All Activity

- Today

-

Related: https://www.geomancy.net/forums/topic/20899-a-critical-review-of-the-common-unit-selection-framework-made-popular-by-singapore-property-influencers-and-agents/ More: https://www.geomancy.net/forums/topic/20898-a-practical-pro-and-cons-review-of-how-singapore-property-is-often-assessed-and-sometimes-marketed-by-real-estate-agents/ More: https://www.geomancy.net/forums/topic/20897-the-3-main-signs-of-property-change-when-to-step-in-and-buy/

-

Related: https://www.geomancy.net/forums/topic/20899-a-critical-review-of-the-common-unit-selection-framework-made-popular-by-singapore-property-influencers-and-agents/ More: More: https://www.geomancy.net/forums/topic/20897-the-3-main-signs-of-property-change-when-to-step-in-and-buy/

-

Related: More: https://www.geomancy.net/forums/topic/20896-boutique-condos-in-singapore-are-often-ignored-because-most-buyers-focus-on-big-high-unit-projects-but-they-can-offer-strong-long-term-value/ More: https://www.geomancy.net/forums/topic/20897-the-3-main-signs-of-property-change-when-to-step-in-and-buy/

-

Related: More: https://www.geomancy.net/forums/topic/20898-a-practical-pro-and-cons-review-of-how-singapore-property-is-often-assessed-and-sometimes-marketed-by-real-estate-agents/ More: https://www.geomancy.net/forums/topic/20896-boutique-condos-in-singapore-are-often-ignored-because-most-buyers-focus-on-big-high-unit-projects-but-they-can-offer-strong-long-term-value/

-

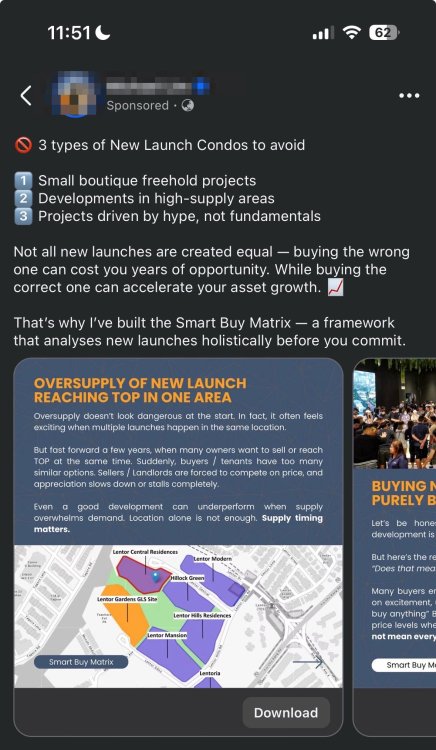

Introduction A critical review of the typical “unit selection framework” popularised by Singapore property influencers/agents (stack selection, facing/floor premiums, launch timing, and exit strategy). I’m not reviewing any one named person but I’ll flag where these frameworks are strong, where they can mislead, and what good practice due diligence looks like in Singapore’s context (ABSD/SSD, URA pipeline, new launch pricing behaviour, etc.). A. The framework itself — what it gets right and what it often misses What these frameworks usually do well (Pros) - Forces structured thinking instead of buying emotionally (“nice showroom” effect). - Translates “homebuyer preferences” into resale liquidity: facing, noise, privacy, layout efficiency do affect buyer pool and rental appeal. - Recognises micro-differentiation in condos where stacks can trade very differently even in the same project. Common weaknesses / blind spots (Cons) - Overweights micro factors (facing/floor) and underweights macro drivers: interest rates, credit rules (TDSR/MSR), policy shocks (ABSD changes), and nearby supply. - Uses selective anecdotes (“this stack always wins”) rather than transaction-level evidence and comparable analysis. - Assumes premiums always come back: paying extra for “best stack” can reduce your future buyer pool (fewer people can afford it) and compress upside. - Agency incentive mismatch: some advice is subtly optimised for “closing at launch” rather than maximising risk-adjusted returns. - Undervalues holding power & cashflow: the best unit on paper can still be a bad buy if your financing, ABSD exposure, or rental buffer is weak. Good practice baseline: treat unit selection as secondary to (1) asset type suitability (OCR/RCR/CCR, freehold/99), (2) total entry price & financing resilience, (3) supply pipeline and exit liquidity. --- 1) Entry Price (Facings | Floor Level) How the “popular discussion” usually frames it - Choose “premium” facings (unblocked, pool view, greenery, away from road/bin centre/substation). - Higher floors = better (view, wind, privacy). - Pay a premium if it’s “rare” because resale buyers will pay too. What’s valid (Pros) - Noise and negative adjacencies are real in Singapore (major roads, MRT tracks, expressways, schools, places of worship, bin centre, loading bay, substation). - Privacy/unblocked view has measurable resale impact, especially for mass-market condos where stacks compete tightly. - Floor premium is usually real up to a point, especially where view corridors matter. Where it goes wrong (Cons / pitfalls) - Premium stacking can become “overpaying”: if you pay a big premium at launch, your resale upside may be capped because future buyers benchmark against nearby alternatives and their affordability ceiling. - High floor isn’t always superior: - Wind, heat, lift reliance, maintenance issues, and “too high” can be less preferred by some families. - “Unblocked” can be temporary if you didn’t verify zoning / future plots. - Facing myths: “south-facing is best” is too simplistic; what matters is afternoon west sun, cross-ventilation, and your specific obstruction/noise context. Good practices (Singapore-specific) - Quantify the premium: compare stack/floor premiums within the same project and against nearby resale/new launches by PSF and absolute price. - Check future obstruction risk using URA Master Plan / zoning and nearby GLS sites, not just current greenery. - Do “negative adjacency mapping”: locate bin centre, guardhouse, function room, tennis court, pools, pump rooms, substation, MSCP ramps—these matter more than many people think. - Benchmark affordability: the best unit is the one your future buyer can still afford. Absolute quantum often constrains demand more than PSF. --- 2) Layout Typical influencer take - “Efficient layout wins” (minimise corridors/bay windows). - Dumbbell layouts for privacy; squarish living/dining; good bedroom sizes. - Avoid weird angles; avoid too much balcony. What’s valid (Pros) - Efficiency drives liveability and valuation: buyers pay for usable area. - Bedroom sizes and storage matter a lot in modern smaller units. - Functional kitchens (enclosed vs open) affect family demand and rental profile. Where it’s often oversimplified (Cons) - “Efficiency” is not universal: some segments value balcony/outdoor space; others want enclosed kitchens due to cooking habits. - Ignoring structural constraints: a “nice-looking plan” can be hard to renovate if many walls are structural, beams intrude, or AC ledge placement is awkward. - Not matching layout to target exit buyer: e.g., dual-key or small 2BR might rent well but have narrower resale demand depending on location/price point. Good practices - Measure real usability: - Can you place a proper sofa/TV wall and dining table without awkward circulation? - Are bedrooms genuinely fit for a queen bed + side tables? - Is there a household shelter (HS) and where is it placed (dead space vs storage)? - Match layout to your exit market: - Near business parks/MRT: compact 1–2BR can be liquid for tenants/investors. - Family-oriented node: 3BR with good bedroom sizes often more resilient. - Avoid “headline traps”: huge balcony counted in strata, long corridors, excessive planter/bay window-like dead spaces (less common now but still appears). --- 3) Demand and Supply Typical discussion - “Near MRT/schools = strong demand.” - “Low supply in the area = price support.” - “Look for transformation stories” (URA plans, new lines, commercial hubs). What’s valid (Pros) - Rental demand is location-led in Singapore (MRT connectivity, employment nodes). - Supply pipeline is crucial because condos compete against nearby substitutes. - Transformation catalysts can work, but only if they convert into real household formation and affordability. Where it can be misleading (Cons) - Demand is not just “interest”; it’s qualified demand (after ABSD/TDSR/MSR and interest rate reality). - Supply analysis is often shallow: people cite “few condos nearby” but ignore: - upcoming GLS sites, - en-bloc potential, - large EC/condo clusters completing around the same period, - unit mix competition (e.g., too many similar 2BRs). - Over-indexing on schools: within 1km matters mainly for certain primary schools and for certain buyer profiles; it may not offset an over-entry price. Good practices (data-driven) - Use URA pipeline and completion schedules (nearby projects TOP-ing within your expected exit window). - Study unit mix supply: if the district is flooded with small 2BRs, your 2BR faces heavier resale competition than a scarce 3BR type (or vice versa). - Check real rental comparables: not just asking rents—look at achieved rents (where possible) and vacancy sensitivity. --- 4) Timing Of Sales (when to buy) Typical influencer playbook - Buy early at launch for “lowest price.” - Look for “star buy” units. - Avoid later phases when developer raises prices. What’s true (Pros) - Developers do often price-in phases based on take-up. - Early phases may offer better unit choice and sometimes better pricing (not guaranteed). - “Star buy” can be real value if it’s not a compromised stack. Key risks and misconceptions (Cons) - Early is not automatically cheaper: some launches are priced aggressively from day 1 due to competition, land price, and recent comparables. - Showflat-driven urgency can cause mispricing decisions. - Macro timing matters more than launch phase: interest rate regime, policy risk, and broader affordability cycle often dominate. Good practices - Anchor to resale comparables: if new launch PSF is far above nearby resale without a strong reason (tenure, MRT proximity, scarcity, product leap), be cautious. - Watch absorption rate and price revisions: strong take-up can justify pricing; weak take-up may bring incentives (but Singapore incentives can be opaque—sometimes via commissions, rebates, or “discounted stacks”). - Consider your holding horizon: if you might need to sell within 3–4 years, you are much more exposed to cycle and SSD constraints. --- 5) How To Time The Exit Typical discussion - Sell at/after TOP when project “matures.” - Sell when nearby new launch pricing sets a higher benchmark. - Avoid SSD period; sell when demand is strong. ### What’s valid (Pros) - SSD is a real constraint and shapes optimal minimum holding periods for private property. - New launch pricing can “pull up” resale benchmarks—sometimes. - Project maturity (livability + transaction history) can widen buyer confidence. Where it’s often incomplete (Cons) - Exit is constrained by your buyer’s financing: even if your unit is “worth” more, buyers may not clear TDSR or may balk at quantum. - “TOP pop” isn’t guaranteed: if many units TOP together (area-wide supply wave), resale competition and rental vacancy can suppress prices. - Ignoring opportunity cost: sometimes the best exit is not “max price” but “best risk-adjusted redeployment,” especially under policy uncertainty or changing family needs. Good practices (practical exit planning) - Pre-plan an exit window (e.g., after SSD, or 1–2 years post-TOP) but validate against: - nearby completions (competition), - interest rate outlook (affects affordability), - your unit’s quantum bracket (mass-market vs high-end behave differently). - Track listing competition within your own project: if many identical stacks are listed, you need price realism. - Maintain optionality: choose units with stronger rental resilience so you can hold longer if the resale market is weak. --- A simple “good unit selection” checklist (robust version) 1) Budget & policy reality: ABSD/SSD exposure, financing buffers, interest-rate stress test. 2) Entry price vs comparables: PSF and absolute quantum vs nearby substitutes. 3) Supply pipeline: URA upcoming completions + GLS/en-bloc risk within 1–3km. 4) Stack fundamentals: noise, privacy, heat (west sun), negative adjacencies, future obstruction risk. 5) Layout usability: furniture test, bedroom practicality, storage/HS placement, reno constraints. 6) Exit buyer clarity: who buys this later (family, upgrader, investor) and can they afford it? --- Here’s a practical, “do-this-then-that” way to apply the good practices for Entry Price (facing/floor) and Layout to a specific new launch condo in Singapore. You can run this like a repeatable workflow and end up with a short, defensible shortlist of stacks. --- 1) What to collect (before you judge any unit) From the developer/agent - Full price list (all stacks + all floors) and unit mix. - Stacking plan, site plan, floor plans (with dimensions if available). - List of facilities, MSCP locations, bin centre, substation (if shown). From public sources - URA Master Plan / zoning (future plots + plot ratio near the project). - URA REALIS / condo transactions for nearby resale benchmarks. - GLS / pipeline: nearby confirmed sites + projects completing around your likely exit window. - OneMap: measure distance to MRT exits, expressways, schools; identify noise sources. --- 2) Entry Price (Facing | Floor Level): turn “premium” into numbers Step A — Build an internal “premium map” within the project Create a simple table (Excel/Sheets) with columns: - Stack / Unit type / Size - Floor - PSF - Absolute price - Facing label (e.g., road/pool/greenery/other block) - Notes (noise/afternoon sun/privacy) Then compute: - Same-stack floor premium: PSF difference between low/mid/high floors. - Same-floor stack premium: PSF difference across stacks on the same level. Decision rule (practical): - Prefer stacks where you’re not paying an outlier premium for a “nice” facing unless it’s genuinely scarce (e.g., only 1–2 stacks have unblocked view AND obstruction risk is low). Step B — Check “unblocked” is real (and stays real) For any stack marketed as “unblocked/greenery”: - Check the adjacent land parcel zoning + plot ratio (URA Master Plan). - Look for reserve sites / GLS nearby. - If it’s facing “landed,” don’t assume permanent—confirm zoning (landed-only vs can intensify). Decision rule: - If the view premium is large but future obstruction is plausible, treat that premium as at-risk (don’t pay full “unblocked” price). Step C — Do negative-adjacency mapping (often the biggest hidden driver) On the site plan + stacking plan, mark stacks that are close to: - Bin centre / M&E rooms / substation - Guardhouse, drop-off, loading bay - MSCP ramps, driveway - Facilities that create noise (courts, pools, function rooms) Decision rule: - All else equal, avoid these unless priced at a clear discount you believe will also be recognised at resale. Step D — “Quantum realism” test (exit affordability) Even if PSF is ok, your exit is limited by absolute price. - Compare the unit’s absolute quantum to nearby resale alternatives (same bed count). - Ask: “Who is the next buyer at $X? How many can afford $X under today’s TDSR-ish reality?” Decision rule: - Don’t stretch into a quantum bracket where your buyer pool thins sharply (this is where “best stack” can become illiquid later). --- 3) Layout: run a fast “furniture + usability” audit (not just aesthetics) Step A — Do a 10-minute furniture fit test (per shortlisted unit) On the floor plan, confirm these can fit without awkward circulation: - Living: proper sofa + TV wall and walkway that isn’t squeezed - Dining: table size appropriate to buyer segment (2BR vs 3BR family) - Bedrooms: can fit a queen bed + side tables, not just a queen outline - Kitchen: workable counter run, fridge position, cooking ventilation practicality - Storage: household shelter placement (usable vs creating dead corners) Decision rule: - Reject layouts that “look efficient” but fail basic furnishing (especially living/dining pinch points and undersized bedrooms). Step B — Identify “paid area that doesn’t live well” Flag: - Oversized balcony (especially if it steals living space) - Long corridors / weird angles - AC ledge / planter-like dead zones - Bathroom doors opening into tight walkways Decision rule: - If 2 units are similarly priced, choose the one with more usable internal area, not more “headline” area. Step C — Match layout to your exit buyer (this avoids false positives) Define likely exit buyer: - Near MRT / business node: tenants + investors → efficient 1–2BR, good privacy, easy maintenance - Family node: owner-occupiers → 3BR practicality, storage, kitchen usability, real bedroom sizes Decision rule: - A “great” layout is only great if it fits the dominant buyer pool at that location and price. --- 4) Put it together: a simple scoring model (so you can decide confidently) Create a 100-point scorecard for each candidate unit: Entry Price (50 points) - (20) Not an outlier premium vs same-type stacks - (10) Low obstruction risk (future development check) - (10) Low negative adjacency exposure - (10) Quantum affordability vs nearby alternatives Layout (50 points) - (20) Living/dining usability (furniture fit) - (15) Bedroom sizes/practicality - (10) Kitchen + storage functionality - (5) Renovation friendliness (less odd angles/dead corridors) 1) Get the official zoning / plot ratio around the condo (URA Space) 1. Go to URA SPACE: https://www.ura.gov.sg/maps 2. Search the condo name or address in the search bar. 3. Turn on these layers (names may vary slightly): - Master Plan 2019 (Land Use / Zoning) - Development Control / Intensity (look for Plot Ratio or Gross Plot Ratio) - Conservation / Special Control (if relevant) 4. Click on the adjacent land parcels (the lots in front of the stacks you care about). A panel will show: - Zoning (e.g., Residential, Commercial, White, Open Space, Reserve Site) - Plot ratio (e.g., 1.4 / 2.8 / 3.5 etc.) - Sometimes height controls or special notes (area-specific) How to interpret quickly - Higher plot ratio nearby = higher chance of a taller building later, hence your “unblocked” view is at risk. - “Reserve Site” / “White” / “Commercial” in front of you is a bigger obstruction risk than “Park / Waterbody / Road”. - Landed zoning is safer for view only if the zoning is truly low-rise and not earmarked for intensification. 2) Cross-check what’s already coming (GLS / pipeline) Even if the Master Plan allows something, you want to know if it’s likely soon. - URA GLS site list (Government Land Sales): https://www.ura.gov.sg/Corporate/Land-Sales Check if any nearby sites are Confirmed (more imminent) vs Reserve. - Look for nearby sites with: - High plot ratio - Large site area - “Residential” / “Residential with Commercial at 1st storey” / “White” 3) Use the condo’s stack orientation to decide which parcels matter From your stacking plan, note: - Which stacks face north/east/south/west - The line of sight from your unit (what’s directly in front vs diagonal) Then, on URA Space, prioritize parcels: - Directly in front within ~100–400m (most likely to block) - Any large plots (redevelopment candidates) even if a bit farther 4) A simple “obstruction risk rating” you can apply For each shortlisted stack, rate what’s in front: - Low risk: park/green buffer/road/waterbody + no reserve/GLS nearby - Medium risk: existing low-rise but zoning/plot ratio allows mid-rise later - High risk: reserve site / GLS / commercial-white / high plot ratio parcel likely to redevelop This topic has nothing to do with Feng Shui. I am also not a Real Estate agent. I am simply, just like you, a property buyer who is interested in property trends in SG.

-

Another Practical Framework to Evaluate Singapore Condos: Pros, Cons, and What People Often Miss Singapore property discussions often revolve around a familiar checklist: Entry Price, Resale Comparison, Transformation, Amenities & Facilities, Demand & Supply, Rentability, and Primary School proximity. These are useful—but each has blind spots. Below is a grounded way to analyse each factor, with pros/cons, what to look for, and common traps. --- 1) Entry Price (Is it “cheap” for the area—or just “cheap for a reason”?) What it is: Comparing a project’s launch price (usually in $PSF) against its surrounding region’s pricing range at that point in time. Some also try to infer the developer’s break-even vs profit margin. Pros - Forces context: A $2,300 psf condo means different things in CCR vs OCR. - Highlights mispricing: Occasionally, new launches are priced close to older resale condos nearby, creating a “value gap” opportunity. - Useful for downside risk: Buying at the top of a micro-market can limit exit options. Cons / Pitfalls - “Region pricing range” can be misleading: Singapore has micro-markets. A project 700m from an MRT can price very differently from one 1.5km away, even if both are “District X”. - New launch vs resale isn’t apples-to-apples: New launches bake in brand-new lease, nicer facilities, developer warranties, and marketing premiums. - Developer break-even is hard to estimate reliably: Land cost is known, but construction cost assumptions, financing, marketing, and product mix vary widely. Over-focusing on “developer margin” can create false confidence. Better ways to use Entry Price - Compare within a tight radius and similar attributes: - distance to MRT (walk vs feeder bus) - tenure (99 vs freehold) - unit mix (mostly 1–2BR vs family-heavy) - remaining lease (for resale condos) - Track price positioning over time, not just a single snapshot: - Was it launched at a premium to nearby resale, and did that premium widen? --- 2) Resale Comparison (How liquid is your exit—really?) What it is: Comparing your target project’s pricing to comparable resale transactions nearby. Pros - Reality check on exit price: Resale data reflects what buyers actually paid (not what was asked). - Helps spot “ceiling prices”: Some neighbourhoods have psychological caps unless a big catalyst arrives (new MRT, major jobs node, etc.). - Signals buyer depth: Frequent transactions often indicate better liquidity. Cons / Pitfalls - Comparables can be wrong: Similar PSF doesn’t mean similar desirability (layout efficiency, facing, noise, condo prestige, proximity to amenities). - Newer condos typically trade at a premium: If you compare a 2026 TOP to a 2005 TOP directly, you may underestimate fair premium (or overestimate “upside”). - Small sample sizes: In boutique projects, a few transactions can distort the perceived market. Better ways to use Resale Comparison - Look at: - transaction volume (liquidity) - price dispersion (wide swings may indicate a “story-driven” project) - gap vs nearby substitutes (what else can a buyer buy with similar budget?) --- 3) Transformation (The “URA Master Plan” story: opportunity + timing risk) What it is: Government plans (URA Master Plan, new MRT lines, redevelopment, new commercial nodes, rejuvenation projects) that could improve accessibility, jobs, and lifestyle. Pros - Can create real demand: New MRT stations, business parks, and lifestyle nodes can change renter/buyer behaviour. - Supports longer-term appreciation: If transformation adds jobs and improves connectivity, demand can become structural, not just speculative. Cons / Pitfalls - Time horizon mismatch: Transformation can take 5–15 years. Your holding power matters. - “Priced-in” risk: By the time it’s widely known, developers may already price in the upside. - Execution uncertainty: Plans can be phased, resized, or delayed. Even when delivered, impact may be uneven across the area. Better ways to analyse Transformation - Separate catalysts into: - Confirmed & funded (e.g., station under construction) - Planned conceptually (early-stage land use intents) - Ask: Does transformation add (1) accessibility, (2) jobs, (3) amenities, or only “nice-to-have” beautification? The first two tend to move prices/rents more decisively. --- 4) Amenities & Facilities (Convenience sells—but so do low monthly outgoings) What it is: Nearby transport, food, groceries, and internal condo facilities (pool, gym, function room, etc.). Also includes unit size and liveability. Pros - Direct impact on rentability and resale: Convenience is one of the most consistent drivers of tenant and buyer choice. - Reduces vacancy risk: A tenant who can walk to MRT/supermarket is less price-sensitive. - Liveability matters for owner-occupiers: Practical layouts and daily convenience often beat “fancy brochure features”. Cons / Pitfalls - Facilities aren’t free: More facilities often mean higher maintenance fees, which can reduce investor yield or buyer appetite later. - “Condo facilities checklist” is not universal: Tennis courts, huge grounds, multiple pools—some buyers love them, others see them as cost-heavy. - Unit size and efficiency can trump facility count: A 2BR with awkward corridors may underperform a smaller but efficient layout. Better ways to evaluate Amenities & Facilities - Measure walk time, not “nearby”: - actual sheltered walkway? - crossings/traffic lights? - slope/heat exposure? - Look for “daily essentials”: - supermarket, hawker/coffee shop, clinic, childcare, bus interchange/MRT - Check layout efficiency: - bay windows, long corridors, odd angles = wasted area = weaker value retention --- 5) Demand & Supply (The macro story is important—but the pipeline is everything) What it is: Balancing how many units are coming into the market (new supply, upcoming TOPs, GLS sites) against demand drivers (household formation, upgrader pools, expat demand, nearby job nodes). Pros - Explains price/rent pressure: Oversupply clusters often coincide with slower growth and higher competition among landlords. - Useful for timing: Buying before a wave of completions can mean tougher rental competition; buying after a wave may reduce supply pressure. Cons / Pitfalls - People oversimplify: “High supply = bad” isn’t always true. If a new MRT or business node is also arriving, demand may rise alongside supply. - Supply can be micro-specific: Two stops apart on the same MRT line can behave very differently. - Demand composition matters: Family buyers, investors, and expats respond to different triggers. Better ways to analyse Demand & Supply - Map: - nearby projects TOP-ing in the same 1–3 year window - unit types being added (many 1BRs can saturate rental competition) - Identify demand anchors: - business parks, hospitals, universities, industrial clusters, city fringe accessibility - Watch “substitute competition”: - new launches nearby can divert your future resale buyers. --- 6) Rentability (Tenant demand is not just “near MRT”) What it is: The likelihood of attracting tenants consistently at good rents, keeping vacancy low and supporting investor demand (which can also support resale liquidity). Pros - Creates a second buyer pool: When a project rents well, investor interest broadens your exit options. - Buffers during softer markets: Strong rental demand can offset holding costs. - Helps price resilience: Areas with durable tenant bases can hold value better. Cons / Pitfalls - Gross yield can be deceptive: Maintenance fees, vacancy, agent fees, repairs, and furnishing reduce net yield. - Tenant profile mismatch: A condo marketed for expats may struggle if nearby demand is mostly local families (or vice versa). - Small-unit saturation: If an area has many shoebox/1BR units, landlords compete aggressively on rent and incentives. Better ways to evaluate Rentability - Identify the likely tenant segment: - expats (CBD access, international schools, lifestyle nodes) - locals (near work hubs, near parents, near schools) - students (universities, polytechnics—where applicable) - Check: - realistic commute time to job clusters (not just “on the same line”) - whether the unit type matches demand (e.g., 2BR for small families/roommates) --- 7) Primary School Within 1km (Bonus factor—powerful, but not automatic) What it is: Proximity to popular primary schools can influence demand from parents (owner-occupiers and some tenant families), potentially supporting resale value. Pros - Creates non-investor demand: Parent buyers can be less price-sensitive when school priority is perceived as valuable. - Supports family-tenant rentability: Some families rent to secure proximity (though eligibility rules and balloting nuances matter). - Improves resale liquidity: Family-driven demand can stabilise transaction volume. Cons / Pitfalls - Not a guaranteed admission: Balloting phases and citizenship priority mean “within 1km” doesn’t equal certainty. - Value varies by school reputation and cohort pressure: Not all “within 1km” carries the same premium. - May not help small-unit projects: If a condo is mostly 1BR/compact 2BR, the family buyer pool is naturally smaller. Better ways to use the School Factor - Treat it as an upside stabiliser, not the sole investment thesis. - Match unit mix to buyer profile: - if you’re banking on school demand, family-sized functional layouts matter. --- Putting It Together: A Balanced Scorecard (Instead of a Single “Best Factor”) A practical way is to weigh each category by how directly it affects (1) exit liquidity, (2) downside risk, and (3) holding power: - Downside risk: Entry Price + Supply pipeline + substitutability - Exit liquidity: Resale comparables + buyer pool breadth (investor + owner-occupier) - Holding power: Rentability + maintenance costs + unit efficiency - Optional upside: Transformation + school proximity (when not already priced in) --- Common “Good-on-Paper” Traps to Avoid - Buying the story, not the numbers: Transformation headlines without clear timelines or measurable demand drivers. - Overrating facilities: More isn’t always better if monthly costs reduce appeal. - Ignoring unit efficiency: Layout beats brochure size; tenants/buyers feel it immediately. - Comparing across mismatched products: Tenure, age, MRT distance, and unit mix must be aligned.

-

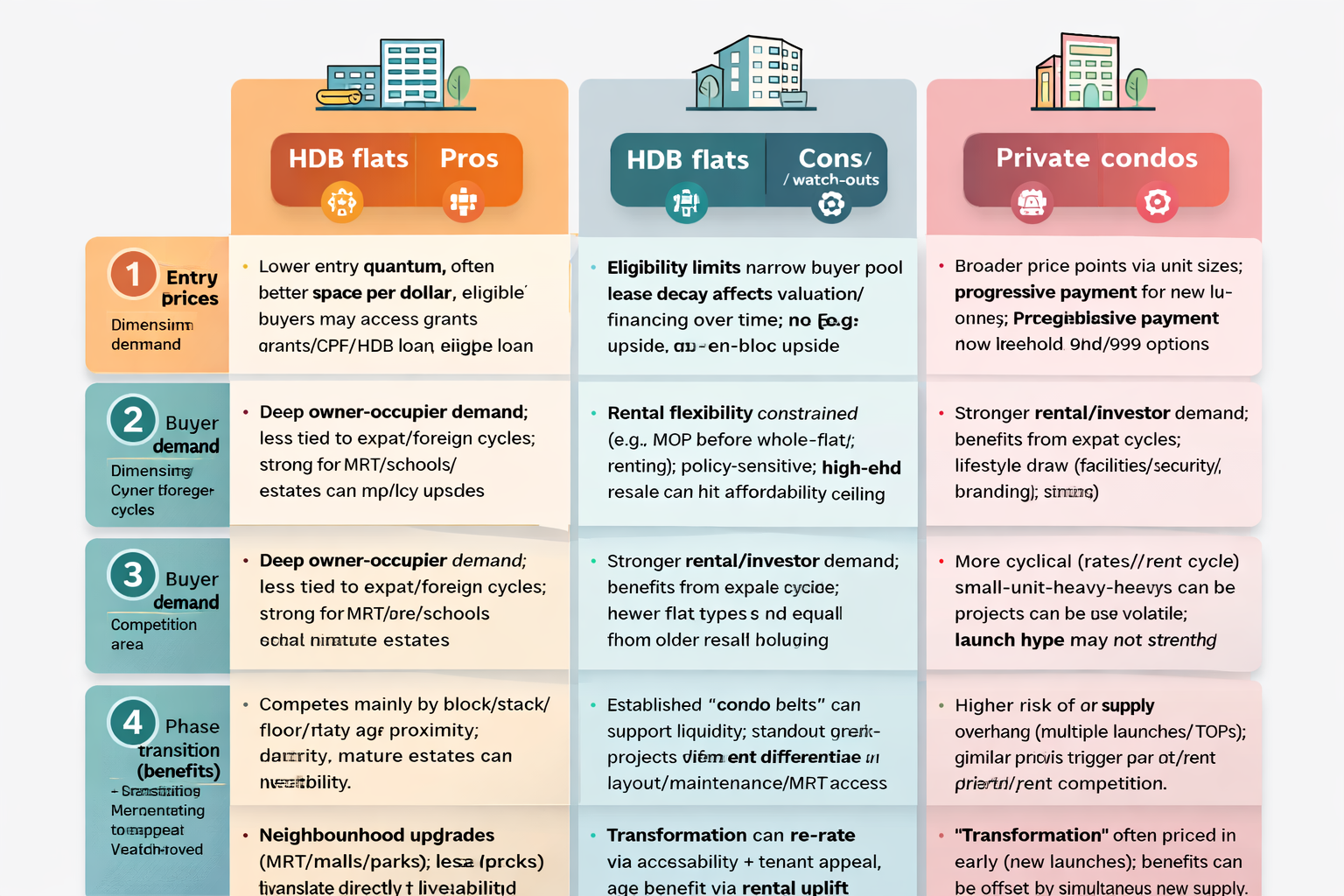

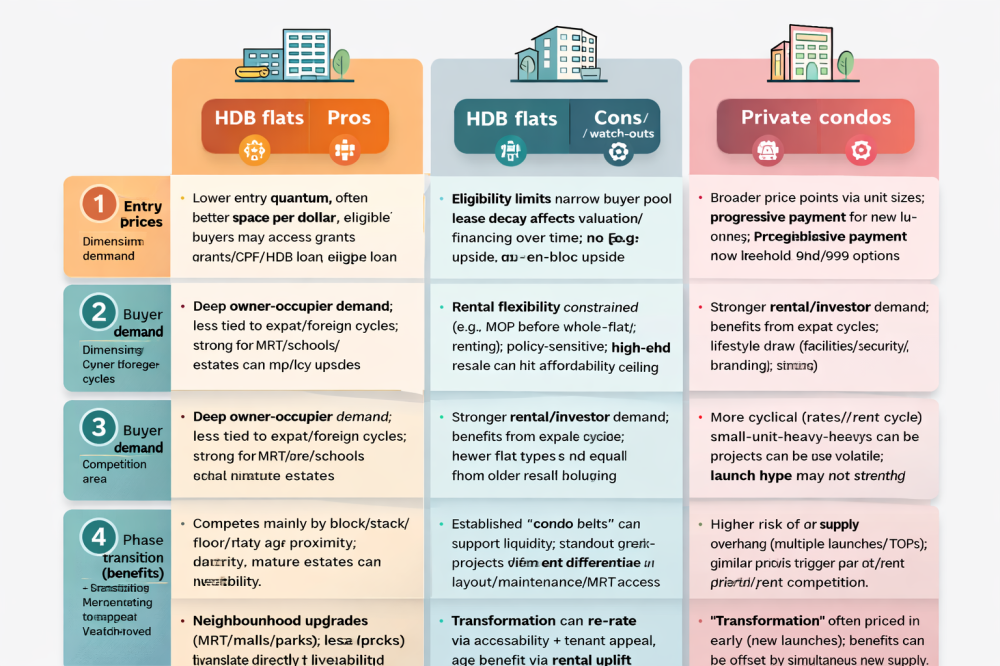

Introduction A practical pro and cons review of how Singapore property is often assessed and sometimes marketed by real estate agents, organised around four kEY points. This article will cover what tends to be true, what can be overstated, and what to check to validate the story. 1) Entry Prices Pros (what agents highlight) - “Affordable quantum” even if PSF is high: Smaller units in OCR/RCR can look entry-friendly (e.g., 1–2 bedders). Agents often position this as easier to own/exit. - New-launch pricing clarity: Fixed developer price list, progressive payment scheme, and “fresh lease” are pitched as a premium worth paying. - Resale “value gap”: Resale condos/HDBs in mature estates may look cheaper than nearby new launches on a PSF basis, creating a “relative value” narrative. Cons (real-world friction) - High absolute price levels: Singapore’s base price has risen materially over the past cycle; “entry” is often still a large downpayment + mortgage burden. - Quantum traps: - Small units can have higher PSF and more volatile resale demand (investor-led, tenant-led). - Maintenance fees can be disproportionately painful for small units. - Lease/tenure penalty: - Older leasehold properties can face financing constraints and valuation sensitivity as lease decays (especially for older HDBs and older leasehold condos). - Policy/financing constraints: - ABSD, TDSR/MSR, and LTV limits can make “cheap entry” less meaningful if you’re constrained by eligibility or total debt servicing. What to check (quick validation) - Compare quantum, PSF, and maintenance fees side-by-side for the same unit type. - Review recent caveats (URA Realis) for actual transacted prices, not just asking prices. - For older assets: check remaining lease, recent bank valuations, and resale time-on-market. --- 2) Buyer Demand Pros (common demand drivers) - Owner-occupier base demand: Singapore has structurally strong owner-occupier preference (especially for well-located resale and family-sized layouts). - Rental market supports investors (cyclical, but can be strong): Proximity to MRT/business nodes/schools often sustains rental demand. - Scarcity narratives: “Mature estate, limited supply” can be real in some pockets, supporting resale liquidity. Cons (where demand can be overstated) - Demand is segmented: - 1-bedders are often investor/tenant-driven; demand can drop fast if yields compress or policies tighten. - Large units rely on affluent upgrader demand which is sensitive to interest rates and stock-market sentiment. - New-launch demand can be “event-driven”: - Strong launch weekend take-up doesn’t always translate to strong resale premiums later, especially if many similar projects TOP together. - Foreign demand is policy-sensitive: - High ABSD for foreigners means foreign buyer demand is concentrated in specific segments and can switch off quickly. What to check - Track transaction volume trends (not just price) in the last 6–12 months. - For investment: test net yield after maintenance, property tax, agent fees, vacancy assumptions. - For family demand: check school zone reality (1km rules), actual walk time to MRT, and nearby amenity maturity. --- 3) Competition Within the Area Pros (how competition can help) - Cluster effect: Multiple condos in an area can create a known “condo belt” that attracts tenants and buyers (more comparables, more visibility). - Amenity build-out: Competition among developers/MCSTs can improve landscaping, facilities, and upkeep standards—helping perceived value. Cons (most important risk) - Supply overhang / “cannibalisation”: - If multiple projects launch or TOP around the same time, you can see resale price stagnation and rental competition (landlords undercut each other). - Similar product problem: - If nearby projects offer similar layouts/size/pricing, your unit’s differentiation is weak—buyers pick based on price, squeezing upside. - Exit liquidity varies by stack and layout: - Even in a “hot area,” odd layouts, poor facing, road noise, or weak stack positioning can face much slower resale. What to check - Look up the pipeline: GLS sites, upcoming launches, and estimated TOP dates within ~1–3 km. - Compare unit mix (how many 1/2/3-bedders) across projects—this predicts resale and rental competition. - Observe rental listings (number of competing listings + asking rents) to gauge landlord competition. --- 4) Phases of Transformation Agents frequently sell a “transformation story.” This can be valid—but timing matters. Typical phases (and what they mean for buyers) Phase 1: Announcement / Masterplan headline (0–2 years) - Pros: Sentiment uplift; “early-bird” narrative; some price repricing happens quickly if the plan is credible. - Cons: Most of the gain can be front-loaded; execution risk is high; details are often vague. Phase 2: Infrastructure commitment (2–6 years) - Examples: confirmed MRT line/station, major road links, institutional anchors. - Pros: Real improvement in accessibility; demand broadens; rental appeal can improve. - Cons: Construction noise/dust; detours; liveability dips short-term; “buy the rumour, sell the news” risk. Phase 3: Commercial/amenity activation (5–10+ years) - Examples: malls, offices, parks, schools, healthcare nodes actually open and operate. - Pros: Strongest fundamental support for both owner-occupiers and tenants; resale liquidity tends to improve. - Cons: By the time benefits are obvious, entry price is usually much higher; upside may be more limited. Phase 4: Maturity / Re-rating stabilises - Pros: More stable demand base; clearer price discovery. - Cons: Growth can slow; you rely more on broader market cycles than “transformation alpha.” Singapore examples of transformation narratives (illustrative) - Jurong Lake District / 2nd CBD influence on nearby OCR/RCR nodes. - Greater Southern Waterfront long-horizon uplift narrative for city fringe/southern corridor. - Punggol Digital District and surrounding Punggol/Sengkang rental/owner demand themes. - Tengah new town (longer ramp-up; amenity maturity is the key risk early on). - New MRT lines / station additions (e.g., Cross Island Line and extensions) often drive micro-market repricing—timing matters most. What to check - Confirm whether the “transformation” is funded and scheduled (not just conceptual). - Map walkability (true 8–10 min walk vs “one traffic light away” marketing). - Assess whether your holding period matches the transformation timeline (e.g., 3 years vs 10 years). --- ## A quick “agent claims” checklist (to keep it grounded) - Ask for 3 nearest comparable transactions in the last 3 months (same size, same project/nearby). - Ask what new supply is coming within 24–48 months. - Ask what the exit buyer is (upgrader? investor? family?) and whether the unit mix supports that. - Stress test at higher interest rates and more conservative rents. --- Here’s how the same “pros/cons” framework typically differs between HDB flats and private condos in Singapore. 1) Entry Prices HDB flats Pros - Lower entry quantum (especially non-mature estates) and often better $/sqft for space. - More financing support/affordability levers for eligible buyers (CPF usage; grants for eligible first-timers; HDB loan option for some). - Resale price discovery is clearer because the buyer pool is mostly owner-occupiers. Cons - Eligibility constraints (citizenship, family nucleus, income ceilings for some schemes) can limit who can buy. - Lease decay matters more visibly over time (and can affect financing/CPF usage depending on remaining lease and buyer age). - Less “asset enhancement” optionality (no renovation-to-luxury positioning that shifts a whole project’s brand; no en-bloc). ### Private condos Pros - Broader buyer pool (Singaporeans, PRs, and—policy-dependent—foreigners) supports liquidity in some segments. - Wider product range (small units for lower quantum entry; new launches with progressive payment). - Freehold/999 options (where available) can support long-hold narratives. Cons - Higher entry cost (downpayment + typically higher absolute prices). - ABSD exposure is a bigger deal for many condo buyers (2nd/3rd property, PR/foreigner). - Ongoing costs: maintenance fees, sinking fund, and higher frictional costs can erode returns, especially for small units. --- 2) Buyer Demand HDB flats Pros - Deep, stable owner-occupier demand (family formation, upgrader flow from smaller flats). - Less sensitive to “luxury cycles” and foreign buyer sentiment. - Certain locations (near MRT, schools, mature estates) enjoy very consistent resale interest. Cons - Rental demand is constrained by rules (e.g., Minimum Occupation Period before renting whole flat; tighter subletting conditions vs condos). - Demand is policy-sensitive (grant changes, HDB supply pipeline, cooling measures). - High-priced resale flats can face affordability ceilings faster because buyers are mainly local income-based households. Private condos Pros - Investor + tenant demand is a core demand pillar (especially near MRT, CBD/fringe, business parks, universities). - Can benefit more directly from expat cycles and rental market upswings. - More “lifestyle” demand: facilities, security, branding. Cons - Demand can be more cyclical (rates, job market, rental cycle). - If a project is dominated by small units/investors, resale can turn more volatile when yields compress. - New-launch demand can be strong at launch but weaker at resale if many similar projects TOP together. --- 3) Competition Within the Area HDB flats Pros - Competition is often more about which block/stack, floor, renovation, and proximity to MRT/amenities, rather than competing “projects.” - In mature estates, limited new HDB resale substitutes can support prices. Cons - BTO/Prime model supply nearby can cap upside for older resale flats (buyers may choose a subsidised new flat if wait-time is acceptable). - Nearby “better” flat types (e.g., newer 4/5-room projects) can pull demand away from older stock. Private condos Pros - Multiple condos nearby create a benchmarking ecosystem (more comps), which can support liquidity if the area is established. - A standout project can differentiate on layout efficiency, maintenance, views, direct MRT link, or full amenities. Cons - Supply overhang risk is higher (GLS sites, multiple launches, and simultaneous TOPs can depress resale and rents). - Projects often compete on very similar features; without differentiation, it becomes a price war at resale or rental. --- 4) Phases of Transformation HDB flats Pros - Transformation (new MRT, mall, park, town centre) tends to translate more directly into owner-occupier convenience value, supporting steady demand. - Upgrading of amenities can improve liveability even if price growth is moderated. Cons - Upside can be bounded by affordability of the core buyer pool and by policy settings. - Lease age remains a structural headwind for older flats even if the neighbourhood improves. Private condos Pros - Transformation can create outsized re-rating if it materially improves tenant appeal (new MRT, office nodes, lifestyle hubs). - More able to monetise transformation through rental uplift and broader buyer segments. Cons - Transformation gains can be priced in early (especially new launches marketed on future plans). - If transformation coincides with heavy new supply, the benefit can be offset by competition (more units chasing the same tenants/buyers). --- Practical takeaway - HDB: generally stronger on affordability + stable owner-occupier demand, weaker on policy/eligibility constraints + lease decay + limited rental flexibility. - Condo: stronger on rental/investor optionality + broader buyer pool + transformation-driven re-rating, weaker on higher entry costs/ABSD + supply competition + higher holding costs. This topic has nothing to do with Feng Shui. I am also not a Real Estate agent. I am simply, just like you, a property buyer who is interested in property trends in SG.

- Yesterday

-

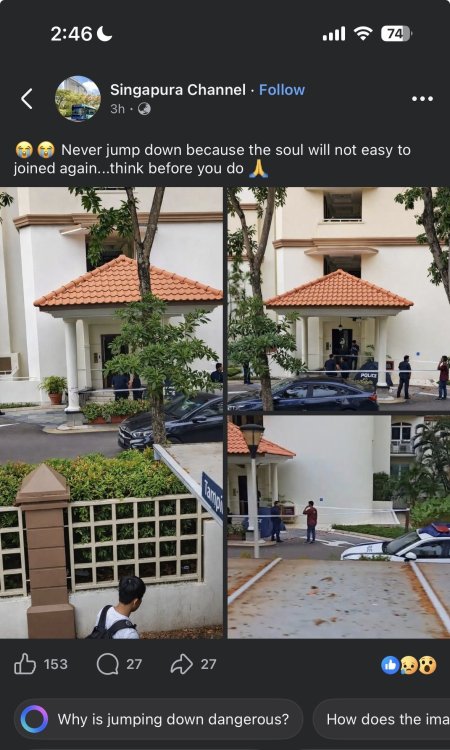

Source & Credit:

-

It seems not everyone agrees with the above. Please keep in mind: it depends.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

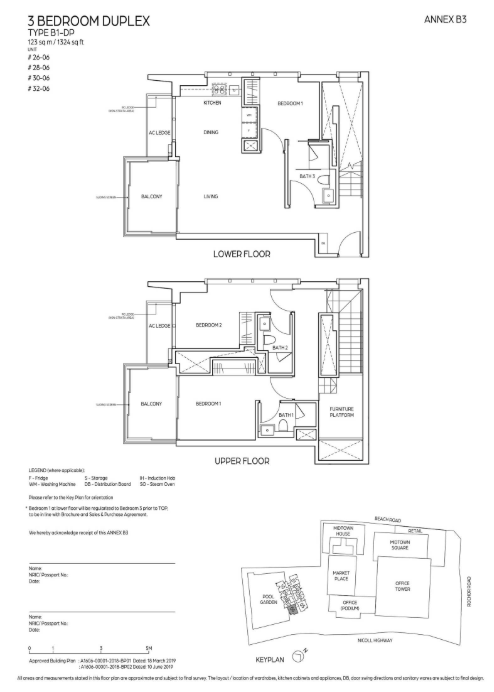

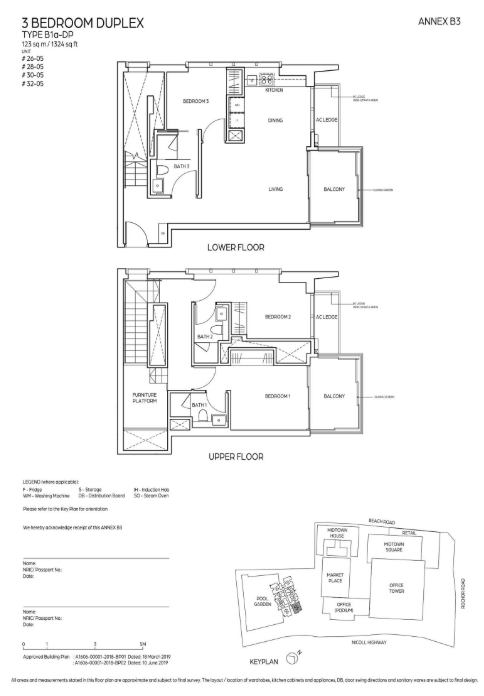

3 Bedroom Duplex

-

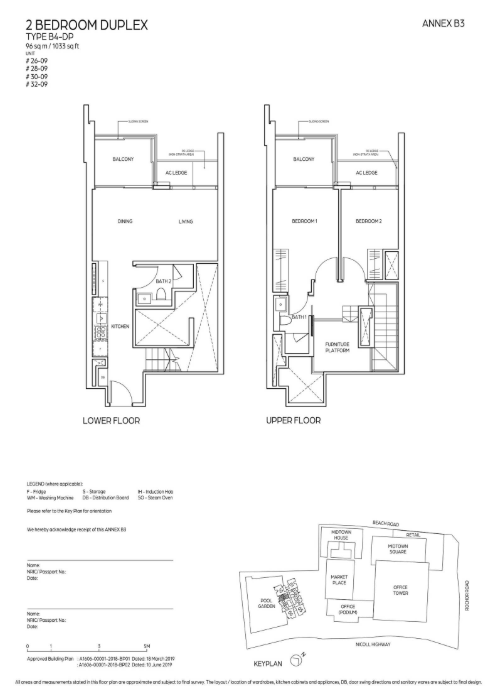

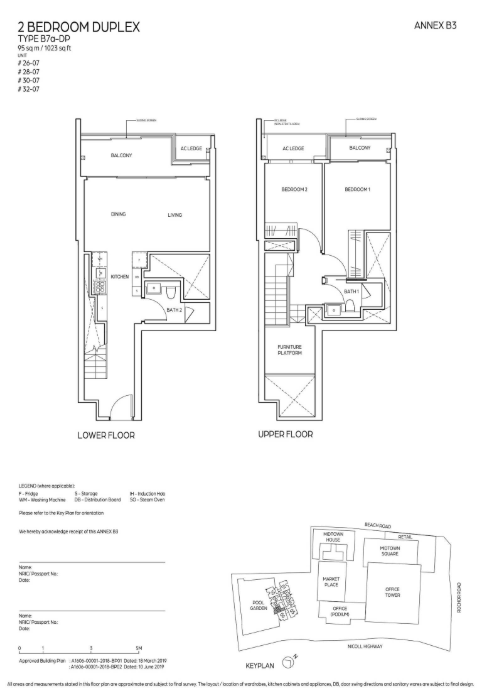

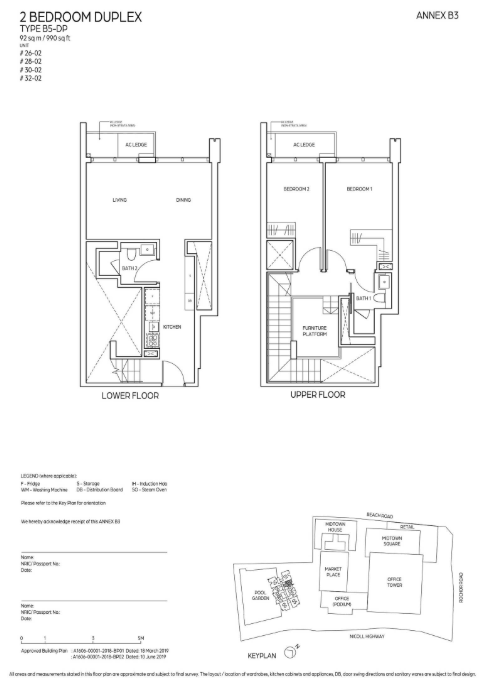

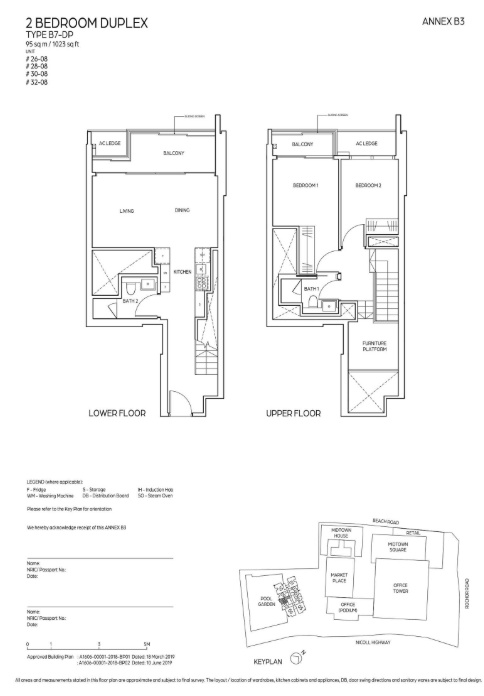

2 Bedroom Duplex

-

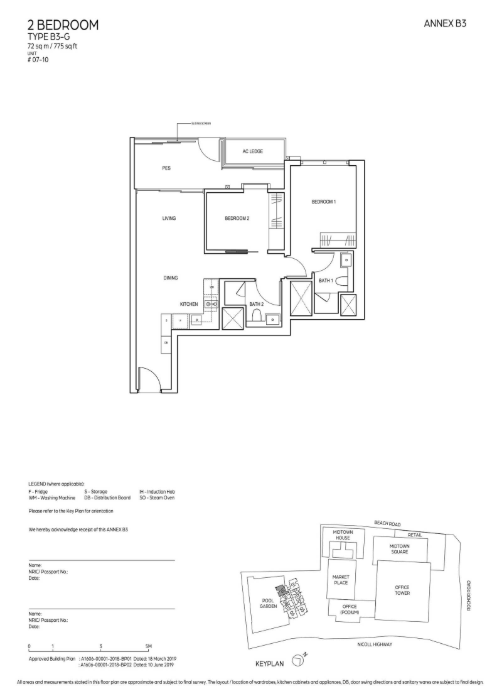

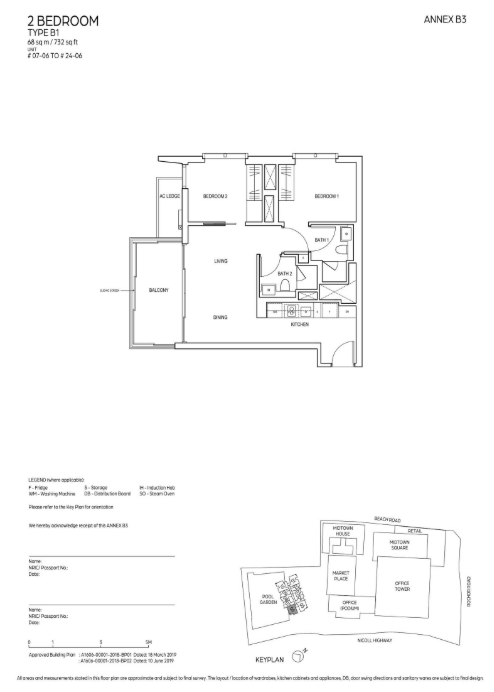

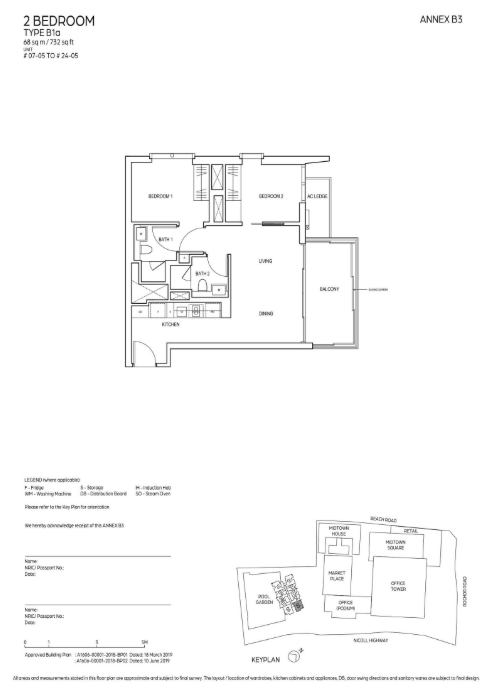

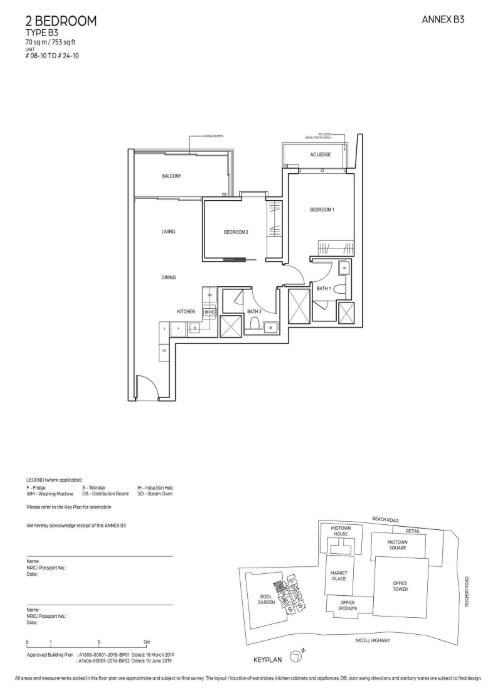

2 Bedroom

-

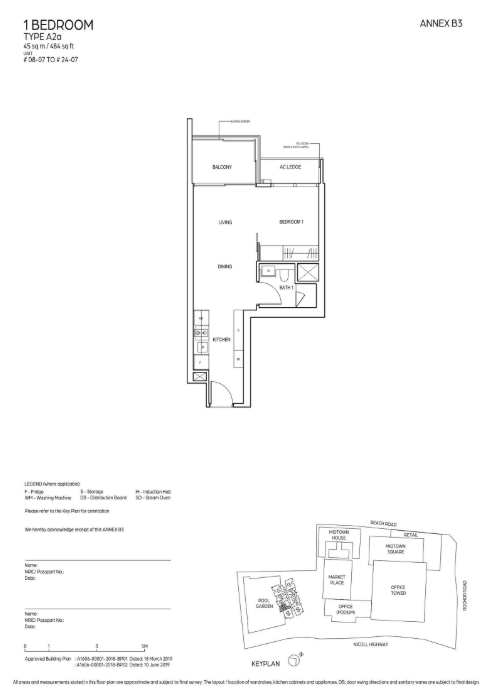

1 Bedroom

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

Thinking about buying a home that faces the afternoon sun? BUT +++

-

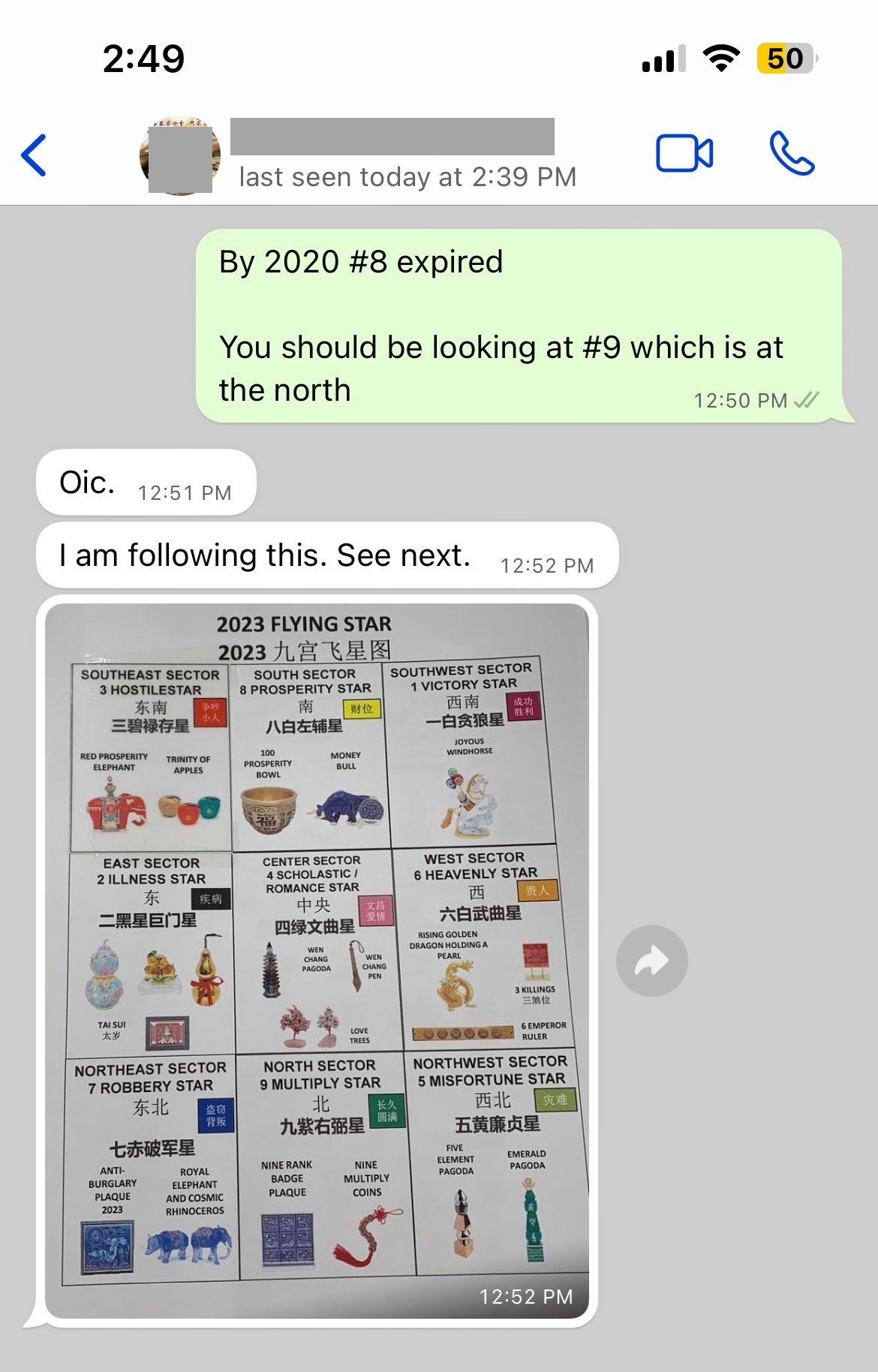

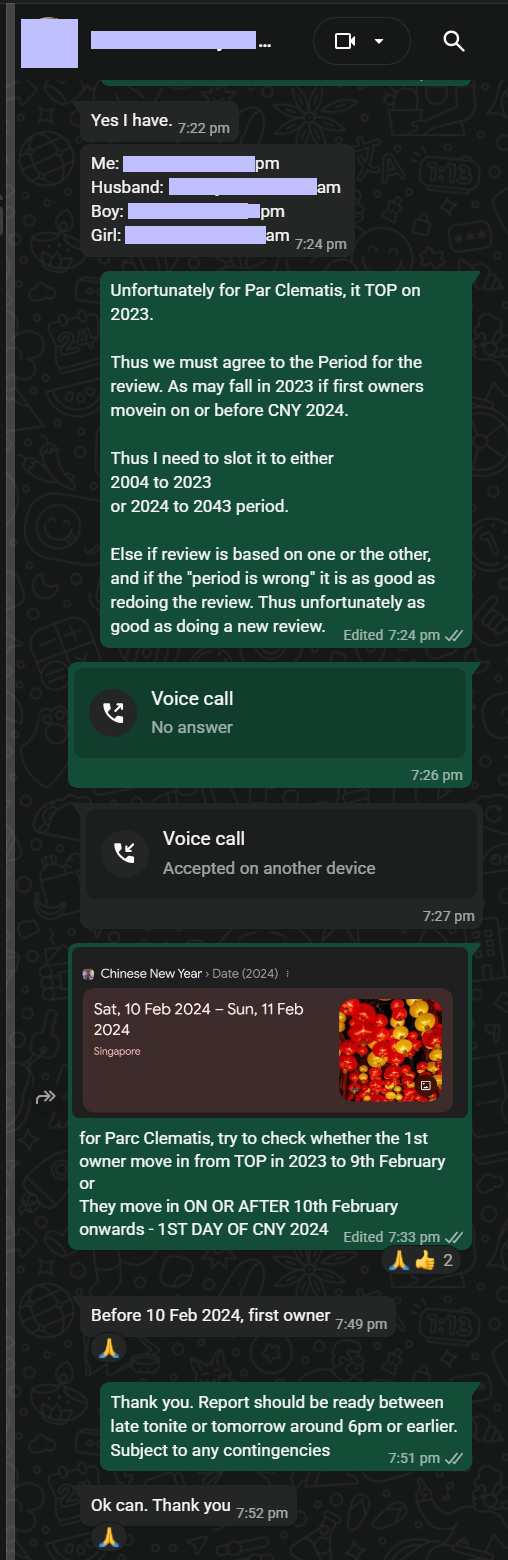

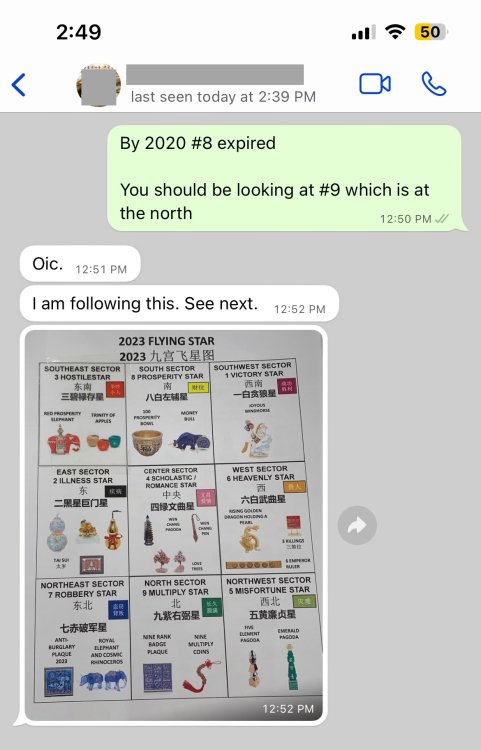

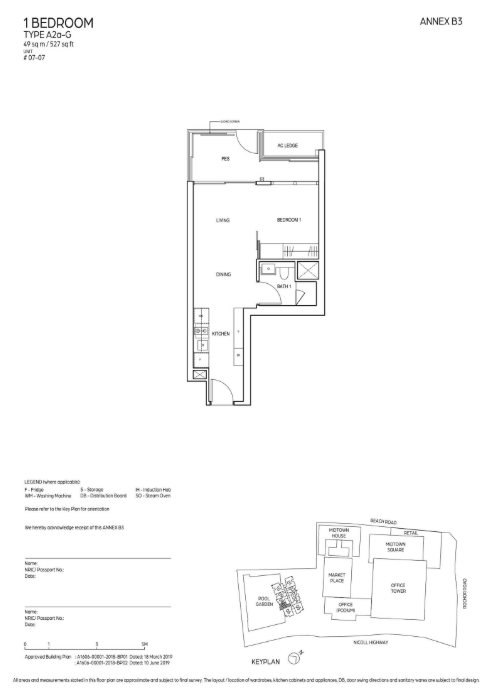

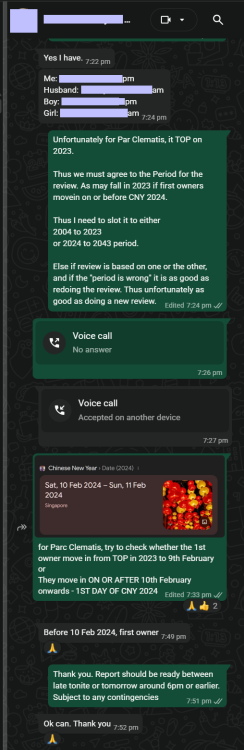

TOP in 2023 - If you move in on or before CNY 2024 (9 February 2024 or earlier), use Period 8 Feng Shui. If the first owner moves in on or after 10 February 2024, use Period 9 Feng Shui. More AN EXAMINATION OF WHICH FLYING STAR PERIOD ONE SHOULD UTILIZE? +++ Which Flying Star Period to Use? For example, take a look at Treasure @ Tampines The transition of Feng Shui Qi is significant in the context of the Chinese New Year 2024, as it influences the energy dynamics within a space. The timing of when a unit is first occupied plays a crucial role in determining its Flying Star Feng Shui. This means that the specific day of occupancy will affect the energetic quality and overall Feng Shui of the unit, highlighting the importance of timing in Feng Shui practices. Understanding these elements can help individuals optimize their living environments in alignment with the changing energies associated with the New Year. +++ When did the first owner/resident/tenant take residence in the unit at Treasure @ Tampines? +++ EITHER Can be the owner, resident or a tenant OR Can be the owner, resident or a tenant REGARDLESS, UNITS FACING NORTH POSSESS A POSITIVE FENG SHUI OVERALL How do you Feng Shui your home? Use your front door? Who are the Conservatives & the Modernist? +++ For Parc Clematis, for example, many collected their keys in 2023. However, some may choose to move in on or after CNY 2024. +++ Cecil Lee, Geomancy.net

-

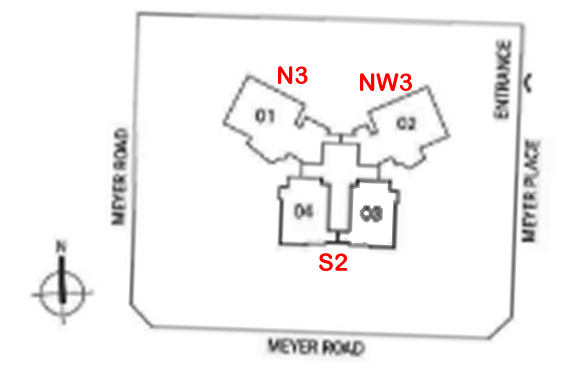

One Meyer Site Plan

-

One Meyer Site Plans

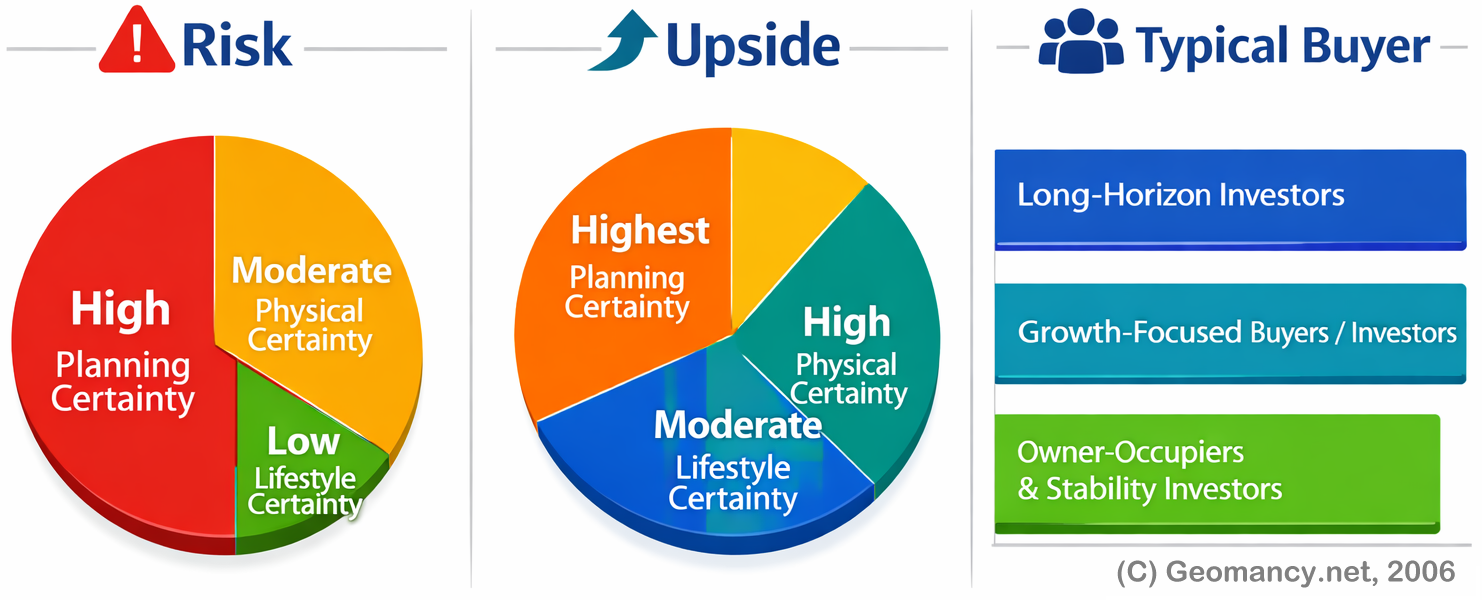

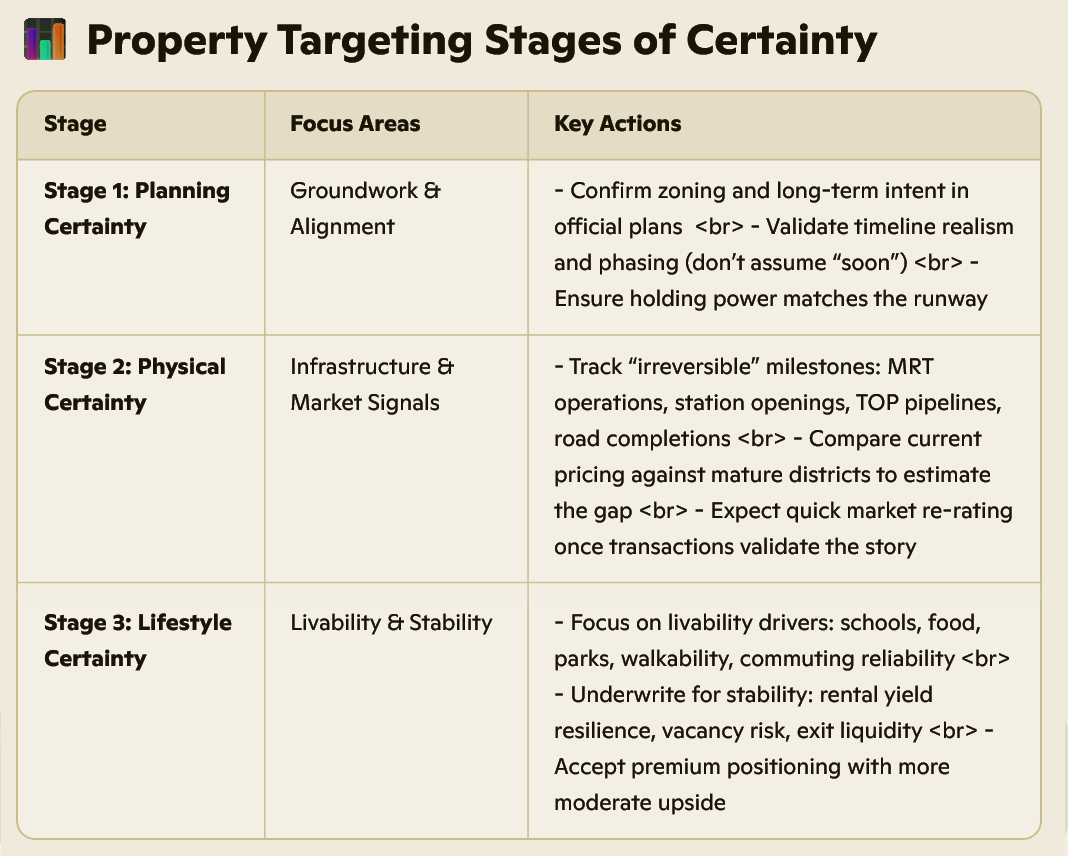

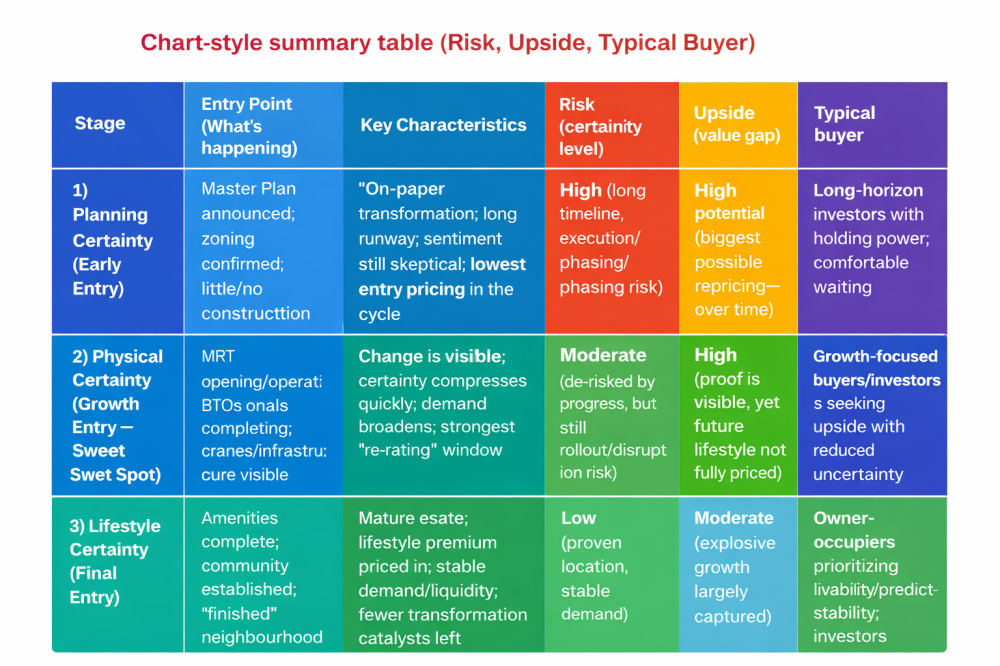

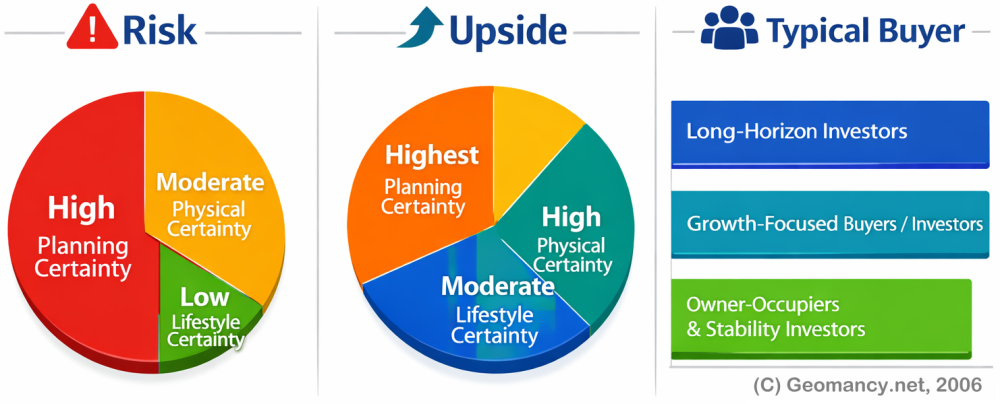

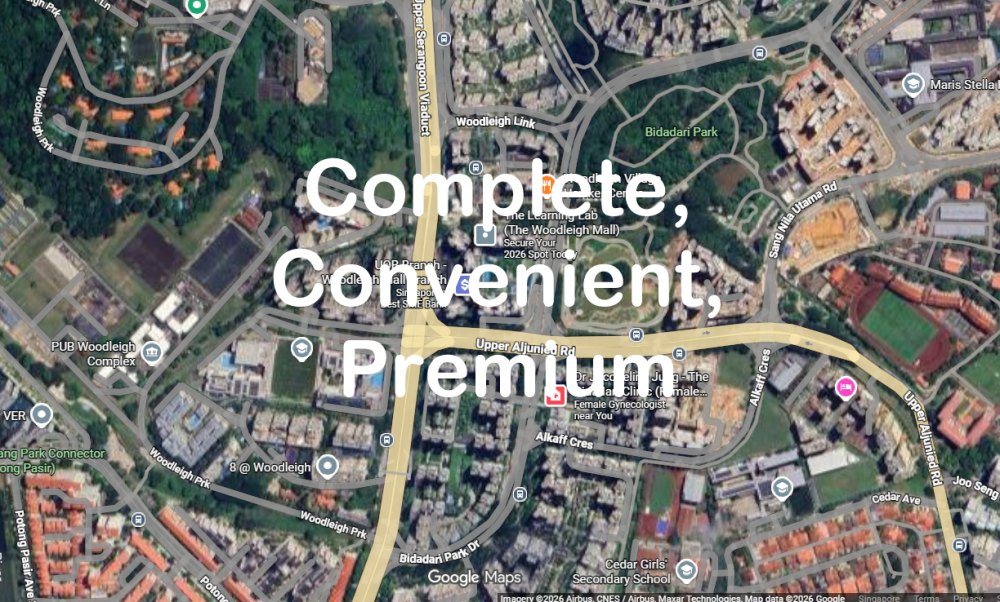

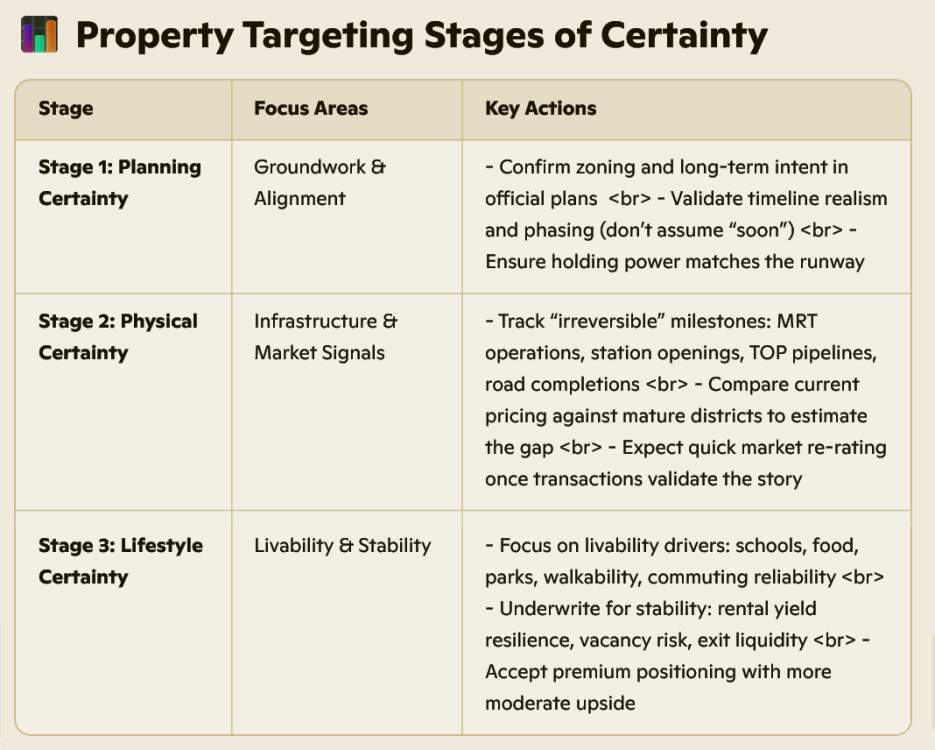

+++ The 3 Certainties of Property Transformation: A Professional Framework for Timing Your Entry The 3 Signals: When to Enter Real estate outperformance is rarely about “finding a cheap unit.” It is more often about entering a location at the right point in its transformation cycle—when the market has not yet fully priced in what is coming, but the probability of change is rising. A practical way to time this is to track three escalating forms of certainty: 1. Planning Certainty (Early Entry) 2. Physical Certainty (Growth Entry — the Sweet Spot) 3. Lifestyle Certainty (Final Entry) Each stage carries a different risk profile, valuation logic, and profit potential. The investors who consistently do well are not guessing the future—they are buying certainty before it becomes consensus. Since 1996, (C) Geomancy.net Stage 1 — Planning Certainty (Early Entry): “The Blueprint Is Real, But the Ground Is Empty” What it looks like - Government master plan announced - Zoning confirmed, land use intentions clarified - Nothing built yet (or minimal enabling works) - The narrative is strong, but proof on the ground is limited Why prices are lowest here At this stage, the market discounts heavily because the timeline is long and outcomes feel abstract. Even if the plan is credible, buyers price in: - execution risk (delays, phasing, policy shifts) - opportunity cost (capital tied up for years) - uncertainty around the eventual “vibe” of the area Result: This stage often offers the lowest entry prices in the entire cycle. Who Stage 1 is for - Investors with long holding power - Buyers comfortable with “paper certainty” and longer waits - Portfolios that can tolerate slower initial appreciation Example: Paya Lebar Airbase (PLA) - Announced in 2013, reinforced by planning clarity including the 2025 Master Plan - Approximately 800 hectares of future mixed-use development - Connectivity uplift (e.g., Cross Island Line integration) - Major development expected to ramp in the 2030s Interpretation: This is classic Planning Certainty—arguably the lowest-cost point of entry, but also the longest runway. Stage 2 — Physical Certainty (Growth Entry): “You Can See It Now” (The Sweet Spot) One of the most often-quoted examples in the recent past was Bidahari Estate. What it looks like - MRT stations opening or operational - BTO projects completing, population starting to form - Cranes are up (active construction, visible delivery) - Roads, bridges, parks, and commercial nodes are clearly taking shape This is the inflection point where the market shifts from believing to recognizing. Why this stage tends to produce the biggest profits Stage 2 is where you often get the best mix of: - de-risking (proof replaces speculation) - still-wide valuation gap (future amenities are not fully priced) - accelerating demand (buyers upgrade their confidence) In simple terms: the discount for uncertainty shrinks rapidly, but the neighbourhood is not “finished”—so you are not yet paying the full lifestyle premium. Who Stage 2 is for - Buyers seeking strong upside with reduced uncertainty - Investors who want to ride the re-rating phase (not just wait for completion) - Owners comfortable with some construction disruption in exchange for value capture Example: Bidadari (The “Cemetery” Mispricing) When The Woodleigh Residences launched in 2019 at about $1,733 psf, public perception lagged reality. Many still anchored on the old “cemetery” identity. But the physical signals were already strong: - MRT presence and connectivity were real - Roads were being realigned and infrastructure works were tangible - BTO completions were bringing in residents and demand fundamentals A reported outcome: ~$660,000 profit—generated not by buying a finished estate, but by buying during Physical Certainty, before broad-market pricing fully adjusted to the new reality. Example: Lentor (Certainty Compression in Real Time) With the Thomson–East Coast Line (TEL) and the area’s redevelopment momentum, Lentor illustrates how pricing can escalate as certainty increases: - Early launches price in “potential” - Later launches price in “proof” (transport reliability, buyer adoption, comparable transactions) - Each new delivery milestone compresses the uncertainty discount further Key takeaway: In districts like Lentor, the biggest jumps typically come as the MRT and surrounding projects transition from plan → operation → lived experience. Stage 3 — Lifestyle Certainty (Final Entry): “Complete, Convenient, Premium” What it looks like - Area is fully developed - Amenities are complete (retail, schools, parks, transport integration) - A vibrant community exists (the place has identity and habit) - Rental demand is stable, and owner-occupier willingness to pay is high Why profits are solid but moderate By Stage 3, you are paying for: - certainty - convenience - comfort - a proven neighbourhood The trade-off is that the explosive repricing has usually already happened. Returns can still be good, but the entry price is higher, and incremental gains are often steadier rather than outsized. Who Stage 3 is for - Owner-occupiers prioritizing quality of life and predictability - Investors seeking stability, easier leasing, lower “execution risk” - Buyers who prefer to pay a premium to avoid transformation disruption Example: East Coast (Finished-Neighbourhood Premium) Examples cited: - Liv @ MB buyers averaged about $275K–$354K profit - Amber Park averaged about $264K–$536K These are respectable outcomes—but the entry pricing tells the story: - Buyers entered around $2,368–$2,479 psf, substantially higher than Woodleigh’s earlier $1,733 psf Interpretation: East Coast reflects Lifestyle Certainty—strong, proven demand and good profits, but much of the “transformation alpha” is already captured in the price you pay. --- The Core Insight: Markets Don’t Reprice Once—They Reprice Three Times You can think of the transformation cycle as three separate repricing events: 1. Planning Certainty: repricing begins quietly (only some buyers act) 2. Physical Certainty: repricing accelerates (evidence converts skeptics) 3. Lifestyle Certainty: repricing stabilizes (premium for completion, not potential) The most consistent outperformance tends to occur when you enter before the crowd upgrades its confidence—but after enough proof exists to meaningfully reduce downside risk. That is why Stage 2 is often the “sweet spot.” --- How to Use This Framework (Practical Checklist) In Summary, ### Chart Summary: Risk, Upside, and Typical Buyer Profiles The graphic breaks a property/opportunity into three lenses—**Risk**, Upside, and Typical Buyer—using “certainty” levels to show what is most/least predictable and where the value potential sits. 1) Risk (left pie) Risk is driven mainly by planning certainty: - High Planning Certainty (largest share): The dominant risk factor relates to the planning/entitlement environment (e.g., approvals, zoning, allowable uses). Even with “high certainty,” planning outcomes still represent the biggest risk component relative to the others. - Moderate Physical Certainty (mid share): Site/building conditions are somewhat knowable (e.g., condition, access, services, construction complexity), creating a moderate level of risk. - Low Lifestyle Certainty (smallest share): Lifestyle/amenity or “place experience” factors are least certain (e.g., neighborhood perception, livability, demand drivers tied to lifestyle), adding a smaller—but less predictable—risk portion. Interpretation: Overall risk is weighted toward planning/entitlement considerations, with physical factors secondary and lifestyle factors the least represented but more uncertain. 2) Upside (middle pie) Upside is where certainty translates into value creation potential: - Highest Planning Certainty (large share): The strongest upside comes from planning-related confidence—when the planning path is clear, the ability to execute and capture value is greatest. - High Physical Certainty (moderate-to-large share): Solid knowledge of the physical asset/site supports upside (e.g., deliverability, cost control, feasibility). - Moderate Lifestyle Certainty (moderate share): Lifestyle demand is a meaningful contributor to upside, but only moderately certain—suggesting upside exists, though it depends more on market sentiment and buyer preferences. Interpretation: Value potential is led by planning clarity, supported by physical deliverability, with lifestyle demand contributing but less reliably. 3) Typical Buyer Profiles (right panel) Based on that risk/upside mix, the likely buyers fall into three groups: 1. Long-Horizon Investors – Buyers comfortable holding through cycles and timelines, often prioritizing durable, long-term value. 2. Growth-Focused Buyers / Investors – Buyers seeking appreciation and execution-driven returns, typically attracted to clearer planning and feasible delivery. 3. Owner-Occupiers & Stability Investors – Buyers prioritizing predictability, usability, and steady outcomes (often more sensitive to lifestyle and day-to-day fit). Overall takeaway The chart suggests an opportunity where planning certainty is the main driver of both risk and upside. Physical factors are comparatively well understood, while lifestyle factors are less predictable. As a result, the opportunity appeals to a mix of long-term, growth-oriented, and stability-focused buyers, depending on their tolerance for planning and market-driven uncertainty. 4) In Conclusion (See Below) +++ This topic isn’t related to Feng Shui at all. I’m also not a Real Estate agent. I’m simply, like you, a property buyer who’s interested in property trends in SG. These three stages are very commonly used by many local Realty Agents to explain a property’s profit potential, if any.

+++ The 3 Certainties of Property Transformation: A Professional Framework for Timing Your Entry The 3 Signals: When to Enter Real estate outperformance is rarely about “finding a cheap unit.” It is more often about entering a location at the right point in its transformation cycle—when the market has not yet fully priced in what is coming, but the probability of change is rising. A practical way to time this is to track three escalating forms of certainty: 1. Planning Certainty (Early Entry) 2. Physical Certainty (Growth Entry — the Sweet Spot) 3. Lifestyle Certainty (Final Entry) Each stage carries a different risk profile, valuation logic, and profit potential. The investors who consistently do well are not guessing the future—they are buying certainty before it becomes consensus. Since 1996, (C) Geomancy.net Stage 1 — Planning Certainty (Early Entry): “The Blueprint Is Real, But the Ground Is Empty” What it looks like - Government master plan announced - Zoning confirmed, land use intentions clarified - Nothing built yet (or minimal enabling works) - The narrative is strong, but proof on the ground is limited Why prices are lowest here At this stage, the market discounts heavily because the timeline is long and outcomes feel abstract. Even if the plan is credible, buyers price in: - execution risk (delays, phasing, policy shifts) - opportunity cost (capital tied up for years) - uncertainty around the eventual “vibe” of the area Result: This stage often offers the lowest entry prices in the entire cycle. Who Stage 1 is for - Investors with long holding power - Buyers comfortable with “paper certainty” and longer waits - Portfolios that can tolerate slower initial appreciation Example: Paya Lebar Airbase (PLA) - Announced in 2013, reinforced by planning clarity including the 2025 Master Plan - Approximately 800 hectares of future mixed-use development - Connectivity uplift (e.g., Cross Island Line integration) - Major development expected to ramp in the 2030s Interpretation: This is classic Planning Certainty—arguably the lowest-cost point of entry, but also the longest runway. Stage 2 — Physical Certainty (Growth Entry): “You Can See It Now” (The Sweet Spot) One of the most often-quoted examples in the recent past was Bidahari Estate. What it looks like - MRT stations opening or operational - BTO projects completing, population starting to form - Cranes are up (active construction, visible delivery) - Roads, bridges, parks, and commercial nodes are clearly taking shape This is the inflection point where the market shifts from believing to recognizing. Why this stage tends to produce the biggest profits Stage 2 is where you often get the best mix of: - de-risking (proof replaces speculation) - still-wide valuation gap (future amenities are not fully priced) - accelerating demand (buyers upgrade their confidence) In simple terms: the discount for uncertainty shrinks rapidly, but the neighbourhood is not “finished”—so you are not yet paying the full lifestyle premium. Who Stage 2 is for - Buyers seeking strong upside with reduced uncertainty - Investors who want to ride the re-rating phase (not just wait for completion) - Owners comfortable with some construction disruption in exchange for value capture Example: Bidadari (The “Cemetery” Mispricing) When The Woodleigh Residences launched in 2019 at about $1,733 psf, public perception lagged reality. Many still anchored on the old “cemetery” identity. But the physical signals were already strong: - MRT presence and connectivity were real - Roads were being realigned and infrastructure works were tangible - BTO completions were bringing in residents and demand fundamentals A reported outcome: ~$660,000 profit—generated not by buying a finished estate, but by buying during Physical Certainty, before broad-market pricing fully adjusted to the new reality. Example: Lentor (Certainty Compression in Real Time) With the Thomson–East Coast Line (TEL) and the area’s redevelopment momentum, Lentor illustrates how pricing can escalate as certainty increases: - Early launches price in “potential” - Later launches price in “proof” (transport reliability, buyer adoption, comparable transactions) - Each new delivery milestone compresses the uncertainty discount further Key takeaway: In districts like Lentor, the biggest jumps typically come as the MRT and surrounding projects transition from plan → operation → lived experience. Stage 3 — Lifestyle Certainty (Final Entry): “Complete, Convenient, Premium” What it looks like - Area is fully developed - Amenities are complete (retail, schools, parks, transport integration) - A vibrant community exists (the place has identity and habit) - Rental demand is stable, and owner-occupier willingness to pay is high Why profits are solid but moderate By Stage 3, you are paying for: - certainty - convenience - comfort - a proven neighbourhood The trade-off is that the explosive repricing has usually already happened. Returns can still be good, but the entry price is higher, and incremental gains are often steadier rather than outsized. Who Stage 3 is for - Owner-occupiers prioritizing quality of life and predictability - Investors seeking stability, easier leasing, lower “execution risk” - Buyers who prefer to pay a premium to avoid transformation disruption Example: East Coast (Finished-Neighbourhood Premium) Examples cited: - Liv @ MB buyers averaged about $275K–$354K profit - Amber Park averaged about $264K–$536K These are respectable outcomes—but the entry pricing tells the story: - Buyers entered around $2,368–$2,479 psf, substantially higher than Woodleigh’s earlier $1,733 psf Interpretation: East Coast reflects Lifestyle Certainty—strong, proven demand and good profits, but much of the “transformation alpha” is already captured in the price you pay. --- The Core Insight: Markets Don’t Reprice Once—They Reprice Three Times You can think of the transformation cycle as three separate repricing events: 1. Planning Certainty: repricing begins quietly (only some buyers act) 2. Physical Certainty: repricing accelerates (evidence converts skeptics) 3. Lifestyle Certainty: repricing stabilizes (premium for completion, not potential) The most consistent outperformance tends to occur when you enter before the crowd upgrades its confidence—but after enough proof exists to meaningfully reduce downside risk. That is why Stage 2 is often the “sweet spot.” --- How to Use This Framework (Practical Checklist) In Summary, ### Chart Summary: Risk, Upside, and Typical Buyer Profiles The graphic breaks a property/opportunity into three lenses—**Risk**, Upside, and Typical Buyer—using “certainty” levels to show what is most/least predictable and where the value potential sits. 1) Risk (left pie) Risk is driven mainly by planning certainty: - High Planning Certainty (largest share): The dominant risk factor relates to the planning/entitlement environment (e.g., approvals, zoning, allowable uses). Even with “high certainty,” planning outcomes still represent the biggest risk component relative to the others. - Moderate Physical Certainty (mid share): Site/building conditions are somewhat knowable (e.g., condition, access, services, construction complexity), creating a moderate level of risk. - Low Lifestyle Certainty (smallest share): Lifestyle/amenity or “place experience” factors are least certain (e.g., neighborhood perception, livability, demand drivers tied to lifestyle), adding a smaller—but less predictable—risk portion. Interpretation: Overall risk is weighted toward planning/entitlement considerations, with physical factors secondary and lifestyle factors the least represented but more uncertain. 2) Upside (middle pie) Upside is where certainty translates into value creation potential: - Highest Planning Certainty (large share): The strongest upside comes from planning-related confidence—when the planning path is clear, the ability to execute and capture value is greatest. - High Physical Certainty (moderate-to-large share): Solid knowledge of the physical asset/site supports upside (e.g., deliverability, cost control, feasibility). - Moderate Lifestyle Certainty (moderate share): Lifestyle demand is a meaningful contributor to upside, but only moderately certain—suggesting upside exists, though it depends more on market sentiment and buyer preferences. Interpretation: Value potential is led by planning clarity, supported by physical deliverability, with lifestyle demand contributing but less reliably. 3) Typical Buyer Profiles (right panel) Based on that risk/upside mix, the likely buyers fall into three groups: 1. Long-Horizon Investors – Buyers comfortable holding through cycles and timelines, often prioritizing durable, long-term value. 2. Growth-Focused Buyers / Investors – Buyers seeking appreciation and execution-driven returns, typically attracted to clearer planning and feasible delivery. 3. Owner-Occupiers & Stability Investors – Buyers prioritizing predictability, usability, and steady outcomes (often more sensitive to lifestyle and day-to-day fit). Overall takeaway The chart suggests an opportunity where planning certainty is the main driver of both risk and upside. Physical factors are comparatively well understood, while lifestyle factors are less predictable. As a result, the opportunity appeals to a mix of long-term, growth-oriented, and stability-focused buyers, depending on their tolerance for planning and market-driven uncertainty. 4) In Conclusion (See Below) +++ This topic isn’t related to Feng Shui at all. I’m also not a Real Estate agent. I’m simply, like you, a property buyer who’s interested in property trends in SG. These three stages are very commonly used by many local Realty Agents to explain a property’s profit potential, if any.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.