pray that the upstairs neighbour—if they ever do major hacking—doesn’t end up bringing down the beam. We definitely don’t want another "Hotel New World" happening in a home (touch-wood). Where if they are actual beams, drop down and hurt someone. +++ The Hotel New World collapse (also known as the Lian Yak Building collapse) was a major structural disaster in Singapore. - When/where: On 15 March 1986, the six‑storey mixed‑use building at 142 Serangoon Road (near Rochor) collapsed suddenly, around midday. - What happened: The building came down almost completely, trapping people in the rubble. The ground floor housed businesses (including a nightclub), and the upper floors were used as a hotel. - Casualties: 33 people died and 17 were injured. - Rescue effort: A large, multi‑agency rescue operation ran for days; several survivors were pulled out from voids in the debris, but many victims were trapped deep inside. - Cause (official finding): Investigations concluded the collapse resulted from fundamental structural design errors—most notably the building was underdesigned for its actual loads because the engineer’s calculations omitted key loads/weight (including the building’s own dead load), leaving the structure with inadequate strength. - Aftermath/impact: The incident led to significant tightening of building design checks, regulatory oversight, and professional accountability, and became a landmark case shaping Singapore’s modern building safety regime. Short timeline — rescue and investigation (Hotel New World / Lian Yak Building collapse) - 15 Mar 1986 (midday) — The six‑storey building at 142 Serangoon Road collapses suddenly, trapping occupants and bystanders. - 15 Mar 1986 (same day) — Singapore Civil Defence Force (then Civil Defence), Police, SAF units, and other agencies begin a large-scale search-and-rescue operation. The site is stabilised; rescuers work in shifts using heavy equipment and hand tools to avoid further collapse. - 15–16 Mar 1986 — Survivors are located and pulled out from pockets within the rubble (voids). The operation continues around the clock, balancing speed with safety. - Following days (late Mar 1986) — The rescue shifts gradually from finding live survivors to recovery, as chances of survival diminish and access remains difficult. - After rescue phase (1986) — A formal inquiry/investigation begins. Authorities and engineers collect design drawings, calculation sheets, material information, and site evidence; they also interview parties involved in the building’s design and construction. - Investigation findings (1986–1987 period) — The inquiry concludes the collapse was due to critical structural design/calculation errors, with the building significantly underdesigned for the loads it had to carry. - Aftermath (late 1980s onward) — Singapore implements tighter checking/approval processes and professional practice safeguards (including stronger requirements around independent design checking and regulatory scrutiny).

Check with you. Is this design acceptable: The overhead beams These beams: Master Cecil Lee: In my view, at least 7 out of 10 Chinese people don’t like overhead beams. And if you have several visitors making unfriendly remarks about it, it’s understandable that someone might feel upset. And also, if you mentioned that your FS master says it’s okay… I really have no choice but to deny that I ever said I was “okay” with it. Honestly, your ceiling is already about 2.5 metres, and beams like that can be quite an eyesore. If they are truly heavy beams… then I’d really pray that the upstairs neighbour—if they ever do major hacking—doesn’t end up bringing down the beam. We definitely don’t want another "Hotel New World" happening in a home (touch-wood). Where if they are actual beams, drop down and hurt someone. +++ The Hotel New World collapse (also known as the Lian Yak Building collapse) was a major structural disaster in Singapore. - When/where: On 15 March 1986, the six‑storey mixed‑use building at 142 Serangoon Road (near Rochor) collapsed suddenly, around midday. - What happened: The building came down almost completely, trapping people in the rubble. The ground floor housed businesses (including a nightclub), and the upper floors were used as a hotel. - Casualties: 33 people died and 17 were injured. - Rescue effort: A large, multi‑agency rescue operation ran for days; several survivors were pulled out from voids in the debris, but many victims were trapped deep inside. - Cause (official finding): Investigations concluded the collapse resulted from fundamental structural design errors—most notably the building was underdesigned for its actual loads because the engineer’s calculations omitted key loads/weight (including the building’s own dead load), leaving the structure with inadequate strength. - Aftermath/impact: The incident led to significant tightening of building design checks, regulatory oversight, and professional accountability, and became a landmark case shaping Singapore’s modern building safety regime. Short timeline — rescue and investigation (Hotel New World / Lian Yak Building collapse) - 15 Mar 1986 (midday) — The six‑storey building at 142 Serangoon Road collapses suddenly, trapping occupants and bystanders. - 15 Mar 1986 (same day) — Singapore Civil Defence Force (then Civil Defence), Police, SAF units, and other agencies begin a large-scale search-and-rescue operation. The site is stabilised; rescuers work in shifts using heavy equipment and hand tools to avoid further collapse. - 15–16 Mar 1986 — Survivors are located and pulled out from pockets within the rubble (voids). The operation continues around the clock, balancing speed with safety. - Following days (late Mar 1986) — The rescue shifts gradually from finding live survivors to recovery, as chances of survival diminish and access remains difficult. - After rescue phase (1986) — A formal inquiry/investigation begins. Authorities and engineers collect design drawings, calculation sheets, material information, and site evidence; they also interview parties involved in the building’s design and construction. - Investigation findings (1986–1987 period) — The inquiry concludes the collapse was due to critical structural design/calculation errors, with the building significantly underdesigned for the loads it had to carry. - Aftermath (late 1980s onward) — Singapore implements tighter checking/approval processes and professional practice safeguards (including stronger requirements around independent design checking and regulatory scrutiny).

AD

AD

- Yesterday

ADs

Villas @ Greenbank Park Villas @ Greenbank Park is a freehold development located at 50 and 52 Greenbank Park (semi-detached) and 54 Greenbank Park (bungalow) in District 21, Clementi / Upper Bukit Timah, Singapore. The development is by Tong Eng Brothers Pte Ltd. Villas @ Greenbank Park has a total of 3 units. Villas @ Greenbank Park is planned to be completed on 30/03/2026.

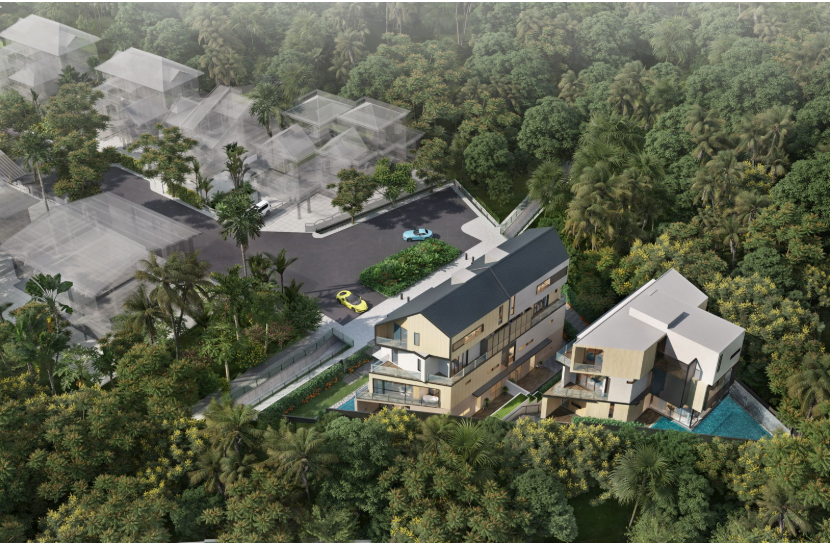

Villas @ Greenbank Park Villas @ Greenbank Park is a freehold development located at 50 and 52 Greenbank Park (semi-detached) and 54 Greenbank Park (bungalow) in District 21, Clementi / Upper Bukit Timah, Singapore. The development is by Tong Eng Brothers Pte Ltd. Villas @ Greenbank Park has a total of 3 units. Villas @ Greenbank Park is planned to be completed on 30/03/2026. District 27 - Sembawang / Yishun 1 Villa Bungalow & 10 Semi-detached homes Vila Natura Vila Natura is a freehold development located at 20 Tung Po Avenue in District 27 - Sembawang / Yishun of Singapore. The development is by Aurum Gravis. Vila Natura has a total of 11 units. Vila Natura is expected to be completed on 30/01/2029.

District 27 - Sembawang / Yishun 1 Villa Bungalow & 10 Semi-detached homes Vila Natura Vila Natura is a freehold development located at 20 Tung Po Avenue in District 27 - Sembawang / Yishun of Singapore. The development is by Aurum Gravis. Vila Natura has a total of 11 units. Vila Natura is expected to be completed on 30/01/2029.

Source & Credit Costly legal fight for woman who listed daughter as joint owner of 26 properties

Source & Credit Costly legal fight for woman who listed daughter as joint owner of 26 properties On 31st March 2026

On 31st March 2026

- Last week

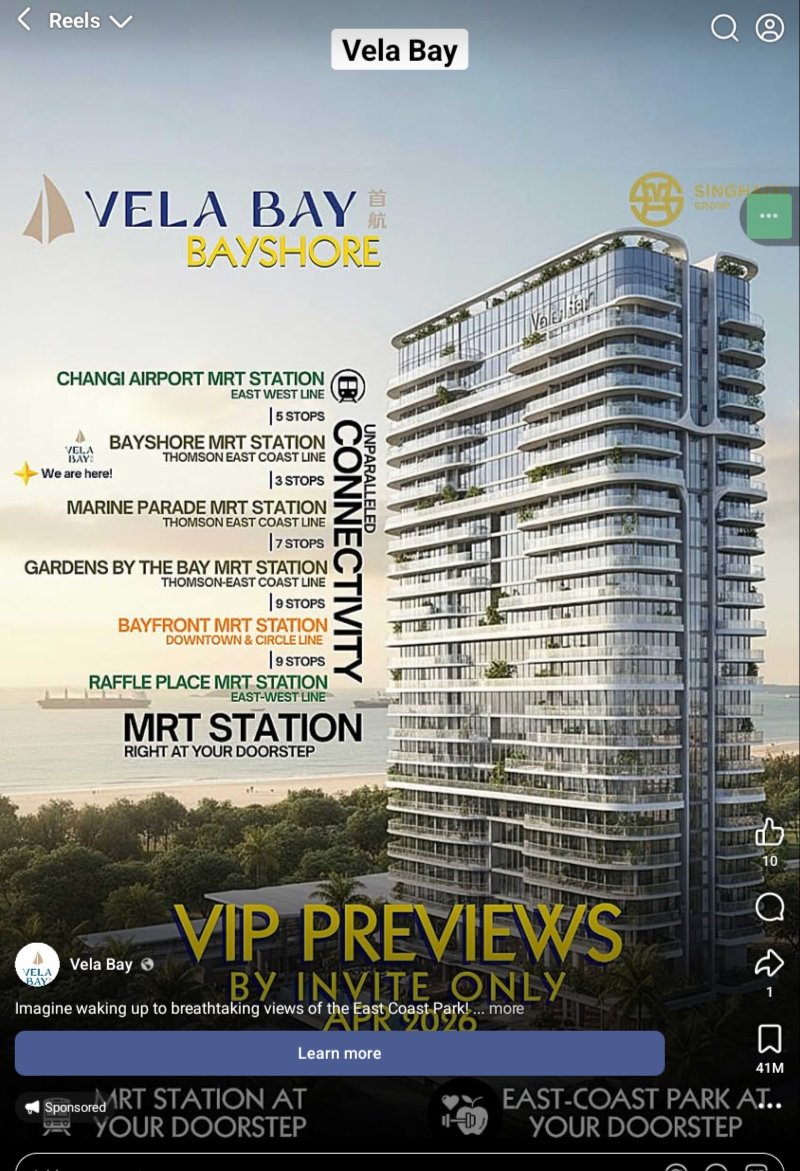

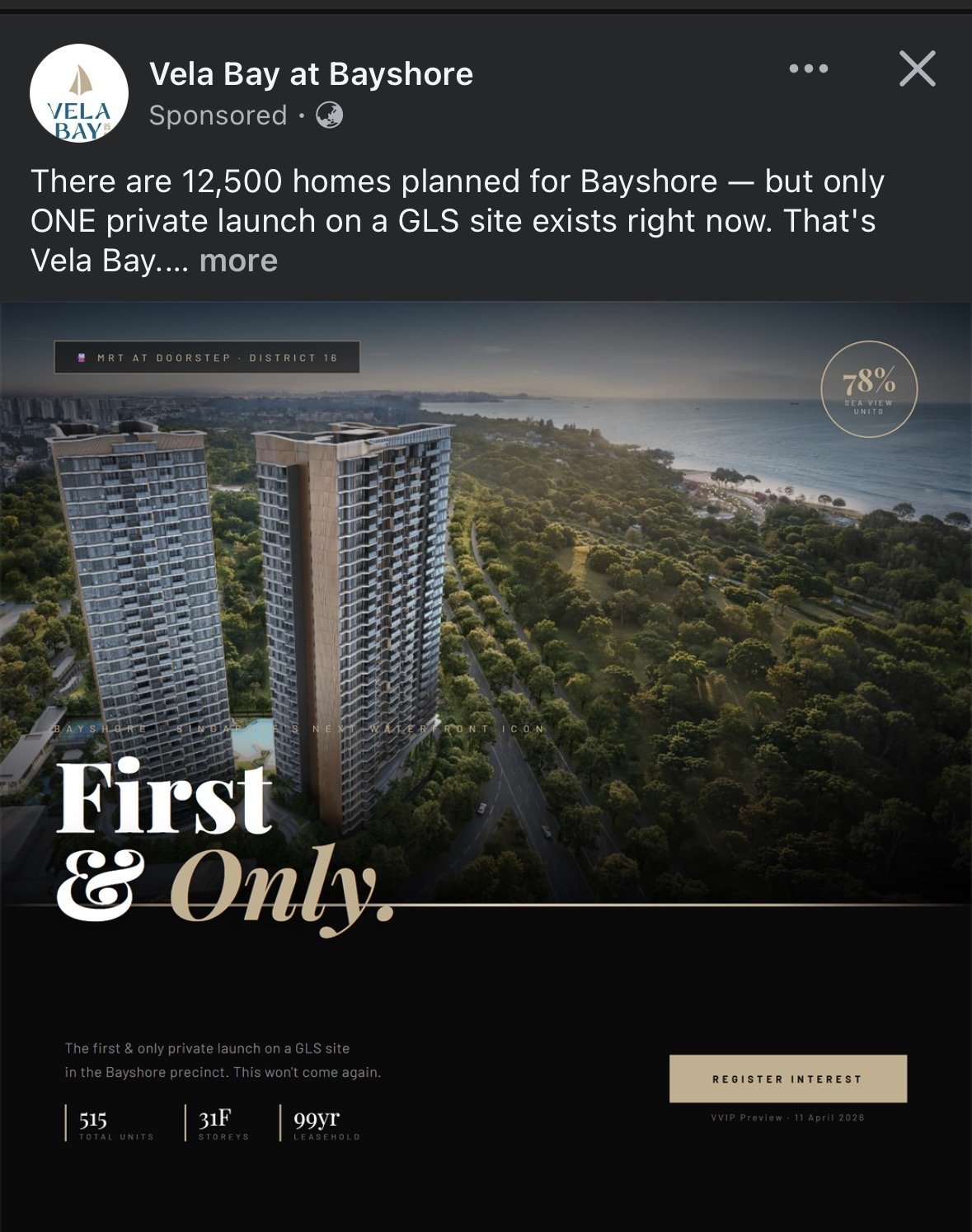

First and only? Ally joined the communitySales ad in 2026 showing a similar design where privacy windows are on the lower part of the windows. Above them are sliding window panels.

Ally joined the communitySales ad in 2026 showing a similar design where privacy windows are on the lower part of the windows. Above them are sliding window panels.

My Salah Mat joined the communityAN EXAMINATION OF WHICH FLYING STAR PERIOD ONE SHOULD UTILIZE? +++ Which Flying Star Period to Use? For example, take a look at Treasure @ Tampines The transition of Feng Shui Qi is significant in the context of the Chinese New Year 2024, as it influences the energy dynamics within a space. The timing of when a unit is first occupied plays a crucial role in determining its Flying Star Feng Shui. This means that the specific day of occupancy will affect the energetic quality and overall Feng Shui of the unit, highlighting the importance of timing in Feng Shui practices. Understanding these elements can help individuals optimize their living environments in alignment with the changing energies associated with the New Year. +++ When did the first owner/resident/tenant take residence in the unit at Treasure @ Tampines? +++ EITHER Can be the owner, resident or a tenant OR Can be the owner, resident or a tenant REGARDLESS, UNITS FACING NORTH POSSESS A POSITIVE FENG SHUI OVERALL How do you Feng Shui your home? Use your front door? Who are the Conservatives & the Modernist? +++ Cecil Lee, Geomancy.net

My Salah Mat joined the communityAN EXAMINATION OF WHICH FLYING STAR PERIOD ONE SHOULD UTILIZE? +++ Which Flying Star Period to Use? For example, take a look at Treasure @ Tampines The transition of Feng Shui Qi is significant in the context of the Chinese New Year 2024, as it influences the energy dynamics within a space. The timing of when a unit is first occupied plays a crucial role in determining its Flying Star Feng Shui. This means that the specific day of occupancy will affect the energetic quality and overall Feng Shui of the unit, highlighting the importance of timing in Feng Shui practices. Understanding these elements can help individuals optimize their living environments in alignment with the changing energies associated with the New Year. +++ When did the first owner/resident/tenant take residence in the unit at Treasure @ Tampines? +++ EITHER Can be the owner, resident or a tenant OR Can be the owner, resident or a tenant REGARDLESS, UNITS FACING NORTH POSSESS A POSITIVE FENG SHUI OVERALL How do you Feng Shui your home? Use your front door? Who are the Conservatives & the Modernist? +++ Cecil Lee, Geomancy.net

Flying Star Feng Shui Workings

Flying Star Feng Shui Workings IRAS does not really offer broad “safe harbors” for ABSD/tax planning in property transactions (e.g., “this structure is always acceptable”). Instead, IRAS provides rule-based guidance (what duty applies, and when specific reliefs/remissions are available) and then applies a facts-and-substance approach for anything more bespoke. What IRAS guidance does function like “safe harbor” These are the closest equivalents—because they are expressly provided for and typically workable if you meet the stated conditions and can evidence them: 1. Published ABSD/BSD rules + examples - IRAS guides/FAQs on ABSD/BSD (rates, buyer profile, counting properties, how to treat joint buyers, etc.). - If your facts clearly fit, paying duty accordingly is “acceptable planning” (it’s just compliance). 2. Specific reliefs/remissions with clear conditions Examples (depending on your situation) include: - ABSD remission/refund schemes that IRAS lists with eligibility criteria and deadlines. - Matrimonial-related transfers where stamp duty treatment depends on meeting conditions (e.g., pursuant to a qualifying court order/settlement framework). - Housing Developer ABSD remission regimes (highly condition-driven). These are “safe” only to the extent you truly satisfy the conditions and keep proof. 3. IRAS e-Stamping / duty assessment processes - Using e-Stamping tools and paying based on accurate, complete facts is the baseline. - Where unclear, IRAS has processes to determine duty based on submitted documents (see next section). How to get certainty if your plan is not clearly covered 1. Ask IRAS for a view / submit for adjudication (case-by-case) - If the structure is unusual (trusts, complex co-ownership changes, multi-step arrangements), the practical route is to write in/submit documents for IRAS to determine the stamp duty outcome. - This is the closest way to “pre-clear” a grey area for stamp duties. 2. Document substance IRAS commonly tests: - Beneficial ownership (who funds, controls, benefits, bears risk) - Consistency across OTP/SPA, loan docs, bank flows, occupancy/rental arrangements - Absence of side agreements contradicting the legal paperwork Having clean, contemporaneous evidence is what keeps “planning” on the acceptable side. 3. If something was done wrongly: voluntary disclosure early - If there’s already an error/underpayment, approaching IRAS early under its voluntary disclosure approach can reduce enforcement pain versus waiting for an audit. Practical takeaway - Acceptable tax planning in this space usually means: pick a transaction path that is real, truthful, and explicitly contemplated by IRAS guidance (including remissions you genuinely qualify for), and ensure beneficial ownership matches the documents.- There’s no “magic structure safe harbor” if the main purpose is to avoid ABSD while the real buyer/beneficiary is someone else.IRAS generally draws the line by looking past the paperwork to the economic reality of the transaction—i.e., who truly owns, controls, funds, benefits from, and bears the risks of the property—and whether the steps taken have a genuine purpose beyond reducing ABSD. How IRAS typically assesses “legitimate planning” vs “evasion/avoidance” 1) Substance over form (beneficial ownership) - Legitimate: The legal buyer is also the real buyer (pays, services the loan, takes the upside/downside, receives rent, decides on sale). - Problematic: A “named buyer” is used, but someone else is the real beneficial owner (e.g., nominee/straw-buyer setups). 2) Commercial / personal rationale beyond tax - Legitimate: There’s a coherent non-tax reason (e.g., genuine estate planning, real asset-allocation between spouses aligned with contributions, genuine business use via an entity). - Problematic: Steps look unnecessary or circular except to change ABSD outcome (e.g., momentary transfers, artificial sequencing, contrived partitions of ownership). 3) Consistency of documents, conduct, and cashflows IRAS will compare: - Contracts (OTP/SPA), loan documents, declarations, trust deeds (if any) - Bank transfers, source of funds, repayment history - Who occupies the property / collects rent / pays expenses - Any side letters or “private understandings” - Legitimate: Everything aligns cleanly. - **Evasion indicator:** False declarations, hidden side agreements, misstated consideration, or conduct that contradicts the documents. 4) Reality of risk and control - Legitimate: The stated owner bears real risk (market risk, default risk) and has genuine control (can sell/lease without being a puppet). - Problematic: The “owner” is insulated while another party effectively controls and benefits—suggesting the structure is a facade. 5) Artificiality and timing - Legitimate: Timing follows genuine life/market events (upgrade after sale, relocation, family needs). - Problematic: Back-to-back steps, “paper” changes, or rapid sequences that look engineered solely to fit ABSD thresholds. A practical rule of thumb - Tax planning: choosing among real, legally and factually true options that Parliament/IRAS clearly contemplates (including using available remissions when you genuinely meet conditions). - Evasion: reducing duty through misrepresentation, concealment, sham documents, or nominee arrangements. - Avoidance (in practice): arrangements that may be formally compliant on paper but are contrived so the main effect is to defeat ABSD’s intent; IRAS may counteract by assessing based on the true buyer/true consideration.IRAS scrutiny usually centers on arrangements whose main (or dominant) purpose appears to be reducing/avoiding stamp duties—especially ABSD—without a genuine commercial reason. Common “creative” patterns include: 1. Nominee / straw-buyer purchases - Buying in another person’s name (e.g., a relative/friend) while the real buyer funds the purchase and enjoys the benefits. - Scrutiny triggers: who paid, side agreements, who occupies/collects rent, who bears risks. 2. Trust or “bare trust” claims used to re-characterize ownership - Declaring someone holds the property “on trust” to argue duties should apply differently (or later transfers are “not really transfers”). - Scrutiny triggers: timing of trust documents, consistency with financing, contemporaneous evidence. 3. Artificial “gift” or below-market transfers - Transfers between family members at undervalue (or labelled as gifts) to reduce duties or facilitate later restructuring. - Scrutiny triggers: valuation vs consideration, hidden consideration, loan write-offs, circular payments. 4. Decoupling / part-share transfers with no real change in beneficial ownership - One spouse transfers a share to the other so that one party can “reset” property count and buy another without ABSD (or at a lower rate). - Scrutiny triggers: rapid sequencing, continued joint control/benefit, funding and reimbursements. 5. Back-to-back / “simultaneous” transactions engineered to change duty outcomes - Closings timed or structured so a buyer “disposes” right before buying to claim a lower ABSD profile, with arrangements effectively locking in both transactions. - Scrutiny triggers: linked contracts, conditionality, pre-arranged counterparties, financing tied across deals. 6. Use of entities (companies/holding vehicles) primarily to avoid buyer-profile duties - Purchasing via a company or interposing entities to achieve a preferred duty treatment (noting entities can also attract ABSD (Housing Developers) or other duty consequences). - Scrutiny triggers: lack of business purpose, thin capitalization, entity created solely for the purchase. 7. Side agreements that contradict the legal paperwork - Private letters/agreements that shift real ownership/economic benefits while the formal documents show something else. - Scrutiny triggers: inconsistencies across OTP/SPA/loan documents vs actual conduct and cashflows. 8. Sham separation/divorce or “paper” arrangements to reallocate ownership - Using personal status changes or agreements primarily to move assets and alter stamp duty outcomes without a genuine underlying arrangement. - Scrutiny triggers: surrounding facts, timing, continued cohabitation/benefit, financial flows. 9. Misstating consideration or “bundling” movable items to depress property value - Inflating the value of furniture/chattels (or other non-dutiable items) to reduce the dutiable consideration attributed to the property. - Scrutiny triggers: unrealistic allocations vs market norms, lack of independent valuation support. 10. Option/assignment structures meant to disguise a sub-sale or flip - Assigning options/rights in ways that try to avoid the stamp duty outcome that would apply to a straightforward purchase/sub-sale. - Scrutiny triggers: who truly controls the right, economic substance, linked payments. General rule of thumb: IRAS looks beyond labels to beneficial ownership, commercial substance, and real cashflows. If a structure mainly exists to change stamp duty results (and especially if it relies on nominees, side letters, or artificial sequencing), it’s more likely to be challenged.Facts of this case A costly lawsuit over a failed “99-1” property ownership arrangement underscores that attempts to circumvent Singapore’s ABSD face heightened IRAS scrutiny, making strict compliance, responsible professional advice, and verified legal/tax guidance essential to avoid severe financial and legal consequences. A RED FLAG +++ Key Takeaways - “99-1” and similar structures aimed at avoiding ABSD are increasingly treated as tax avoidance, not a “gray area.” - Non-compliance can trigger major losses, including expensive litigation (S$731,212 in this case). - Advisors (agents/lawyers) have a duty to prioritize clients’ long-term interests and clearly disclose risks. - Property strategies should be validated with independent legal and tax advice, not just sales assurances. - Deals that appear to offer easy savings warrant extra scrutiny and multiple opinions. - Integrity and transparency are framed as the safest foundation for sustainable real estate decisions. - Authorities’ tougher enforcement raises the cost-benefit risk of “creative” structuring versus full compliance. +++ Source & Credit: ABSD is a form of stamp duty administered by IRAS under the Stamp Duties Act, so “ABSD non‑compliance” is typically dealt with through (i) recovery of the duty shortfall and (ii) statutory penalties, and in more serious cases (iii) criminal enforcement. 1) IRAS can re-characterize the deal and raise an assessment If IRAS finds the arrangement does not reflect the true beneficial owner (or is otherwise an avoidance arrangement), IRAS may: - Disregard the form of the structure and assess ABSD based on the actual purchaser/beneficial owner. - Issue a Notice of Assessment for the ABSD shortfall (often together with any other stamp duty shortfall, e.g., BSD, if relevant). 2) You can be required to pay the ABSD shortfall plus penalties A) Penalties for late stamping / late payment (common) Stamp duty is generally due within 14 days of signing (if signed in Singapore) or 30 days (if signed overseas). If unpaid by the deadline, IRAS can impose a late payment penalty. The commonly applied statutory framework is: - Up to 3 months late: penalty of S$10 or the amount of duty, whichever is higher - More than 3 months late: penalty of S$25 or 4× the amount of duty, whichever is higher B) Penalties for insufficient duty / under-declaration If ABSD was underpaid because the arrangement/documentation understated the true dutiable position, IRAS can require: - Payment of the duty shortfall, and - A further civil penalty (in serious cases, stamp duty penalties can run up to multiples of the duty, including up to 4× in certain late/penalty situations). (Exact penalty quantum depends on what failed—late stamping, insufficient stamping, false statements, etc., and IRAS’s enforcement approach in the case.) 3) Remissions/refunds can be denied or clawed back If ABSD remission/refund was obtained (or sought) based on conditions that turn out not to be met, IRAS may: - Reject the remission/refund, or - Recover the refunded ABSD, potentially with penalties if the underlying duty position was non-compliant or documents were not properly stamped. 4) Criminal consequences (where there is fraud/false information) Where non-compliance involves false statements, sham documents, intentional evasion, or fraud, IRAS can investigate and refer for prosecution. Depending on the specific offence charged, consequences can include: - Fines (often in the thousands to tens of thousands of dollars), and/or - Imprisonment (for the most serious offences). 5) Practical knock-on consequences (often as painful as the penalties) - Transaction disruption: completion delays while stamping/tax issues are resolved. - Financing/solicitor issues: banks and conveyancing solicitors may halt or reassess the deal if beneficial ownership is unclear. - Civil disputes: lawsuits against agents/lawyers/other parties (like the example you shared), plus legal costs. - Reputational/professional risk: for advisors, potential complaints and disciplinary exposure.

IRAS does not really offer broad “safe harbors” for ABSD/tax planning in property transactions (e.g., “this structure is always acceptable”). Instead, IRAS provides rule-based guidance (what duty applies, and when specific reliefs/remissions are available) and then applies a facts-and-substance approach for anything more bespoke. What IRAS guidance does function like “safe harbor” These are the closest equivalents—because they are expressly provided for and typically workable if you meet the stated conditions and can evidence them: 1. Published ABSD/BSD rules + examples - IRAS guides/FAQs on ABSD/BSD (rates, buyer profile, counting properties, how to treat joint buyers, etc.). - If your facts clearly fit, paying duty accordingly is “acceptable planning” (it’s just compliance). 2. Specific reliefs/remissions with clear conditions Examples (depending on your situation) include: - ABSD remission/refund schemes that IRAS lists with eligibility criteria and deadlines. - Matrimonial-related transfers where stamp duty treatment depends on meeting conditions (e.g., pursuant to a qualifying court order/settlement framework). - Housing Developer ABSD remission regimes (highly condition-driven). These are “safe” only to the extent you truly satisfy the conditions and keep proof. 3. IRAS e-Stamping / duty assessment processes - Using e-Stamping tools and paying based on accurate, complete facts is the baseline. - Where unclear, IRAS has processes to determine duty based on submitted documents (see next section). How to get certainty if your plan is not clearly covered 1. Ask IRAS for a view / submit for adjudication (case-by-case) - If the structure is unusual (trusts, complex co-ownership changes, multi-step arrangements), the practical route is to write in/submit documents for IRAS to determine the stamp duty outcome. - This is the closest way to “pre-clear” a grey area for stamp duties. 2. Document substance IRAS commonly tests: - Beneficial ownership (who funds, controls, benefits, bears risk) - Consistency across OTP/SPA, loan docs, bank flows, occupancy/rental arrangements - Absence of side agreements contradicting the legal paperwork Having clean, contemporaneous evidence is what keeps “planning” on the acceptable side. 3. If something was done wrongly: voluntary disclosure early - If there’s already an error/underpayment, approaching IRAS early under its voluntary disclosure approach can reduce enforcement pain versus waiting for an audit. Practical takeaway - Acceptable tax planning in this space usually means: pick a transaction path that is real, truthful, and explicitly contemplated by IRAS guidance (including remissions you genuinely qualify for), and ensure beneficial ownership matches the documents.- There’s no “magic structure safe harbor” if the main purpose is to avoid ABSD while the real buyer/beneficiary is someone else.IRAS generally draws the line by looking past the paperwork to the economic reality of the transaction—i.e., who truly owns, controls, funds, benefits from, and bears the risks of the property—and whether the steps taken have a genuine purpose beyond reducing ABSD. How IRAS typically assesses “legitimate planning” vs “evasion/avoidance” 1) Substance over form (beneficial ownership) - Legitimate: The legal buyer is also the real buyer (pays, services the loan, takes the upside/downside, receives rent, decides on sale). - Problematic: A “named buyer” is used, but someone else is the real beneficial owner (e.g., nominee/straw-buyer setups). 2) Commercial / personal rationale beyond tax - Legitimate: There’s a coherent non-tax reason (e.g., genuine estate planning, real asset-allocation between spouses aligned with contributions, genuine business use via an entity). - Problematic: Steps look unnecessary or circular except to change ABSD outcome (e.g., momentary transfers, artificial sequencing, contrived partitions of ownership). 3) Consistency of documents, conduct, and cashflows IRAS will compare: - Contracts (OTP/SPA), loan documents, declarations, trust deeds (if any) - Bank transfers, source of funds, repayment history - Who occupies the property / collects rent / pays expenses - Any side letters or “private understandings” - Legitimate: Everything aligns cleanly. - **Evasion indicator:** False declarations, hidden side agreements, misstated consideration, or conduct that contradicts the documents. 4) Reality of risk and control - Legitimate: The stated owner bears real risk (market risk, default risk) and has genuine control (can sell/lease without being a puppet). - Problematic: The “owner” is insulated while another party effectively controls and benefits—suggesting the structure is a facade. 5) Artificiality and timing - Legitimate: Timing follows genuine life/market events (upgrade after sale, relocation, family needs). - Problematic: Back-to-back steps, “paper” changes, or rapid sequences that look engineered solely to fit ABSD thresholds. A practical rule of thumb - Tax planning: choosing among real, legally and factually true options that Parliament/IRAS clearly contemplates (including using available remissions when you genuinely meet conditions). - Evasion: reducing duty through misrepresentation, concealment, sham documents, or nominee arrangements. - Avoidance (in practice): arrangements that may be formally compliant on paper but are contrived so the main effect is to defeat ABSD’s intent; IRAS may counteract by assessing based on the true buyer/true consideration.IRAS scrutiny usually centers on arrangements whose main (or dominant) purpose appears to be reducing/avoiding stamp duties—especially ABSD—without a genuine commercial reason. Common “creative” patterns include: 1. Nominee / straw-buyer purchases - Buying in another person’s name (e.g., a relative/friend) while the real buyer funds the purchase and enjoys the benefits. - Scrutiny triggers: who paid, side agreements, who occupies/collects rent, who bears risks. 2. Trust or “bare trust” claims used to re-characterize ownership - Declaring someone holds the property “on trust” to argue duties should apply differently (or later transfers are “not really transfers”). - Scrutiny triggers: timing of trust documents, consistency with financing, contemporaneous evidence. 3. Artificial “gift” or below-market transfers - Transfers between family members at undervalue (or labelled as gifts) to reduce duties or facilitate later restructuring. - Scrutiny triggers: valuation vs consideration, hidden consideration, loan write-offs, circular payments. 4. Decoupling / part-share transfers with no real change in beneficial ownership - One spouse transfers a share to the other so that one party can “reset” property count and buy another without ABSD (or at a lower rate). - Scrutiny triggers: rapid sequencing, continued joint control/benefit, funding and reimbursements. 5. Back-to-back / “simultaneous” transactions engineered to change duty outcomes - Closings timed or structured so a buyer “disposes” right before buying to claim a lower ABSD profile, with arrangements effectively locking in both transactions. - Scrutiny triggers: linked contracts, conditionality, pre-arranged counterparties, financing tied across deals. 6. Use of entities (companies/holding vehicles) primarily to avoid buyer-profile duties - Purchasing via a company or interposing entities to achieve a preferred duty treatment (noting entities can also attract ABSD (Housing Developers) or other duty consequences). - Scrutiny triggers: lack of business purpose, thin capitalization, entity created solely for the purchase. 7. Side agreements that contradict the legal paperwork - Private letters/agreements that shift real ownership/economic benefits while the formal documents show something else. - Scrutiny triggers: inconsistencies across OTP/SPA/loan documents vs actual conduct and cashflows. 8. Sham separation/divorce or “paper” arrangements to reallocate ownership - Using personal status changes or agreements primarily to move assets and alter stamp duty outcomes without a genuine underlying arrangement. - Scrutiny triggers: surrounding facts, timing, continued cohabitation/benefit, financial flows. 9. Misstating consideration or “bundling” movable items to depress property value - Inflating the value of furniture/chattels (or other non-dutiable items) to reduce the dutiable consideration attributed to the property. - Scrutiny triggers: unrealistic allocations vs market norms, lack of independent valuation support. 10. Option/assignment structures meant to disguise a sub-sale or flip - Assigning options/rights in ways that try to avoid the stamp duty outcome that would apply to a straightforward purchase/sub-sale. - Scrutiny triggers: who truly controls the right, economic substance, linked payments. General rule of thumb: IRAS looks beyond labels to beneficial ownership, commercial substance, and real cashflows. If a structure mainly exists to change stamp duty results (and especially if it relies on nominees, side letters, or artificial sequencing), it’s more likely to be challenged.Facts of this case A costly lawsuit over a failed “99-1” property ownership arrangement underscores that attempts to circumvent Singapore’s ABSD face heightened IRAS scrutiny, making strict compliance, responsible professional advice, and verified legal/tax guidance essential to avoid severe financial and legal consequences. A RED FLAG +++ Key Takeaways - “99-1” and similar structures aimed at avoiding ABSD are increasingly treated as tax avoidance, not a “gray area.” - Non-compliance can trigger major losses, including expensive litigation (S$731,212 in this case). - Advisors (agents/lawyers) have a duty to prioritize clients’ long-term interests and clearly disclose risks. - Property strategies should be validated with independent legal and tax advice, not just sales assurances. - Deals that appear to offer easy savings warrant extra scrutiny and multiple opinions. - Integrity and transparency are framed as the safest foundation for sustainable real estate decisions. - Authorities’ tougher enforcement raises the cost-benefit risk of “creative” structuring versus full compliance. +++ Source & Credit: ABSD is a form of stamp duty administered by IRAS under the Stamp Duties Act, so “ABSD non‑compliance” is typically dealt with through (i) recovery of the duty shortfall and (ii) statutory penalties, and in more serious cases (iii) criminal enforcement. 1) IRAS can re-characterize the deal and raise an assessment If IRAS finds the arrangement does not reflect the true beneficial owner (or is otherwise an avoidance arrangement), IRAS may: - Disregard the form of the structure and assess ABSD based on the actual purchaser/beneficial owner. - Issue a Notice of Assessment for the ABSD shortfall (often together with any other stamp duty shortfall, e.g., BSD, if relevant). 2) You can be required to pay the ABSD shortfall plus penalties A) Penalties for late stamping / late payment (common) Stamp duty is generally due within 14 days of signing (if signed in Singapore) or 30 days (if signed overseas). If unpaid by the deadline, IRAS can impose a late payment penalty. The commonly applied statutory framework is: - Up to 3 months late: penalty of S$10 or the amount of duty, whichever is higher - More than 3 months late: penalty of S$25 or 4× the amount of duty, whichever is higher B) Penalties for insufficient duty / under-declaration If ABSD was underpaid because the arrangement/documentation understated the true dutiable position, IRAS can require: - Payment of the duty shortfall, and - A further civil penalty (in serious cases, stamp duty penalties can run up to multiples of the duty, including up to 4× in certain late/penalty situations). (Exact penalty quantum depends on what failed—late stamping, insufficient stamping, false statements, etc., and IRAS’s enforcement approach in the case.) 3) Remissions/refunds can be denied or clawed back If ABSD remission/refund was obtained (or sought) based on conditions that turn out not to be met, IRAS may: - Reject the remission/refund, or - Recover the refunded ABSD, potentially with penalties if the underlying duty position was non-compliant or documents were not properly stamped. 4) Criminal consequences (where there is fraud/false information) Where non-compliance involves false statements, sham documents, intentional evasion, or fraud, IRAS can investigate and refer for prosecution. Depending on the specific offence charged, consequences can include: - Fines (often in the thousands to tens of thousands of dollars), and/or - Imprisonment (for the most serious offences). 5) Practical knock-on consequences (often as painful as the penalties) - Transaction disruption: completion delays while stamping/tax issues are resolved. - Financing/solicitor issues: banks and conveyancing solicitors may halt or reassess the deal if beneficial ownership is unclear. - Civil disputes: lawsuits against agents/lawyers/other parties (like the example you shared), plus legal costs. - Reputational/professional risk: for advisors, potential complaints and disciplinary exposure.

To be frank, it appears quite tidy, organized, and is regarded positively. In comparison to numerous other corridors, this is already an advantage. Nevertheless, these aspects are deemed superficial and do not consider the location, the terrain, and the orientation of this residence.

To be frank, it appears quite tidy, organized, and is regarded positively. In comparison to numerous other corridors, this is already an advantage. Nevertheless, these aspects are deemed superficial and do not consider the location, the terrain, and the orientation of this residence. KIV for Site Map

KIV for Site Map

Background Picker

Account

Navigation

Search

Configure browser push notifications

Chrome (Android)

- Tap the lock icon next to the address bar.

- Tap Permissions → Notifications.

- Adjust your preference.

Chrome (Desktop)

- Click the padlock icon in the address bar.

- Select Site settings.

- Find Notifications and adjust your preference.

Safari (iOS 16.4+)

- Ensure the site is installed via Add to Home Screen.

- Open Settings App → Notifications.

- Find your app name and adjust your preference.

Safari (macOS)

- Go to Safari → Preferences.

- Click the Websites tab.

- Select Notifications in the sidebar.

- Find this website and adjust your preference.

Edge (Android)

- Tap the lock icon next to the address bar.

- Tap Permissions.

- Find Notifications and adjust your preference.

Edge (Desktop)

- Click the padlock icon in the address bar.

- Click Permissions for this site.

- Find Notifications and adjust your preference.

Firefox (Android)

- Go to Settings → Site permissions.

- Tap Notifications.

- Find this site in the list and adjust your preference.

Firefox (Desktop)

- Open Firefox Settings.

- Search for Notifications.

- Find this site in the list and adjust your preference.