All Activity

- Past hour

-

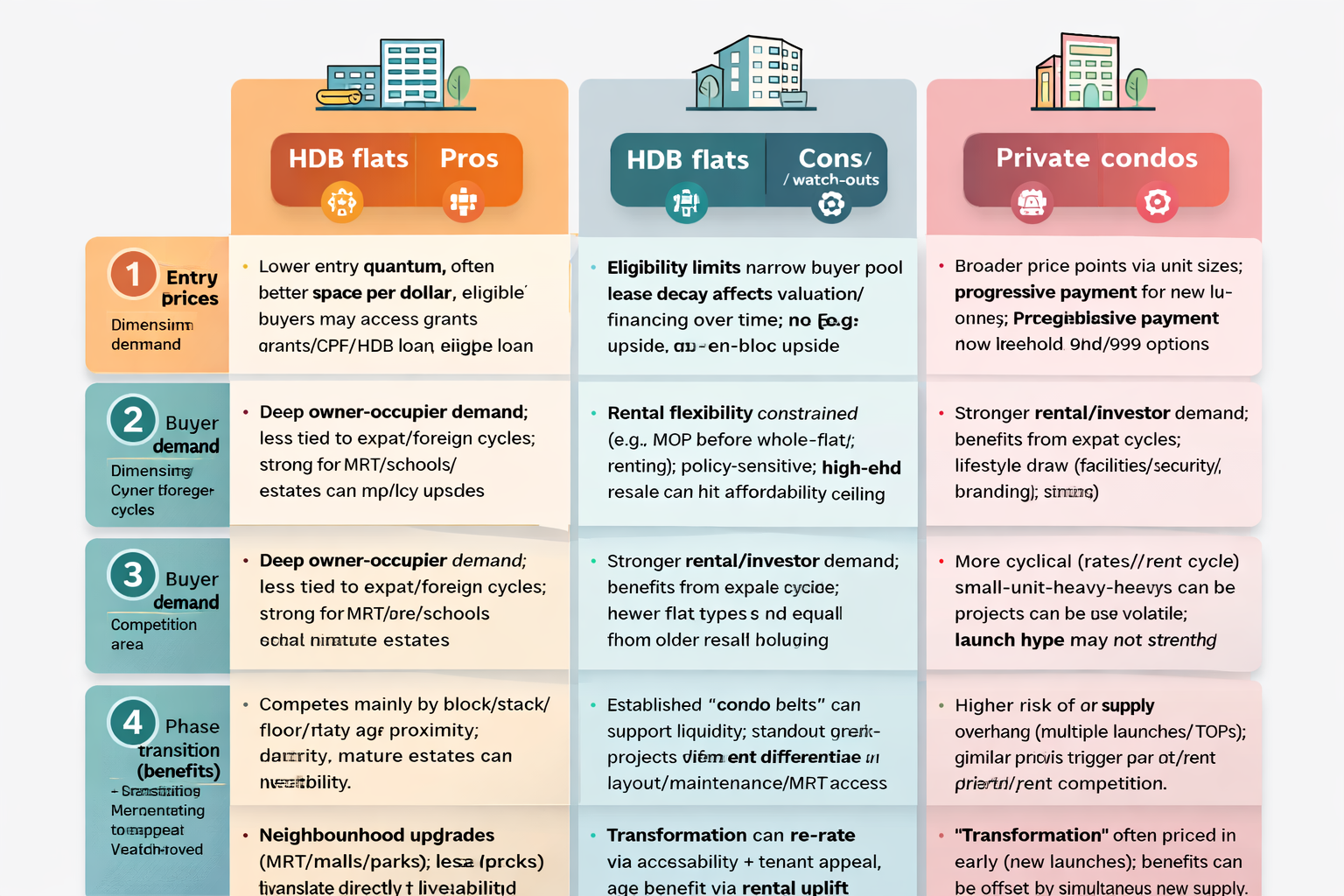

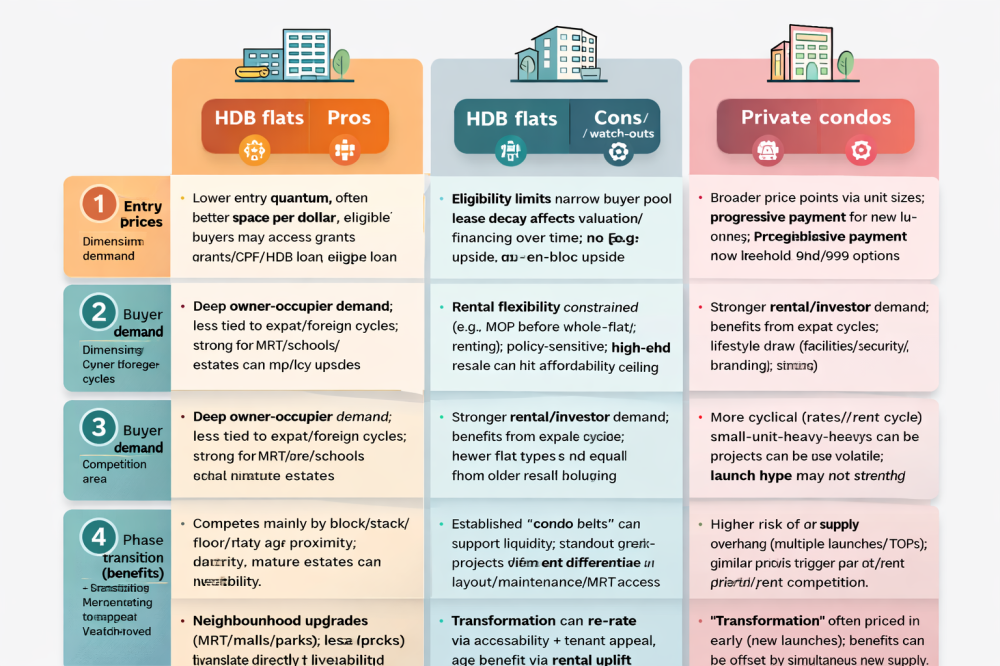

A practical pro and cons review of how Singapore property is often assessed and sometimes marketed by real estate agents, organised around four kEY points. This article will cover what tends to be true, what can be overstated, and what to check to validate the story. 1) Entry Prices Pros (what agents highlight) - “Affordable quantum” even if PSF is high: Smaller units in OCR/RCR can look entry-friendly (e.g., 1–2 bedders). Agents often position this as easier to own/exit. - New-launch pricing clarity: Fixed developer price list, progressive payment scheme, and “fresh lease” are pitched as a premium worth paying. - Resale “value gap”: Resale condos/HDBs in mature estates may look cheaper than nearby new launches on a PSF basis, creating a “relative value” narrative. Cons (real-world friction) - High absolute price levels: Singapore’s base price has risen materially over the past cycle; “entry” is often still a large downpayment + mortgage burden. - Quantum traps: - Small units can have higher PSF and more volatile resale demand (investor-led, tenant-led). - Maintenance fees can be disproportionately painful for small units. - Lease/tenure penalty: - Older leasehold properties can face financing constraints and valuation sensitivity as lease decays (especially for older HDBs and older leasehold condos). - Policy/financing constraints: - ABSD, TDSR/MSR, and LTV limits can make “cheap entry” less meaningful if you’re constrained by eligibility or total debt servicing. What to check (quick validation) - Compare quantum, PSF, and maintenance fees side-by-side for the same unit type. - Review recent caveats (URA Realis) for actual transacted prices, not just asking prices. - For older assets: check remaining lease, recent bank valuations, and resale time-on-market. --- 2) Buyer Demand Pros (common demand drivers) - Owner-occupier base demand: Singapore has structurally strong owner-occupier preference (especially for well-located resale and family-sized layouts). - Rental market supports investors (cyclical, but can be strong): Proximity to MRT/business nodes/schools often sustains rental demand. - Scarcity narratives: “Mature estate, limited supply” can be real in some pockets, supporting resale liquidity. Cons (where demand can be overstated) - Demand is segmented: - 1-bedders are often investor/tenant-driven; demand can drop fast if yields compress or policies tighten. - Large units rely on affluent upgrader demand which is sensitive to interest rates and stock-market sentiment. - New-launch demand can be “event-driven”: - Strong launch weekend take-up doesn’t always translate to strong resale premiums later, especially if many similar projects TOP together. - Foreign demand is policy-sensitive: - High ABSD for foreigners means foreign buyer demand is concentrated in specific segments and can switch off quickly. What to check - Track transaction volume trends (not just price) in the last 6–12 months. - For investment: test net yield after maintenance, property tax, agent fees, vacancy assumptions. - For family demand: check school zone reality (1km rules), actual walk time to MRT, and nearby amenity maturity. --- 3) Competition Within the Area Pros (how competition can help) - Cluster effect: Multiple condos in an area can create a known “condo belt” that attracts tenants and buyers (more comparables, more visibility). - Amenity build-out: Competition among developers/MCSTs can improve landscaping, facilities, and upkeep standards—helping perceived value. Cons (most important risk) - Supply overhang / “cannibalisation”: - If multiple projects launch or TOP around the same time, you can see resale price stagnation and rental competition (landlords undercut each other). - Similar product problem: - If nearby projects offer similar layouts/size/pricing, your unit’s differentiation is weak—buyers pick based on price, squeezing upside. - Exit liquidity varies by stack and layout: - Even in a “hot area,” odd layouts, poor facing, road noise, or weak stack positioning can face much slower resale. What to check - Look up the pipeline: GLS sites, upcoming launches, and estimated TOP dates within ~1–3 km. - Compare unit mix (how many 1/2/3-bedders) across projects—this predicts resale and rental competition. - Observe rental listings (number of competing listings + asking rents) to gauge landlord competition. --- 4) Phases of Transformation Agents frequently sell a “transformation story.” This can be valid—but timing matters. Typical phases (and what they mean for buyers) Phase 1: Announcement / Masterplan headline (0–2 years) - Pros: Sentiment uplift; “early-bird” narrative; some price repricing happens quickly if the plan is credible. - Cons: Most of the gain can be front-loaded; execution risk is high; details are often vague. Phase 2: Infrastructure commitment (2–6 years) - Examples: confirmed MRT line/station, major road links, institutional anchors. - Pros: Real improvement in accessibility; demand broadens; rental appeal can improve. - Cons: Construction noise/dust; detours; liveability dips short-term; “buy the rumour, sell the news” risk. Phase 3: Commercial/amenity activation (5–10+ years) - Examples: malls, offices, parks, schools, healthcare nodes actually open and operate. - Pros: Strongest fundamental support for both owner-occupiers and tenants; resale liquidity tends to improve. - Cons: By the time benefits are obvious, entry price is usually much higher; upside may be more limited. Phase 4: Maturity / Re-rating stabilises - Pros: More stable demand base; clearer price discovery. - Cons: Growth can slow; you rely more on broader market cycles than “transformation alpha.” Singapore examples of transformation narratives (illustrative) - Jurong Lake District / 2nd CBD influence on nearby OCR/RCR nodes. - Greater Southern Waterfront long-horizon uplift narrative for city fringe/southern corridor. - Punggol Digital District and surrounding Punggol/Sengkang rental/owner demand themes. - Tengah new town (longer ramp-up; amenity maturity is the key risk early on). - New MRT lines / station additions (e.g., Cross Island Line and extensions) often drive micro-market repricing—timing matters most. What to check - Confirm whether the “transformation” is funded and scheduled (not just conceptual). - Map walkability (true 8–10 min walk vs “one traffic light away” marketing). - Assess whether your holding period matches the transformation timeline (e.g., 3 years vs 10 years). --- ## A quick “agent claims” checklist (to keep it grounded) - Ask for 3 nearest comparable transactions in the last 3 months (same size, same project/nearby). - Ask what new supply is coming within 24–48 months. - Ask what the exit buyer is (upgrader? investor? family?) and whether the unit mix supports that. - Stress test at higher interest rates and more conservative rents. --- Here’s how the same “pros/cons” framework typically differs between HDB flats and private condos in Singapore. 1) Entry Prices HDB flats Pros - Lower entry quantum (especially non-mature estates) and often better $/sqft for space. - More financing support/affordability levers for eligible buyers (CPF usage; grants for eligible first-timers; HDB loan option for some). - Resale price discovery is clearer because the buyer pool is mostly owner-occupiers. Cons - Eligibility constraints (citizenship, family nucleus, income ceilings for some schemes) can limit who can buy. - Lease decay matters more visibly over time (and can affect financing/CPF usage depending on remaining lease and buyer age). - Less “asset enhancement” optionality (no renovation-to-luxury positioning that shifts a whole project’s brand; no en-bloc). ### Private condos Pros - Broader buyer pool (Singaporeans, PRs, and—policy-dependent—foreigners) supports liquidity in some segments. - Wider product range (small units for lower quantum entry; new launches with progressive payment). - Freehold/999 options (where available) can support long-hold narratives. Cons - Higher entry cost (downpayment + typically higher absolute prices). - ABSD exposure is a bigger deal for many condo buyers (2nd/3rd property, PR/foreigner). - Ongoing costs: maintenance fees, sinking fund, and higher frictional costs can erode returns, especially for small units. --- 2) Buyer Demand HDB flats Pros - Deep, stable owner-occupier demand (family formation, upgrader flow from smaller flats). - Less sensitive to “luxury cycles” and foreign buyer sentiment. - Certain locations (near MRT, schools, mature estates) enjoy very consistent resale interest. Cons - Rental demand is constrained by rules (e.g., Minimum Occupation Period before renting whole flat; tighter subletting conditions vs condos). - Demand is policy-sensitive (grant changes, HDB supply pipeline, cooling measures). - High-priced resale flats can face affordability ceilings faster because buyers are mainly local income-based households. Private condos Pros - Investor + tenant demand is a core demand pillar (especially near MRT, CBD/fringe, business parks, universities). - Can benefit more directly from expat cycles and rental market upswings. - More “lifestyle” demand: facilities, security, branding. Cons - Demand can be more cyclical (rates, job market, rental cycle). - If a project is dominated by small units/investors, resale can turn more volatile when yields compress. - New-launch demand can be strong at launch but weaker at resale if many similar projects TOP together. --- 3) Competition Within the Area HDB flats Pros - Competition is often more about which block/stack, floor, renovation, and proximity to MRT/amenities, rather than competing “projects.” - In mature estates, limited new HDB resale substitutes can support prices. Cons - BTO/Prime model supply nearby can cap upside for older resale flats (buyers may choose a subsidised new flat if wait-time is acceptable). - Nearby “better” flat types (e.g., newer 4/5-room projects) can pull demand away from older stock. Private condos Pros - Multiple condos nearby create a benchmarking ecosystem (more comps), which can support liquidity if the area is established. - A standout project can differentiate on layout efficiency, maintenance, views, direct MRT link, or full amenities. Cons - Supply overhang risk is higher (GLS sites, multiple launches, and simultaneous TOPs can depress resale and rents). - Projects often compete on very similar features; without differentiation, it becomes a price war at resale or rental. --- 4) Phases of Transformation HDB flats Pros - Transformation (new MRT, mall, park, town centre) tends to translate more directly into owner-occupier convenience value, supporting steady demand. - Upgrading of amenities can improve liveability even if price growth is moderated. Cons - Upside can be bounded by affordability of the core buyer pool and by policy settings. - Lease age remains a structural headwind for older flats even if the neighbourhood improves. Private condos Pros - Transformation can create outsized re-rating if it materially improves tenant appeal (new MRT, office nodes, lifestyle hubs). - More able to monetise transformation through rental uplift and broader buyer segments. Cons - Transformation gains can be priced in early (especially new launches marketed on future plans). - If transformation coincides with heavy new supply, the benefit can be offset by competition (more units chasing the same tenants/buyers). --- Practical takeaway - HDB: generally stronger on affordability + stable owner-occupier demand, weaker on policy/eligibility constraints + lease decay + limited rental flexibility. - Condo: stronger on rental/investor optionality + broader buyer pool + transformation-driven re-rating, weaker on higher entry costs/ABSD + supply competition + higher holding costs.

- Yesterday

-

Source & Credit:

-

It seems not everyone agrees with the above. Please keep in mind: it depends.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

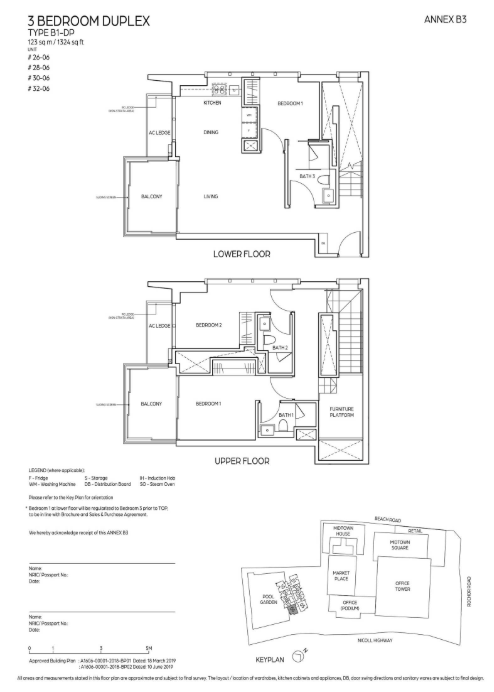

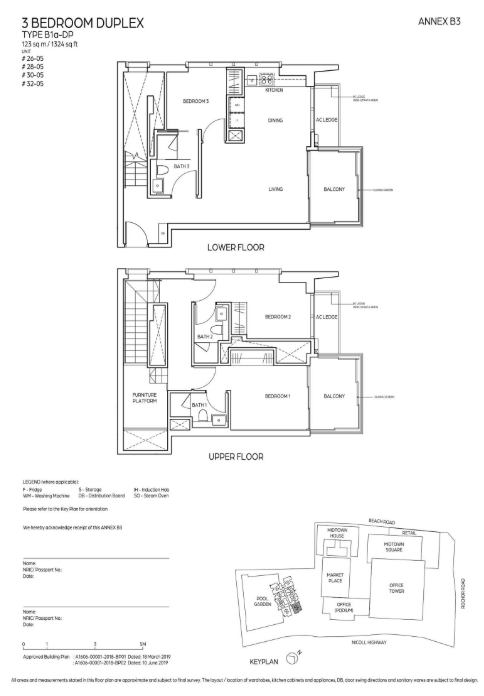

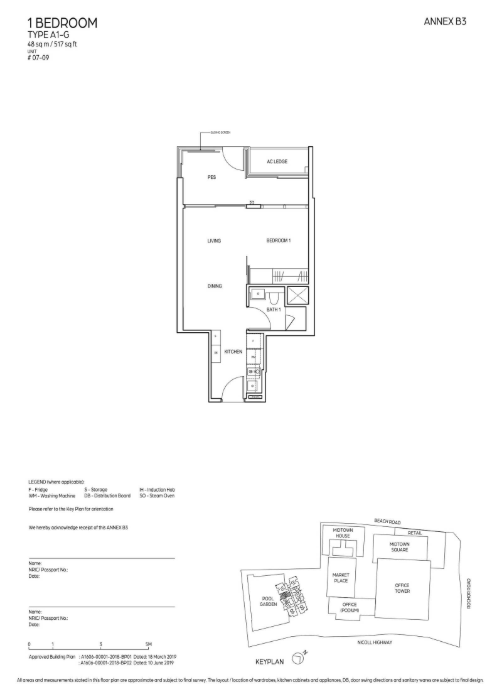

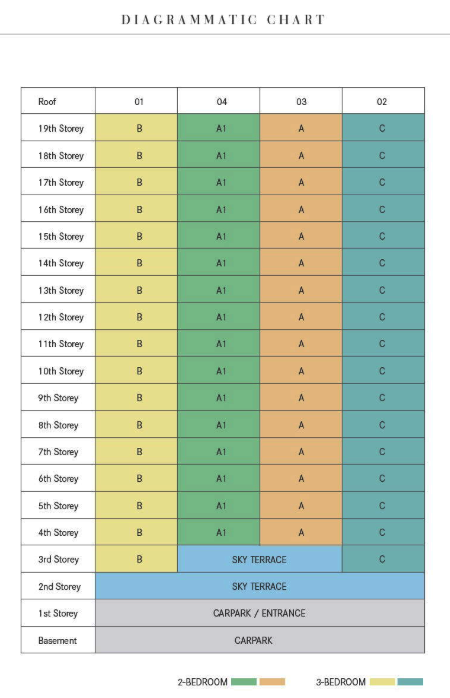

3 Bedroom Duplex

-

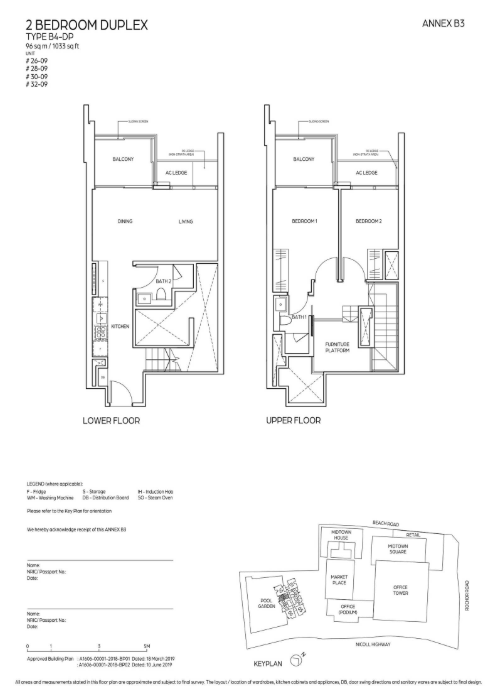

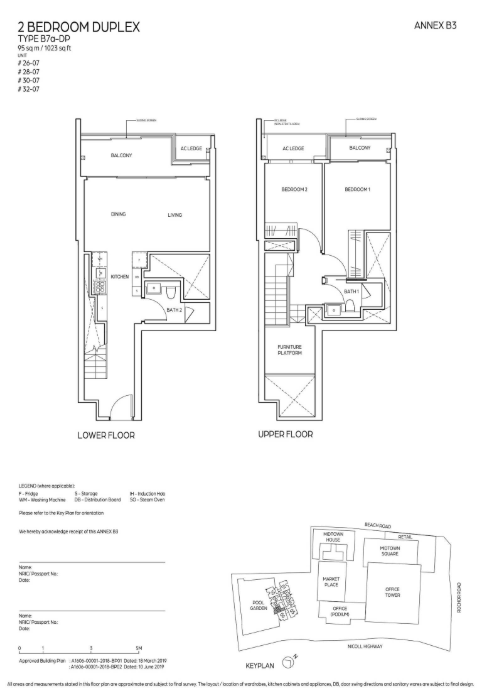

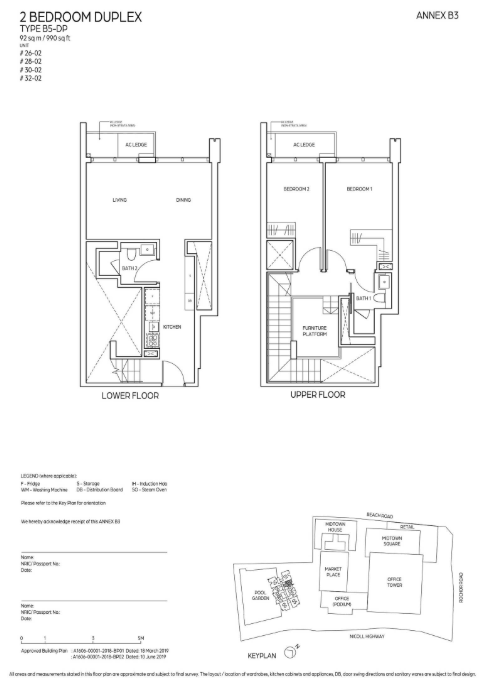

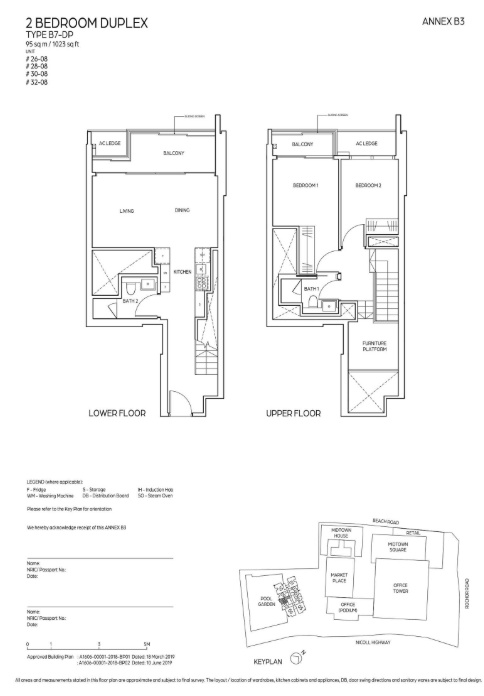

2 Bedroom Duplex

-

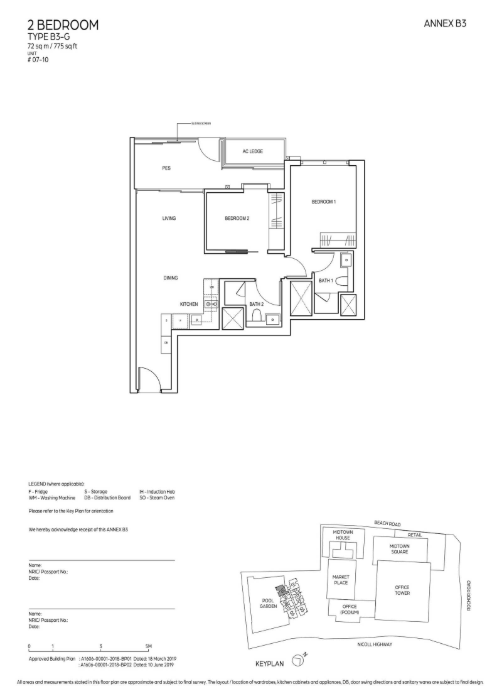

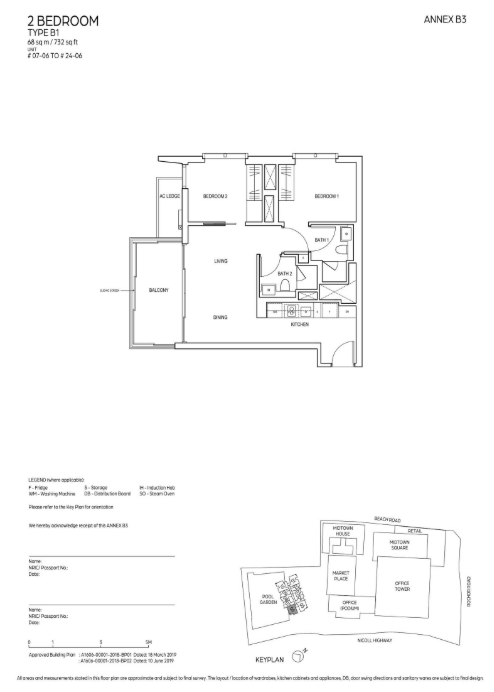

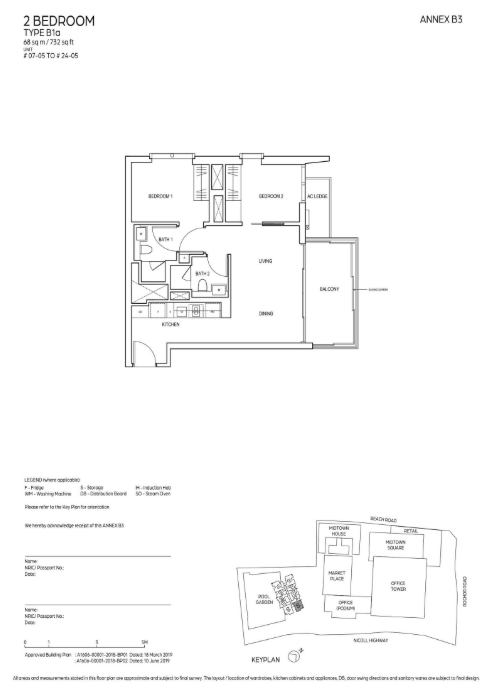

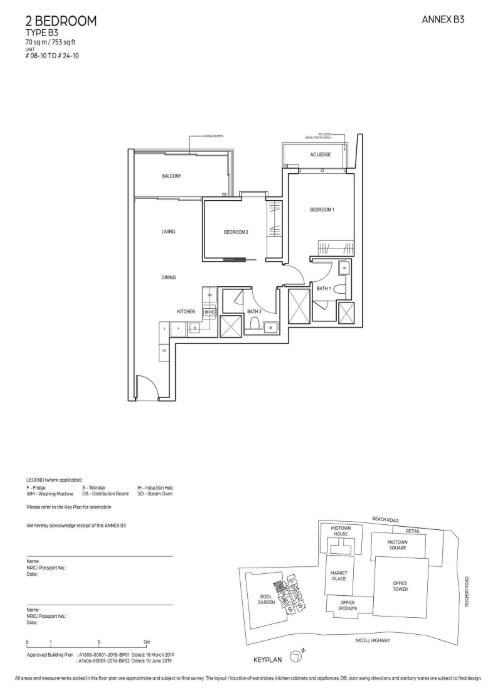

2 Bedroom

-

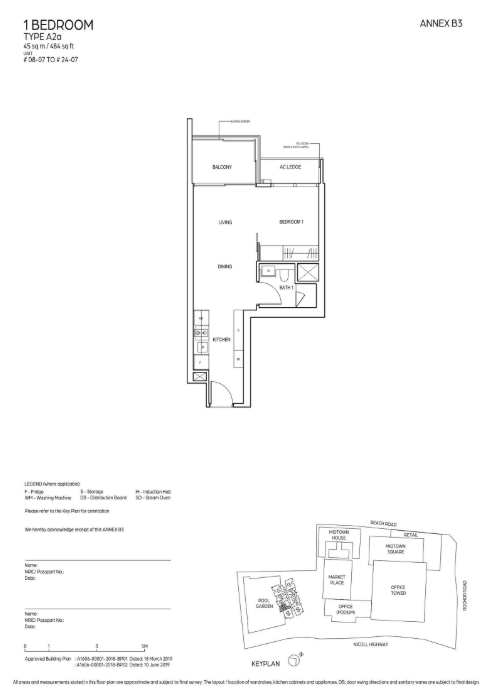

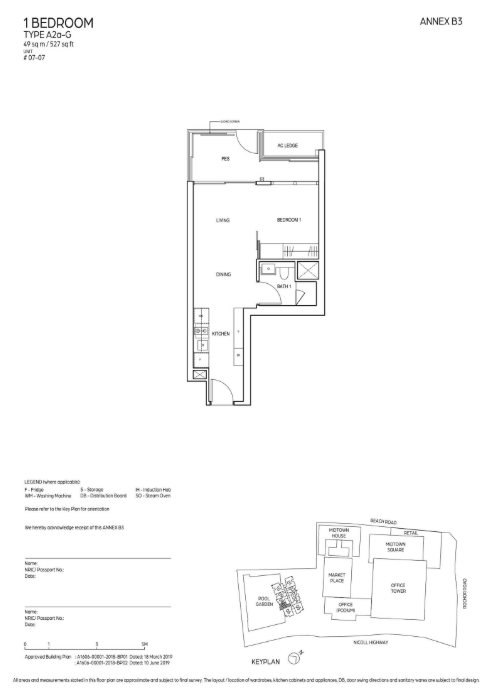

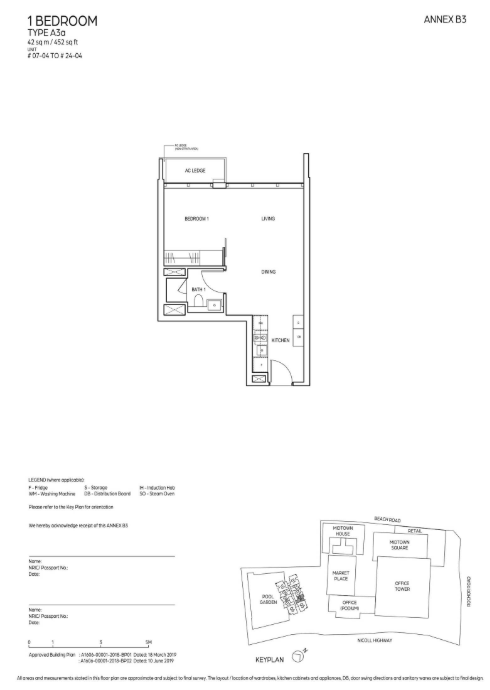

1 Bedroom

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

-

Thinking about buying a home that faces the afternoon sun? BUT +++

-

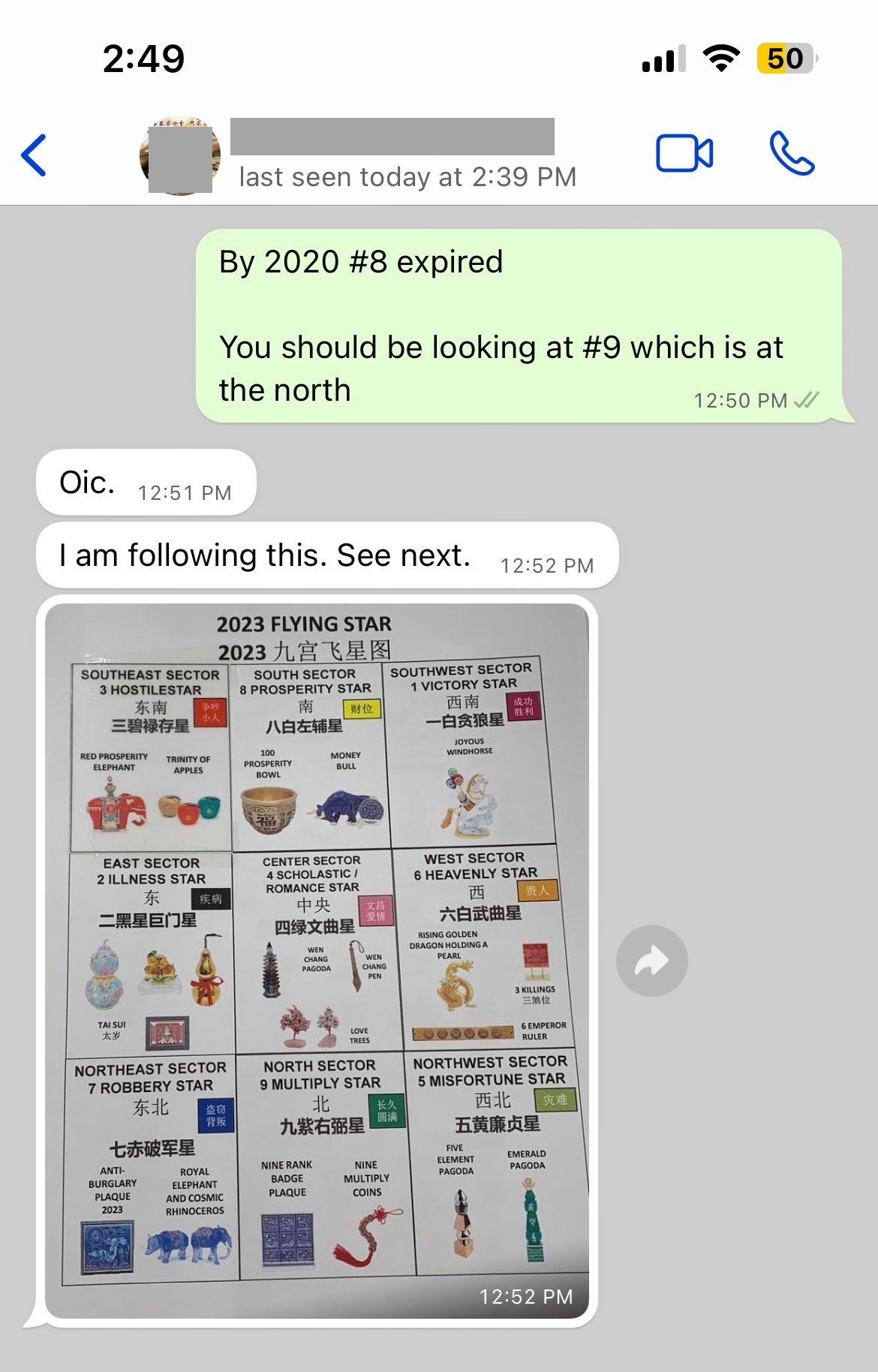

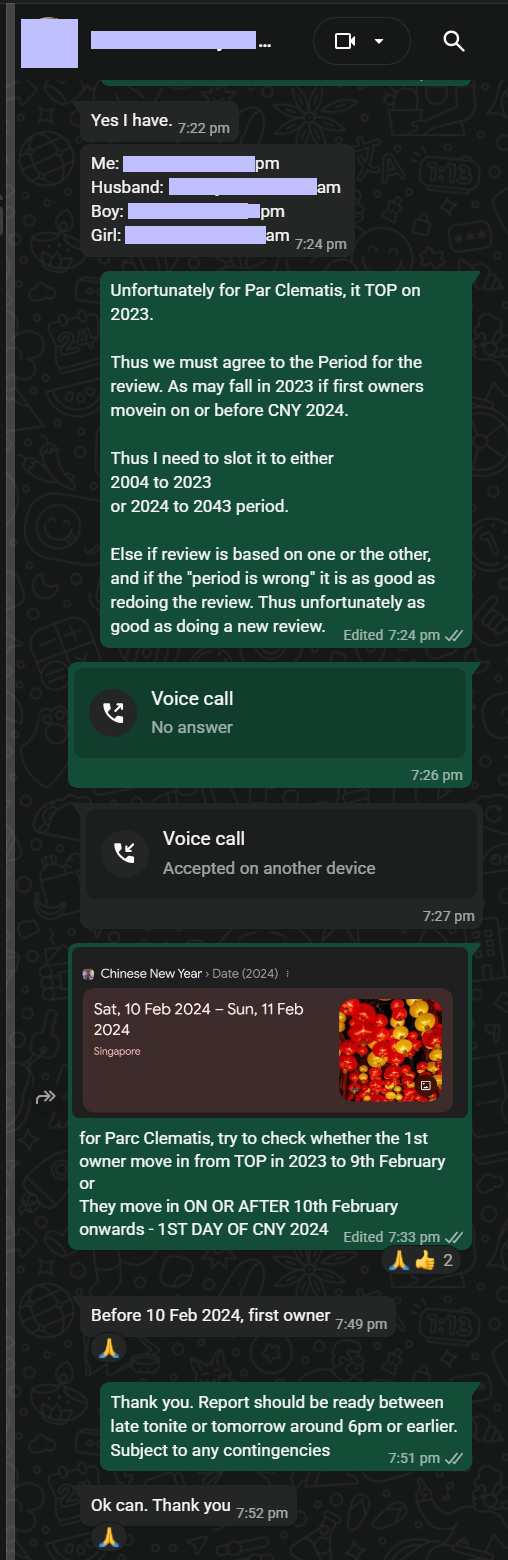

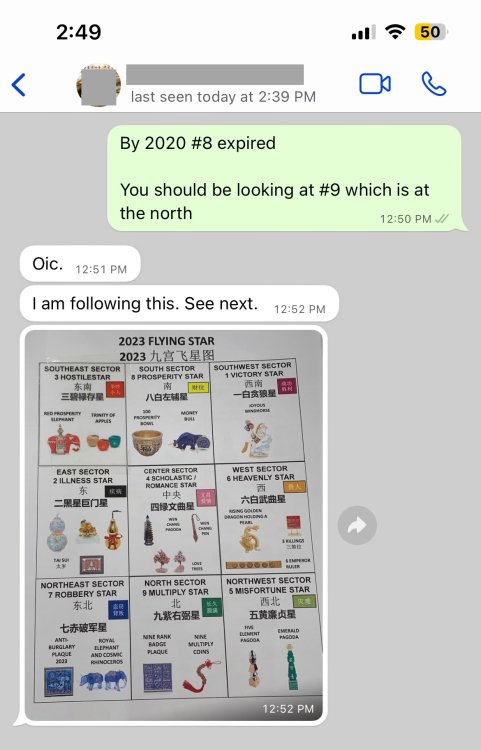

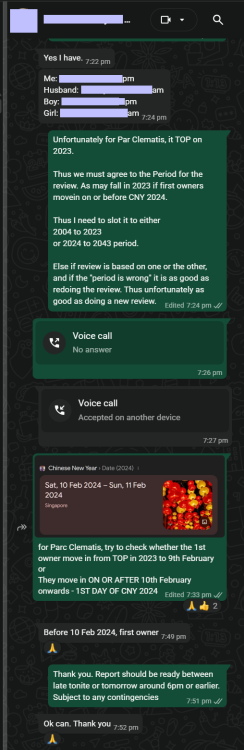

TOP in 2023 - If you move in on or before CNY 2024 (9 February 2024 or earlier), use Period 8 Feng Shui. If the first owner moves in on or after 10 February 2024, use Period 9 Feng Shui. More AN EXAMINATION OF WHICH FLYING STAR PERIOD ONE SHOULD UTILIZE? +++ Which Flying Star Period to Use? For example, take a look at Treasure @ Tampines The transition of Feng Shui Qi is significant in the context of the Chinese New Year 2024, as it influences the energy dynamics within a space. The timing of when a unit is first occupied plays a crucial role in determining its Flying Star Feng Shui. This means that the specific day of occupancy will affect the energetic quality and overall Feng Shui of the unit, highlighting the importance of timing in Feng Shui practices. Understanding these elements can help individuals optimize their living environments in alignment with the changing energies associated with the New Year. +++ When did the first owner/resident/tenant take residence in the unit at Treasure @ Tampines? +++ EITHER Can be the owner, resident or a tenant OR Can be the owner, resident or a tenant REGARDLESS, UNITS FACING NORTH POSSESS A POSITIVE FENG SHUI OVERALL How do you Feng Shui your home? Use your front door? Who are the Conservatives & the Modernist? +++ For Parc Clematis, for example, many collected their keys in 2023. However, some may choose to move in on or after CNY 2024. +++ Cecil Lee, Geomancy.net

-

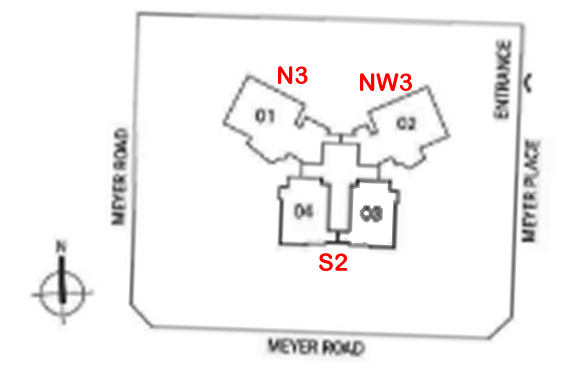

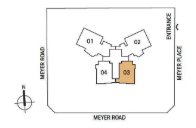

One Meyer Site Plan

-

One Meyer Site Plans

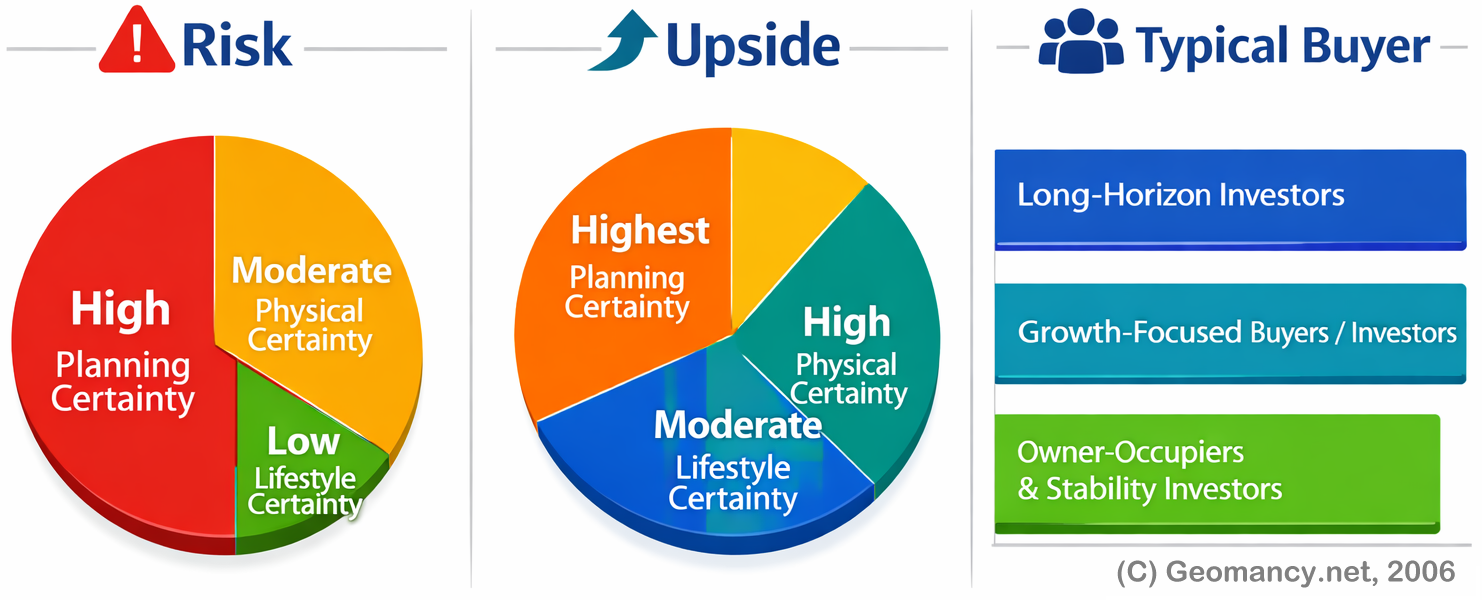

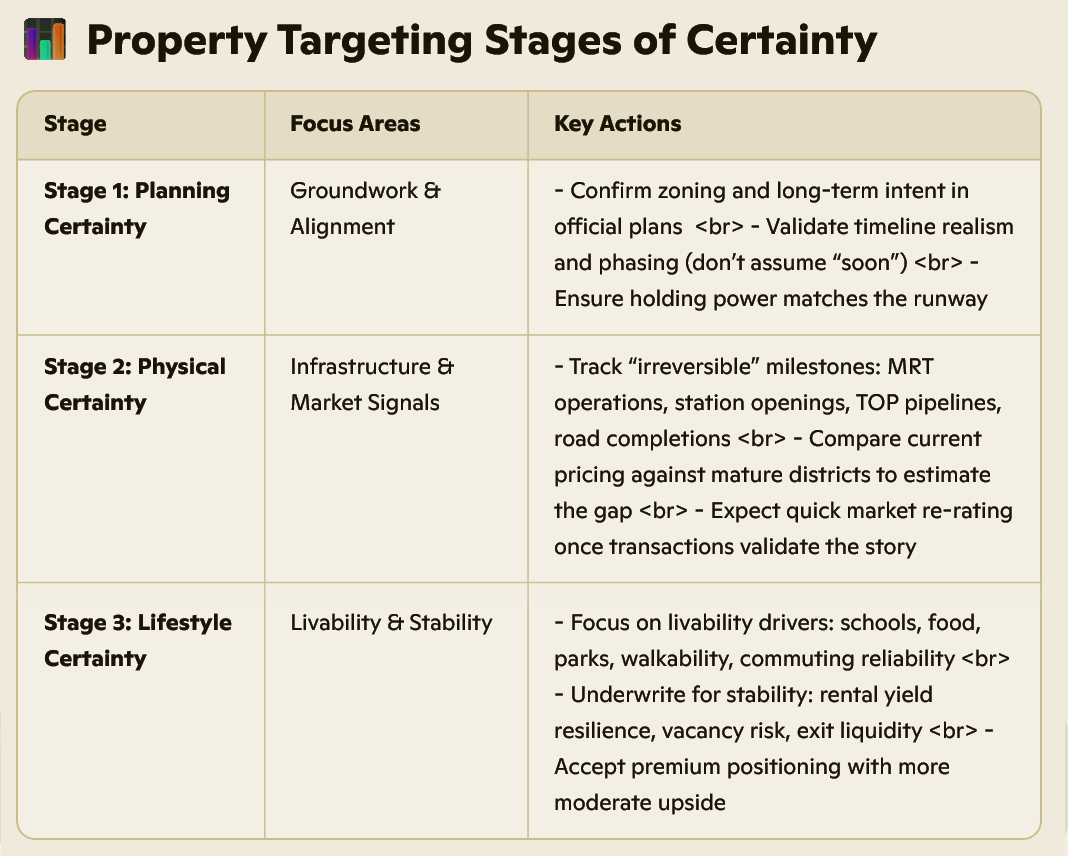

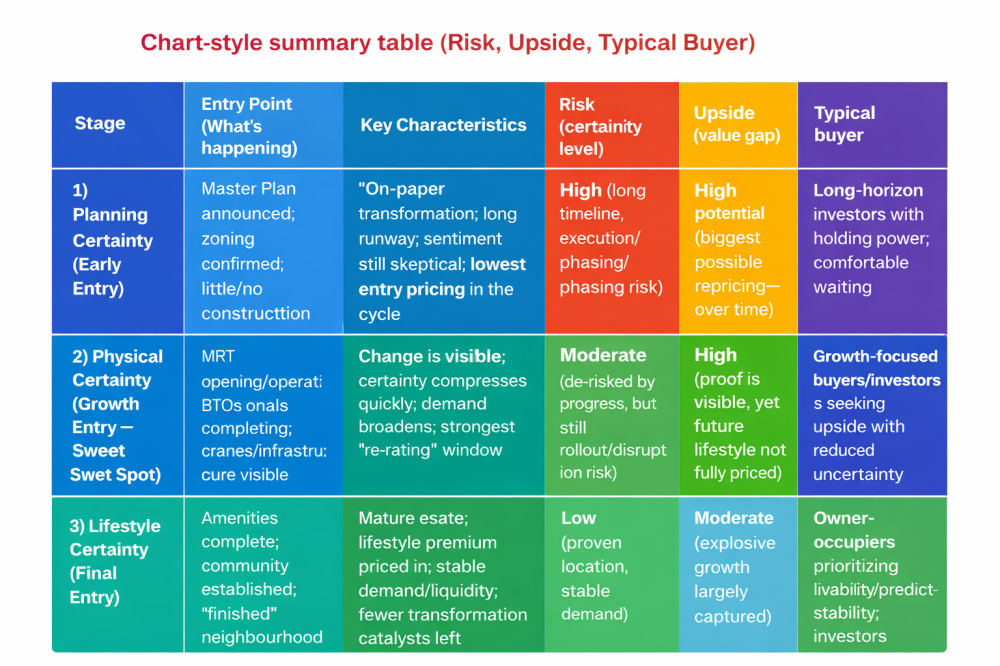

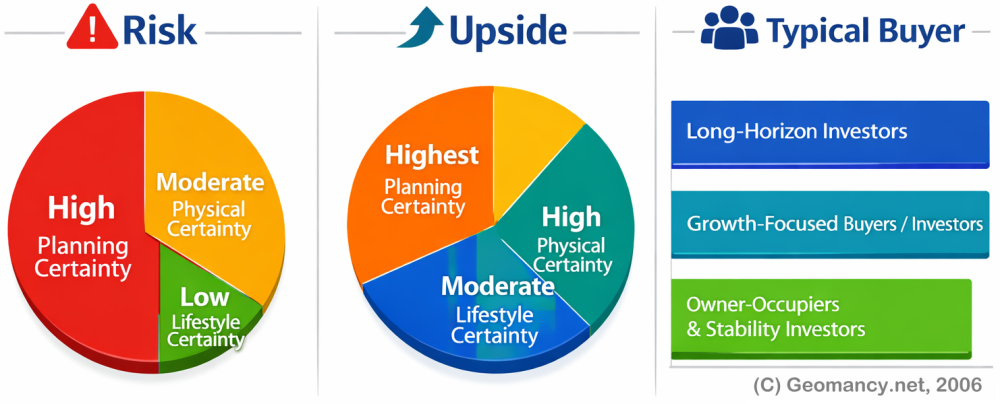

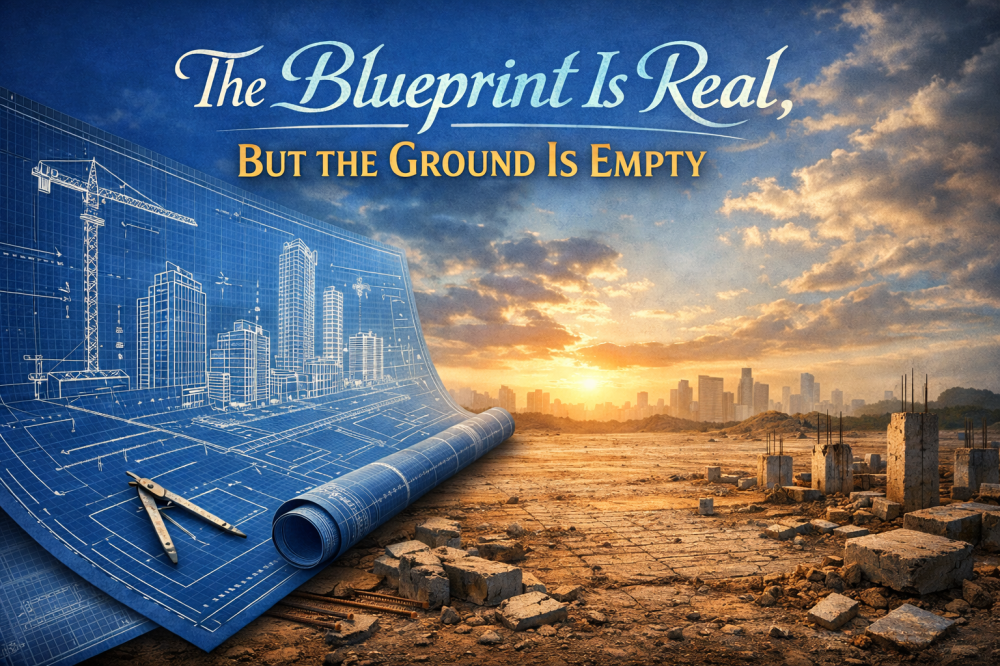

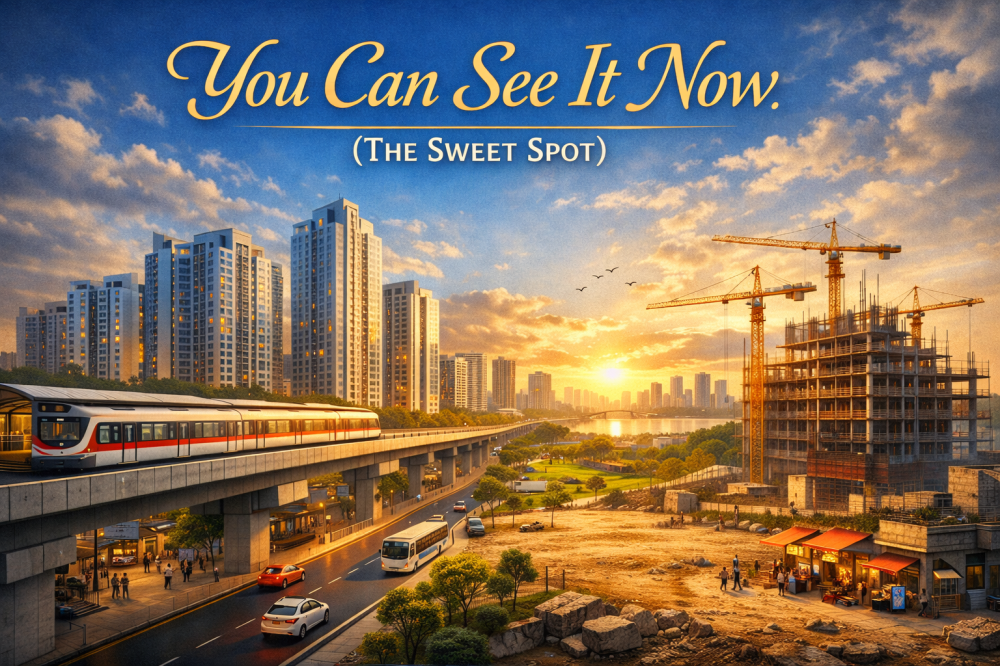

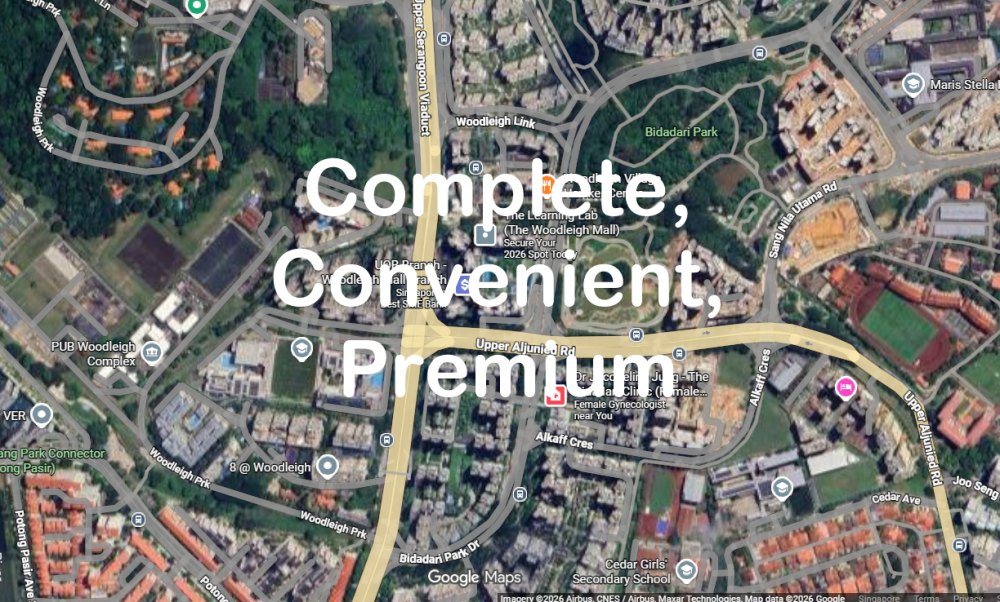

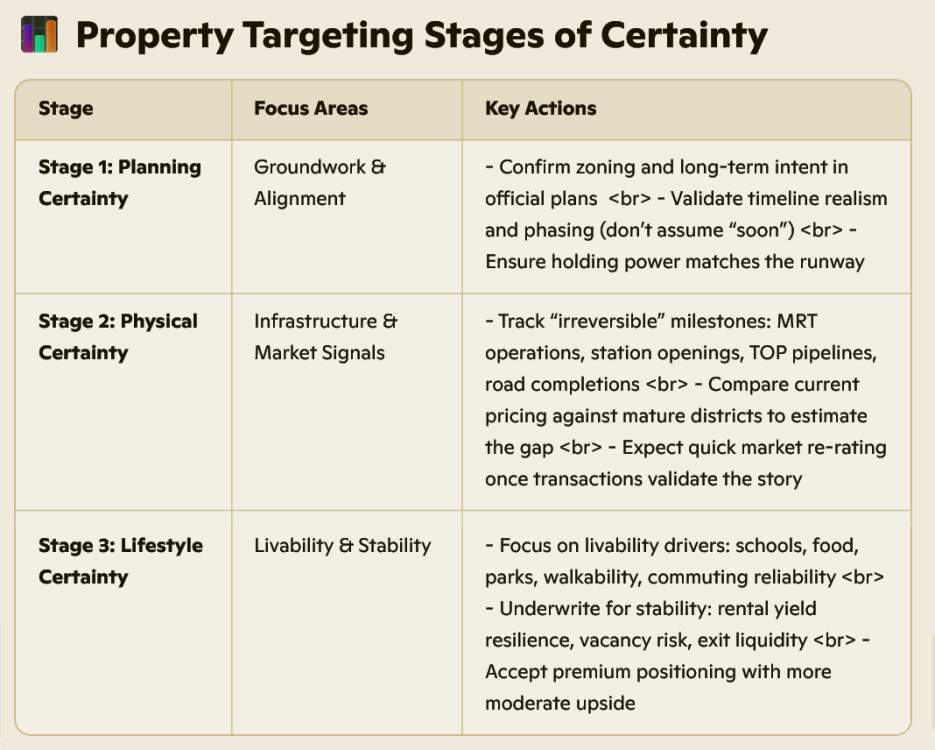

+++ The 3 Certainties of Property Transformation: A Professional Framework for Timing Your Entry The 3 Signals: When to Enter Real estate outperformance is rarely about “finding a cheap unit.” It is more often about entering a location at the right point in its transformation cycle—when the market has not yet fully priced in what is coming, but the probability of change is rising. A practical way to time this is to track three escalating forms of certainty: 1. Planning Certainty (Early Entry) 2. Physical Certainty (Growth Entry — the Sweet Spot) 3. Lifestyle Certainty (Final Entry) Each stage carries a different risk profile, valuation logic, and profit potential. The investors who consistently do well are not guessing the future—they are buying certainty before it becomes consensus. Since 1996, (C) Geomancy.net Stage 1 — Planning Certainty (Early Entry): “The Blueprint Is Real, But the Ground Is Empty” What it looks like - Government master plan announced - Zoning confirmed, land use intentions clarified - Nothing built yet (or minimal enabling works) - The narrative is strong, but proof on the ground is limited Why prices are lowest here At this stage, the market discounts heavily because the timeline is long and outcomes feel abstract. Even if the plan is credible, buyers price in: - execution risk (delays, phasing, policy shifts) - opportunity cost (capital tied up for years) - uncertainty around the eventual “vibe” of the area Result: This stage often offers the lowest entry prices in the entire cycle. Who Stage 1 is for - Investors with long holding power - Buyers comfortable with “paper certainty” and longer waits - Portfolios that can tolerate slower initial appreciation Example: Paya Lebar Airbase (PLA) - Announced in 2013, reinforced by planning clarity including the 2025 Master Plan - Approximately 800 hectares of future mixed-use development - Connectivity uplift (e.g., Cross Island Line integration) - Major development expected to ramp in the 2030s Interpretation: This is classic Planning Certainty—arguably the lowest-cost point of entry, but also the longest runway. Stage 2 — Physical Certainty (Growth Entry): “You Can See It Now” (The Sweet Spot) One of the most often-quoted examples in the recent past was Bidahari Estate. What it looks like - MRT stations opening or operational - BTO projects completing, population starting to form - Cranes are up (active construction, visible delivery) - Roads, bridges, parks, and commercial nodes are clearly taking shape This is the inflection point where the market shifts from believing to recognizing. Why this stage tends to produce the biggest profits Stage 2 is where you often get the best mix of: - de-risking (proof replaces speculation) - still-wide valuation gap (future amenities are not fully priced) - accelerating demand (buyers upgrade their confidence) In simple terms: the discount for uncertainty shrinks rapidly, but the neighbourhood is not “finished”—so you are not yet paying the full lifestyle premium. Who Stage 2 is for - Buyers seeking strong upside with reduced uncertainty - Investors who want to ride the re-rating phase (not just wait for completion) - Owners comfortable with some construction disruption in exchange for value capture Example: Bidadari (The “Cemetery” Mispricing) When The Woodleigh Residences launched in 2019 at about $1,733 psf, public perception lagged reality. Many still anchored on the old “cemetery” identity. But the physical signals were already strong: - MRT presence and connectivity were real - Roads were being realigned and infrastructure works were tangible - BTO completions were bringing in residents and demand fundamentals A reported outcome: ~$660,000 profit—generated not by buying a finished estate, but by buying during Physical Certainty, before broad-market pricing fully adjusted to the new reality. Example: Lentor (Certainty Compression in Real Time) With the Thomson–East Coast Line (TEL) and the area’s redevelopment momentum, Lentor illustrates how pricing can escalate as certainty increases: - Early launches price in “potential” - Later launches price in “proof” (transport reliability, buyer adoption, comparable transactions) - Each new delivery milestone compresses the uncertainty discount further Key takeaway: In districts like Lentor, the biggest jumps typically come as the MRT and surrounding projects transition from plan → operation → lived experience. Stage 3 — Lifestyle Certainty (Final Entry): “Complete, Convenient, Premium” What it looks like - Area is fully developed - Amenities are complete (retail, schools, parks, transport integration) - A vibrant community exists (the place has identity and habit) - Rental demand is stable, and owner-occupier willingness to pay is high Why profits are solid but moderate By Stage 3, you are paying for: - certainty - convenience - comfort - a proven neighbourhood The trade-off is that the explosive repricing has usually already happened. Returns can still be good, but the entry price is higher, and incremental gains are often steadier rather than outsized. Who Stage 3 is for - Owner-occupiers prioritizing quality of life and predictability - Investors seeking stability, easier leasing, lower “execution risk” - Buyers who prefer to pay a premium to avoid transformation disruption Example: East Coast (Finished-Neighbourhood Premium) Examples cited: - Liv @ MB buyers averaged about $275K–$354K profit - Amber Park averaged about $264K–$536K These are respectable outcomes—but the entry pricing tells the story: - Buyers entered around $2,368–$2,479 psf, substantially higher than Woodleigh’s earlier $1,733 psf Interpretation: East Coast reflects Lifestyle Certainty—strong, proven demand and good profits, but much of the “transformation alpha” is already captured in the price you pay. --- The Core Insight: Markets Don’t Reprice Once—They Reprice Three Times You can think of the transformation cycle as three separate repricing events: 1. Planning Certainty: repricing begins quietly (only some buyers act) 2. Physical Certainty: repricing accelerates (evidence converts skeptics) 3. Lifestyle Certainty: repricing stabilizes (premium for completion, not potential) The most consistent outperformance tends to occur when you enter before the crowd upgrades its confidence—but after enough proof exists to meaningfully reduce downside risk. That is why Stage 2 is often the “sweet spot.” --- How to Use This Framework (Practical Checklist) In Summary, ### Chart Summary: Risk, Upside, and Typical Buyer Profiles The graphic breaks a property/opportunity into three lenses—**Risk**, Upside, and Typical Buyer—using “certainty” levels to show what is most/least predictable and where the value potential sits. 1) Risk (left pie) Risk is driven mainly by planning certainty: - High Planning Certainty (largest share): The dominant risk factor relates to the planning/entitlement environment (e.g., approvals, zoning, allowable uses). Even with “high certainty,” planning outcomes still represent the biggest risk component relative to the others. - Moderate Physical Certainty (mid share): Site/building conditions are somewhat knowable (e.g., condition, access, services, construction complexity), creating a moderate level of risk. - Low Lifestyle Certainty (smallest share): Lifestyle/amenity or “place experience” factors are least certain (e.g., neighborhood perception, livability, demand drivers tied to lifestyle), adding a smaller—but less predictable—risk portion. Interpretation: Overall risk is weighted toward planning/entitlement considerations, with physical factors secondary and lifestyle factors the least represented but more uncertain. 2) Upside (middle pie) Upside is where certainty translates into value creation potential: - Highest Planning Certainty (large share): The strongest upside comes from planning-related confidence—when the planning path is clear, the ability to execute and capture value is greatest. - High Physical Certainty (moderate-to-large share): Solid knowledge of the physical asset/site supports upside (e.g., deliverability, cost control, feasibility). - Moderate Lifestyle Certainty (moderate share): Lifestyle demand is a meaningful contributor to upside, but only moderately certain—suggesting upside exists, though it depends more on market sentiment and buyer preferences. Interpretation: Value potential is led by planning clarity, supported by physical deliverability, with lifestyle demand contributing but less reliably. 3) Typical Buyer Profiles (right panel) Based on that risk/upside mix, the likely buyers fall into three groups: 1. Long-Horizon Investors – Buyers comfortable holding through cycles and timelines, often prioritizing durable, long-term value. 2. Growth-Focused Buyers / Investors – Buyers seeking appreciation and execution-driven returns, typically attracted to clearer planning and feasible delivery. 3. Owner-Occupiers & Stability Investors – Buyers prioritizing predictability, usability, and steady outcomes (often more sensitive to lifestyle and day-to-day fit). Overall takeaway The chart suggests an opportunity where planning certainty is the main driver of both risk and upside. Physical factors are comparatively well understood, while lifestyle factors are less predictable. As a result, the opportunity appeals to a mix of long-term, growth-oriented, and stability-focused buyers, depending on their tolerance for planning and market-driven uncertainty. 4) In Conclusion (See Below) +++ This topic isn’t related to Feng Shui at all. I’m also not a Real Estate agent. I’m simply, like you, a property buyer who’s interested in property trends in SG. These three stages are very commonly used by many local Realty Agents to explain a property’s profit potential, if any.

+++ The 3 Certainties of Property Transformation: A Professional Framework for Timing Your Entry The 3 Signals: When to Enter Real estate outperformance is rarely about “finding a cheap unit.” It is more often about entering a location at the right point in its transformation cycle—when the market has not yet fully priced in what is coming, but the probability of change is rising. A practical way to time this is to track three escalating forms of certainty: 1. Planning Certainty (Early Entry) 2. Physical Certainty (Growth Entry — the Sweet Spot) 3. Lifestyle Certainty (Final Entry) Each stage carries a different risk profile, valuation logic, and profit potential. The investors who consistently do well are not guessing the future—they are buying certainty before it becomes consensus. Since 1996, (C) Geomancy.net Stage 1 — Planning Certainty (Early Entry): “The Blueprint Is Real, But the Ground Is Empty” What it looks like - Government master plan announced - Zoning confirmed, land use intentions clarified - Nothing built yet (or minimal enabling works) - The narrative is strong, but proof on the ground is limited Why prices are lowest here At this stage, the market discounts heavily because the timeline is long and outcomes feel abstract. Even if the plan is credible, buyers price in: - execution risk (delays, phasing, policy shifts) - opportunity cost (capital tied up for years) - uncertainty around the eventual “vibe” of the area Result: This stage often offers the lowest entry prices in the entire cycle. Who Stage 1 is for - Investors with long holding power - Buyers comfortable with “paper certainty” and longer waits - Portfolios that can tolerate slower initial appreciation Example: Paya Lebar Airbase (PLA) - Announced in 2013, reinforced by planning clarity including the 2025 Master Plan - Approximately 800 hectares of future mixed-use development - Connectivity uplift (e.g., Cross Island Line integration) - Major development expected to ramp in the 2030s Interpretation: This is classic Planning Certainty—arguably the lowest-cost point of entry, but also the longest runway. Stage 2 — Physical Certainty (Growth Entry): “You Can See It Now” (The Sweet Spot) One of the most often-quoted examples in the recent past was Bidahari Estate. What it looks like - MRT stations opening or operational - BTO projects completing, population starting to form - Cranes are up (active construction, visible delivery) - Roads, bridges, parks, and commercial nodes are clearly taking shape This is the inflection point where the market shifts from believing to recognizing. Why this stage tends to produce the biggest profits Stage 2 is where you often get the best mix of: - de-risking (proof replaces speculation) - still-wide valuation gap (future amenities are not fully priced) - accelerating demand (buyers upgrade their confidence) In simple terms: the discount for uncertainty shrinks rapidly, but the neighbourhood is not “finished”—so you are not yet paying the full lifestyle premium. Who Stage 2 is for - Buyers seeking strong upside with reduced uncertainty - Investors who want to ride the re-rating phase (not just wait for completion) - Owners comfortable with some construction disruption in exchange for value capture Example: Bidadari (The “Cemetery” Mispricing) When The Woodleigh Residences launched in 2019 at about $1,733 psf, public perception lagged reality. Many still anchored on the old “cemetery” identity. But the physical signals were already strong: - MRT presence and connectivity were real - Roads were being realigned and infrastructure works were tangible - BTO completions were bringing in residents and demand fundamentals A reported outcome: ~$660,000 profit—generated not by buying a finished estate, but by buying during Physical Certainty, before broad-market pricing fully adjusted to the new reality. Example: Lentor (Certainty Compression in Real Time) With the Thomson–East Coast Line (TEL) and the area’s redevelopment momentum, Lentor illustrates how pricing can escalate as certainty increases: - Early launches price in “potential” - Later launches price in “proof” (transport reliability, buyer adoption, comparable transactions) - Each new delivery milestone compresses the uncertainty discount further Key takeaway: In districts like Lentor, the biggest jumps typically come as the MRT and surrounding projects transition from plan → operation → lived experience. Stage 3 — Lifestyle Certainty (Final Entry): “Complete, Convenient, Premium” What it looks like - Area is fully developed - Amenities are complete (retail, schools, parks, transport integration) - A vibrant community exists (the place has identity and habit) - Rental demand is stable, and owner-occupier willingness to pay is high Why profits are solid but moderate By Stage 3, you are paying for: - certainty - convenience - comfort - a proven neighbourhood The trade-off is that the explosive repricing has usually already happened. Returns can still be good, but the entry price is higher, and incremental gains are often steadier rather than outsized. Who Stage 3 is for - Owner-occupiers prioritizing quality of life and predictability - Investors seeking stability, easier leasing, lower “execution risk” - Buyers who prefer to pay a premium to avoid transformation disruption Example: East Coast (Finished-Neighbourhood Premium) Examples cited: - Liv @ MB buyers averaged about $275K–$354K profit - Amber Park averaged about $264K–$536K These are respectable outcomes—but the entry pricing tells the story: - Buyers entered around $2,368–$2,479 psf, substantially higher than Woodleigh’s earlier $1,733 psf Interpretation: East Coast reflects Lifestyle Certainty—strong, proven demand and good profits, but much of the “transformation alpha” is already captured in the price you pay. --- The Core Insight: Markets Don’t Reprice Once—They Reprice Three Times You can think of the transformation cycle as three separate repricing events: 1. Planning Certainty: repricing begins quietly (only some buyers act) 2. Physical Certainty: repricing accelerates (evidence converts skeptics) 3. Lifestyle Certainty: repricing stabilizes (premium for completion, not potential) The most consistent outperformance tends to occur when you enter before the crowd upgrades its confidence—but after enough proof exists to meaningfully reduce downside risk. That is why Stage 2 is often the “sweet spot.” --- How to Use This Framework (Practical Checklist) In Summary, ### Chart Summary: Risk, Upside, and Typical Buyer Profiles The graphic breaks a property/opportunity into three lenses—**Risk**, Upside, and Typical Buyer—using “certainty” levels to show what is most/least predictable and where the value potential sits. 1) Risk (left pie) Risk is driven mainly by planning certainty: - High Planning Certainty (largest share): The dominant risk factor relates to the planning/entitlement environment (e.g., approvals, zoning, allowable uses). Even with “high certainty,” planning outcomes still represent the biggest risk component relative to the others. - Moderate Physical Certainty (mid share): Site/building conditions are somewhat knowable (e.g., condition, access, services, construction complexity), creating a moderate level of risk. - Low Lifestyle Certainty (smallest share): Lifestyle/amenity or “place experience” factors are least certain (e.g., neighborhood perception, livability, demand drivers tied to lifestyle), adding a smaller—but less predictable—risk portion. Interpretation: Overall risk is weighted toward planning/entitlement considerations, with physical factors secondary and lifestyle factors the least represented but more uncertain. 2) Upside (middle pie) Upside is where certainty translates into value creation potential: - Highest Planning Certainty (large share): The strongest upside comes from planning-related confidence—when the planning path is clear, the ability to execute and capture value is greatest. - High Physical Certainty (moderate-to-large share): Solid knowledge of the physical asset/site supports upside (e.g., deliverability, cost control, feasibility). - Moderate Lifestyle Certainty (moderate share): Lifestyle demand is a meaningful contributor to upside, but only moderately certain—suggesting upside exists, though it depends more on market sentiment and buyer preferences. Interpretation: Value potential is led by planning clarity, supported by physical deliverability, with lifestyle demand contributing but less reliably. 3) Typical Buyer Profiles (right panel) Based on that risk/upside mix, the likely buyers fall into three groups: 1. Long-Horizon Investors – Buyers comfortable holding through cycles and timelines, often prioritizing durable, long-term value. 2. Growth-Focused Buyers / Investors – Buyers seeking appreciation and execution-driven returns, typically attracted to clearer planning and feasible delivery. 3. Owner-Occupiers & Stability Investors – Buyers prioritizing predictability, usability, and steady outcomes (often more sensitive to lifestyle and day-to-day fit). Overall takeaway The chart suggests an opportunity where planning certainty is the main driver of both risk and upside. Physical factors are comparatively well understood, while lifestyle factors are less predictable. As a result, the opportunity appeals to a mix of long-term, growth-oriented, and stability-focused buyers, depending on their tolerance for planning and market-driven uncertainty. 4) In Conclusion (See Below) +++ This topic isn’t related to Feng Shui at all. I’m also not a Real Estate agent. I’m simply, like you, a property buyer who’s interested in property trends in SG. These three stages are very commonly used by many local Realty Agents to explain a property’s profit potential, if any.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

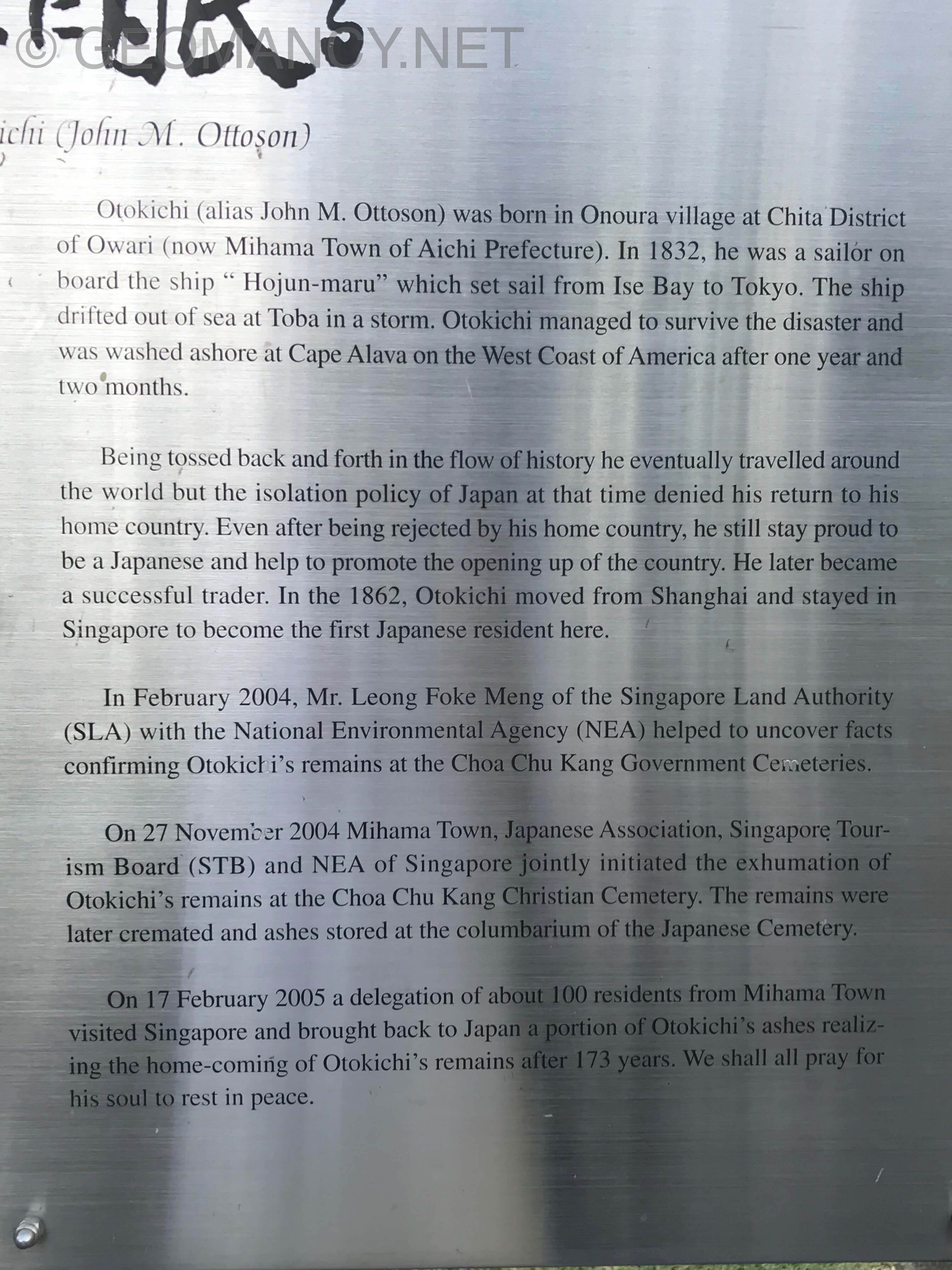

Related: Is a squarish or narrow layout better for an office unit What key factors should I consider Does this also apply to homes - Feng Shui for Business - FengShui.Geomancy.NetOtokichi (John M. Ottoson) Otokichi (alias John M. Ottoson) was born in Onoura village at Chita District of Owari (now Mihama Town of Aichi Prefecture). In 1832, he was a sailor on board the ship “Hojun-maru” which set sail from Ise Bay to Tokyo. The ship drifted out of sea at Toba in a storm. Otokichi managed to survive the disaster and was washed ashore at Cape Alava on the West Coast of America after one year and two months. Being tossed back and forth in the flow of history he eventually travelled around the world but the isolation policy of Japan at that time denied his return to his home country. Even after being rejected by his home country, he still stay proud to be a Japanese and help to promote the opening up of the country. He later became a successful trader. In the 1862, Otokichi moved from Shanghai and stayed in Singapore to become the first Japanese resident here. In February 2004, Mr. Leong Fook Meng of the Singapore Land Authority (SLA) with the National Environmental Agency (NEA) helped to uncover facts confirming Otokichi’s remains at the Choa Chu Kang Government Cemeteries. On 27 November 2004 Mihama Town, Japanese Association, Singapore Tourism Board (STB) and NEA of Singapore jointly initiated the exhumation of Otokichi’s remains at the Choa Chu Kang Christian Cemetery. The remains were later cremated and ashes stored at the columbarium of the Japanese Cemetery. On 17 February 2005 a delegation of about 100 residents from Mihama Town visited Singapore and brought back to Japan a portion of Otokichi’s ashes realizing the home-coming of Otokichi’s remains after 173 years. We shall all pray for his soul to rest in peace.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

The truth about annual Feng Shui products: what’s sold as tradition has become a highly profitable buying trap. What many people don’t realize: annual Feng Shui products are less about balance and more about selling fear. Annual Feng Shui products aren’t guidance they’re a carefully engineered sales cycle. Let’s call it what it is: the annual Feng Shui buying cycle has become a commercialized scam. Understanding the Commercial Side of Modern Feng Shui The Annual Feng Shui Money Trap: Why You’re Told to Buy for All Nine Sectors Every Year The Feng Shui Sales Machine: How Annual “Cures” Turn Advice into Retail Annual Feng Shui Products Explained: Nine Sectors, Endless Purchases Separating Authentic Feng Shui from Product-Driven Practices Feng Shui Without Forced Buying: What Clients Are Rarely Told Many Feng Shui shops deliberately push customers to buy new items year after year, making it seem like these purchases are unavoidable. The bigger the family, the more objects we’re told we need, filling our homes with products we never truly needed in the first place. Over time, this becomes a repeating cycle—almost like an addiction—where people feel they have to make an annual pilgrimage to these so‑called Feng Shui masters. Fear, superstition, and guilt are quietly used to pressure people into buying again and again. In the end, the real purpose becomes clear: generating super‑normal profits for the sellers, while ordinary people unknowingly become their victims. Recognizing this pattern is the first step toward breaking free from it. Behind the friendly advice lies a clear motive: to push customers into buying as many products as possible—one for each of the nine sectors of their home. This isn’t guidance; it’s systematic upselling disguised as tradition. If we want this cycle to end, it starts with us. Please spread the word: when people stop buying out of fear, the selling stops too.

Related: Is a squarish or narrow layout better for an office unit What key factors should I consider Does this also apply to homes - Feng Shui for Business - FengShui.Geomancy.NetOtokichi (John M. Ottoson) Otokichi (alias John M. Ottoson) was born in Onoura village at Chita District of Owari (now Mihama Town of Aichi Prefecture). In 1832, he was a sailor on board the ship “Hojun-maru” which set sail from Ise Bay to Tokyo. The ship drifted out of sea at Toba in a storm. Otokichi managed to survive the disaster and was washed ashore at Cape Alava on the West Coast of America after one year and two months. Being tossed back and forth in the flow of history he eventually travelled around the world but the isolation policy of Japan at that time denied his return to his home country. Even after being rejected by his home country, he still stay proud to be a Japanese and help to promote the opening up of the country. He later became a successful trader. In the 1862, Otokichi moved from Shanghai and stayed in Singapore to become the first Japanese resident here. In February 2004, Mr. Leong Fook Meng of the Singapore Land Authority (SLA) with the National Environmental Agency (NEA) helped to uncover facts confirming Otokichi’s remains at the Choa Chu Kang Government Cemeteries. On 27 November 2004 Mihama Town, Japanese Association, Singapore Tourism Board (STB) and NEA of Singapore jointly initiated the exhumation of Otokichi’s remains at the Choa Chu Kang Christian Cemetery. The remains were later cremated and ashes stored at the columbarium of the Japanese Cemetery. On 17 February 2005 a delegation of about 100 residents from Mihama Town visited Singapore and brought back to Japan a portion of Otokichi’s ashes realizing the home-coming of Otokichi’s remains after 173 years. We shall all pray for his soul to rest in peace.

- Last week

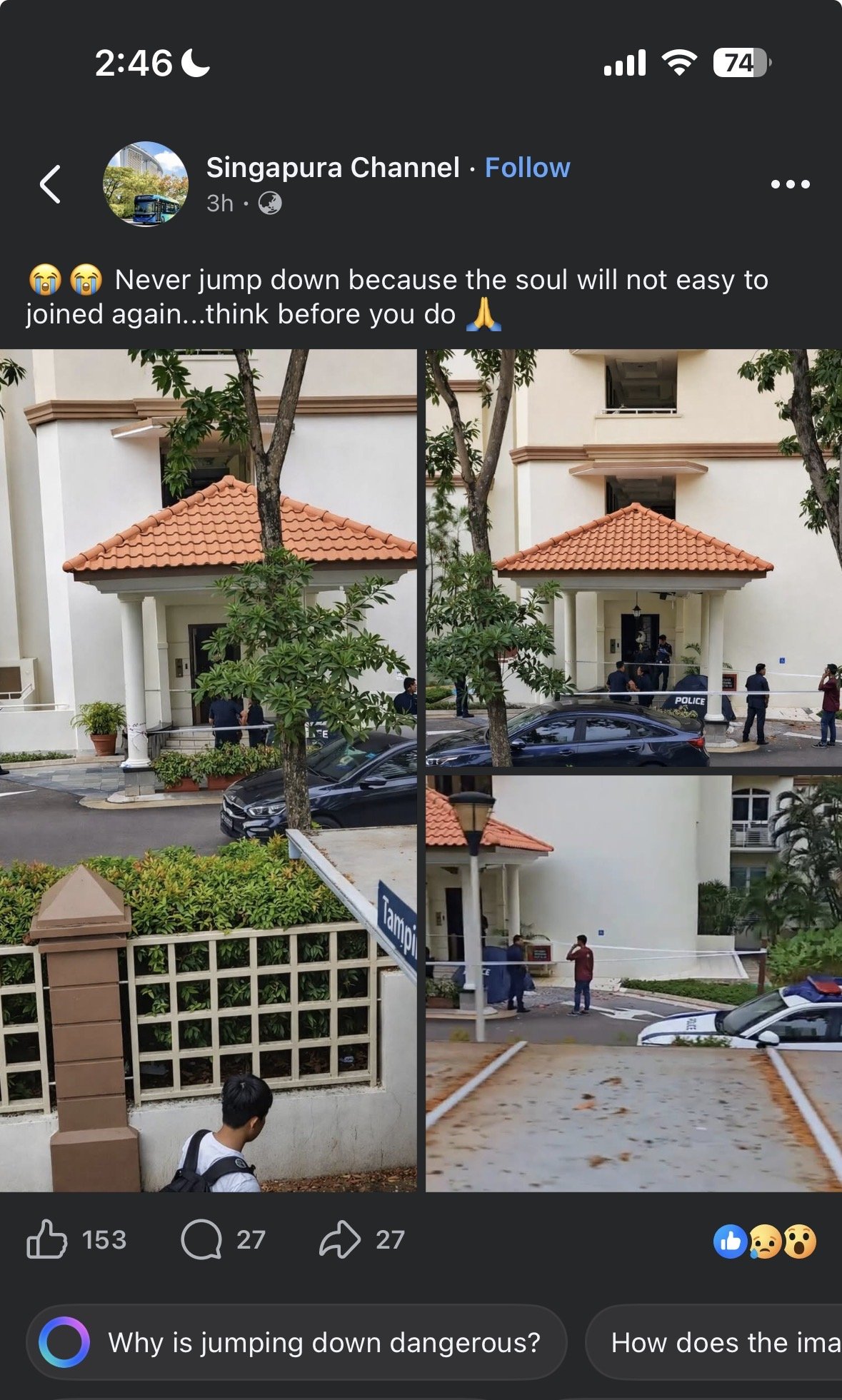

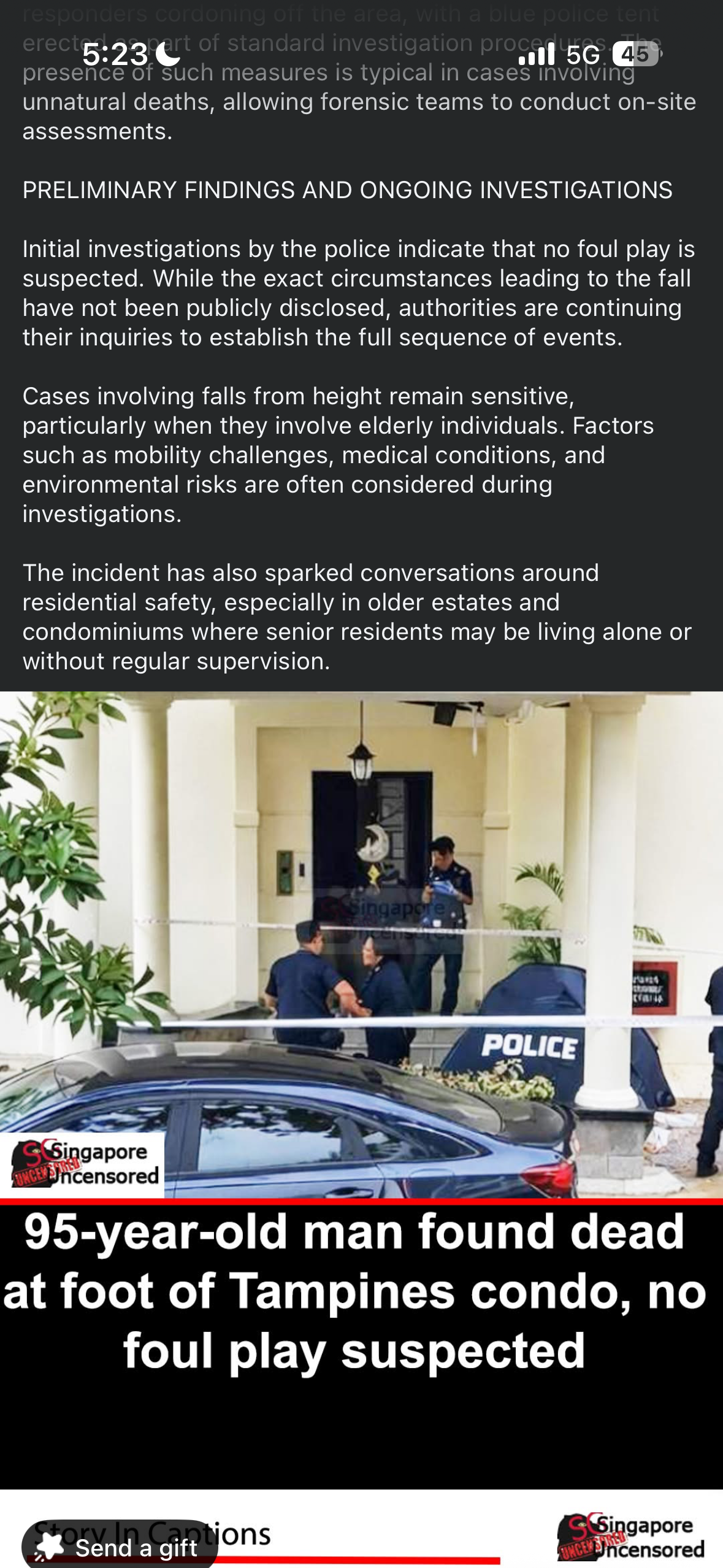

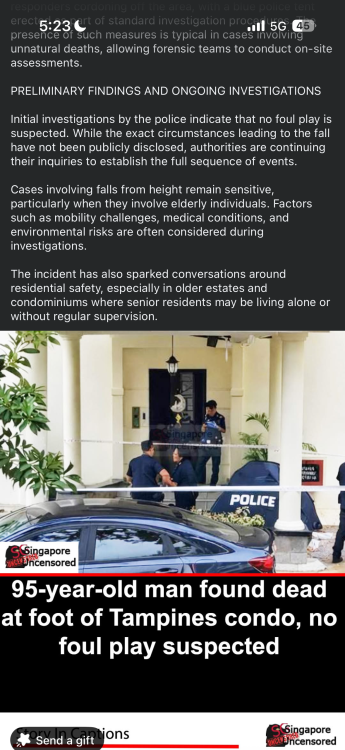

Around 10th April, suicide occurred at The Tropica condo…

How to access MCST accounts & sinking fund details in Singapore:- 1) The most reliable route: via the seller (current proprietor) In practice, MCST/managing agents usually release full packs only to subsidiary proprietors (owners). So ask the seller to obtain (or authorise release of) the following: Documents to request (latest available): - Audited financial statements (last 2–3 financial years) - Current year budget (and any mid-year revisions) - Statement of accounts / fund statements showing Management Fund vs Sinking Fund - A/R ageing report (arrears by aging bucket) - Schedule of contributions (maintenance + sinking rates, and any recent changes) - AGM/EGM minutes (past 2–3 years) - (If available) 10-year cyclical maintenance plan, condition surveys, lift reports Tip: Ask for the full AGM pack (notice, agenda, council report, financials, budgets, motions). It often contains 80% of what you need. 2) Through your conveyancing lawyer (as part of sale checks) Your lawyer can often raise requisitions / requests for: - Outstanding contributions on the unit - Confirmations relating to levies, by-laws, pending disputes (where obtainable) This won’t always replace full financials, but it helps confirm whether there are known arrears/levies/issues tied to the unit or project. 3) Directly from the managing agent (sometimes possible with authorisation) If the seller signs an authorisation letter (or forwards the request), the managing agent may provide the pack to you/your agent. How to interpret the accounts (what to look for) A) Separate the two “pots”: Management Fund vs Sinking Fund - Management Fund = day-to-day operating expenses (cleaning, security, landscaping, managing agent fees, utilities for common areas). - Sinking Fund = long-term/cyclical capital works (roof waterproofing, façade/spalling repairs, lift overhaul/replacement, repainting). Red flag: Sinking fund repeatedly used to plug operating shortfalls (or constant “transfers” to cover management deficits). That usually signals fees are set too low or cost control is weak. B) Balance sheet / fund position: “Do they actually have cash?” Focus on: - Bank balances / fixed deposits (not just “fund balance” on paper) - Any large payables (contractors unpaid) that will eat into cash soon - Whether sinking fund monies are kept properly (typically in MCST bank accounts/FDs) C) Income & expenditure: are costs stable and explainable? Look for: - Rising security/cleaning costs without explanation or re-tendering - One-off spikes (e.g., repairs) and whether they recur - Managing agent fees and any unusual “admin” line items Good sign: Regular tendering, clear notes explaining increases, and predictable operating costs. D) Arrears (A/R ageing): is cashflow at risk? In the A/R ageing report, check: - How much is >90 days overdue (more concerning than short delays) - Whether arrears are concentrated in a few units (common in small/boutique projects) - Whether there’s an allowance for doubtful debts (acknowledges collection risk) Red flags: Persistent high arrears, no improvement year-on-year, frequent council complaints about non-paying owners. E) Sinking fund adequacy: “Is it enough for what’s coming?” There’s no single perfect benchmark, so triangulate: 1) Sinking fund balance per unit (and per sqm/share value if available) 2) Building age and what’s typically due soon: - ~10–15 years: repainting, waterproofing, pumps - ~15–25 years: façade/spalling, major M&E, lifts 3) AGM minutes / maintenance plan: any known upcoming big-ticket works 4) Evidence of a funding plan: raised rates early vs special levies Red flag: Major works discussed in minutes + low sinking fund + no approved plan = higher chance of special levy. F) Budget vs actuals: are they routinely under-budgeting? Check if: - Actual expenses exceed budget every year (suggests fees may rise or levies appear) - Budget assumes “one-off savings” that don’t materialise --- Fast “go/no-go” questions to ask (and verify in documents) 1) Any approved/anticipated special levy in the next 12–24 months? 2) What major works are planned (roof, façade, lifts), and how will they be funded? 3) What’s the current sinking fund balance and monthly contribution rate? 4) How much is in arrears >90 days, and is enforcement ongoing? 5) Any ongoing disputes/litigation, contractor issues, or repeated defects noted in AGM/EGM minutes? If you share the condo name and approximate age (TOP year) and whether it has lifts/pool/basement, I can tell you what “normal” sinking-fund strength looks like for that profile and the most likely capex items to sanity-check. MCST accounts: typical red flags (boutique condos) 1) Operating deficits / “running on fumes” - Management Fund shows repeated deficits (actual expenses > contributions) across multiple years. - Reliance on one-off items (late interest, “other income”) to appear balanced. 2) Sinking fund used to pay day-to-day bills - Frequent transfers from Sinking Fund to Management Fund to cover operating shortfalls. - Notes/minutes suggest “temporary transfer” that keeps recurring. 3) Low cash despite “healthy” fund balances - Fund statements look fine, but bank balances/FDs are low (cash tied up, or large payables pending). - Large trade payables (contractors unpaid) or ballooning accruals. 4) High arrears (A/R ageing) and weak enforcement - Meaningful amount >90 days overdue, persisting year-on-year. - Arrears concentrated in a few units (in small developments this is a big risk). - No/low allowance for doubtful debts, despite chronic arrears. 5) Underbudgeting as a pattern - “Budget vs actual” shows consistent overspend with no corrective fee adjustments. - Budgets assume unrealistic savings (“to be tendered lower”) that never materialise. 6) Cost lines that jump without explanation or tender - Security/cleaning/landscaping costs rising sharply without re-tendering or explanation in council/AGM notes. - Vague headings (e.g., “General expenses”, “Admin charges”) that are large or growing. 7) Insurance or compliance gaps - Unclear/insufficient building insurance coverage, or repeated mentions of compliance issues (fire safety, lift certifications) with no closure. --- Sinking fund: typical red flags 8) Sinking fund clearly not sized for building age and assets - Older boutique condo with lifts/basement/pumps but thin sinking fund and low monthly sinking contributions. - No evidence of a cyclical maintenance plan or condition surveys guiding contributions. 9) Big-ticket works discussed but no funding plan - AGM/EGM minutes mention upcoming façade/spalling, roof waterproofing, lift replacement, repainting, but there’s no approved scope/tender timeline and no plan besides “may call special levy”. 10) Frequent special levies (or “soft” levies) - Repeated special levies, or ad-hoc “top-ups” framed as exceptional but occurring often. - Signals contributions are structurally too low or maintenance is reactive. 11) Deferred maintenance - Minutes repeatedly say “defer,” “monitor,” “patch repair,” “temporary fix,” especially for leaks/spalling/lifts. - Common-area condition aligns with this (stains, seepage, patchy repainting). 12) Concentration risk shows up in decisions - In boutique MCSTs, a few owners can block fee increases; minutes show repeated failed motions to raise contributions despite known upcoming works. --- Quick “walk-away / price-in” triggers - Sinking-to-management transfers + low cash + known major works pending - High >90-day arrears with no improvement - Major works imminent (lifts/façade/waterproofing) and the MCST is clearly not provisionedStrong resale demand for boutique condos usually comes from a mix of scarcity + livability + micro-location. The main drivers: 1) Scarcity (low supply, hard to replicate) - Few units means fewer resale listings at any time, which can support pricing when a desirable unit appears. - Many are on small land parcels in mature estates where new comparable supply is limited. 2) Micro-location advantages (what buyers pay for) - Walkability to MRT, amenities, parks, and lifestyle nodes (e.g., Katong/Orchard/Robertson Quay). - Proximity to “sticky” demand anchors like good schools, medical hubs (Novena), CBD/fringe job clusters, or established expat enclaves. 3) Tenure and long-hold appeal (often freehold) - Freehold reduces “lease decay” concerns and widens the pool of long-term/legacy buyers. - Even for non-legacy buyers, tenure can be a psychological “safety factor” in resale negotiations. 4) Liveability: privacy, noise, and daily convenience - Fewer neighbours, less crowding at lifts/pool/gyms, and generally quieter common areas. - Suits owner-occupiers (privacy-focused) and many expats (quiet, low-density living). 5) Unit attributes that are hard to find in mass projects - Efficient layouts (less wasted corridor/bay window space), better room proportions. - Sometimes larger internal areas for the same price quantum in older boutique stock. - Better orientation (less facing into another block), higher privacy. 6) “Quantum” affordability for prime addresses - Even if $psf is high, a smaller boutique unit can have a more reachable total price than larger units in big prime developments—widening the buyer pool. 7) Strong rental market spillover → resale support - In expat-heavy locations, stable rental demand helps owners hold through cycles and gives buyers confidence on exit options. 8) Building management and upkeep (when done well) - A proactive MCST, healthy sinking fund, and well-maintained façade/common areas reduce buyer hesitation. - Conversely, poor upkeep can kill demand quickly—so this factor is decisive. 9) Limited “internal competition” - In mega-developments, many similar units compete with each other at resale. - In boutiques, each unit can feel more unique (stack, view, layout), reducing direct price undercutting. Typical risks with boutique condos (and why they matter): - Lower liquidity / smaller buyer pool: Fewer transactions and a more niche audience can mean longer selling times and less certainty on exit timing, especially in weaker markets. - Harder price discovery & valuation: With limited recent caveats, banks/valuers have fewer comparables, which can lead to more conservative valuations and larger gaps between asking and achievable prices. - Higher maintenance fees per unit: Costs for security, lifts, façade, pumps, pools, etc. are spread across fewer owners, so monthly MCST fees can be higher, and special levies can sting. - Facilities trade-off: Many boutique projects have minimal or no full facilities, which can reduce appeal for family buyers and make them less competitive versus nearby full-facility condos at the same price point. - Management/MCST concentration risk: In small developments, a few owners can heavily influence decisions. Poor governance can lead to under-maintenance, disputes, or weak financial planning. - Maintenance and aging risk (especially older freehold boutiques): Freehold doesn’t mean “maintenance-free.” Older buildings may face costly cyclical works (waterproofing, spalling concrete, lift replacement). - Developer/build quality variability: Some boutique condos are built by smaller developers; quality and after-sales support can be uneven, increasing defect and long-term upkeep risk. - Rental demand can be narrower: If the layout is quirky, the unit is small but expensive, or the project lacks facilities/parking, it may appeal to fewer tenants, affecting holding power. - En-bloc assumptions may not play out: Small freehold sites can be en-bloc targets, but success depends on plot ratio, buyer interest, consensus among owners, and timing—so don’t overpay for “en-bloc potential.” A practical due‑diligence checklist tailored to boutique condos (where small size makes MCST finances, maintenance planning, and resale liquidity more sensitive). 1) Transaction & price reality (don’t rely on asking prices) - URA caveats (project + stack if possible): last 1–3 years’ resale prices, volume, and days-on-market proxies (how often units transact). - Profit/loss pattern: how many resales are profitable vs loss-making and at what holding periods. - Bank valuation sensitivity: ask your agent/banker if recent caveats are thin—thin data can mean conservative valuations. 2) MCST financial health (most important for boutique) Request the latest: - Audited financial statements (2–3 years) - Budget for current year - A/R ageing report (arrears; who isn’t paying) - Sinking fund balance + how it’s invested/held Check for: - Low sinking fund per unit relative to building age/facilities - High arrears (cashflow risk), frequent special levies, or repeated “one-off” top-ups 3) Upcoming major works (capex) and hidden liabilities Ask for: - 10-year cyclical maintenance plan (if any) - Latest condition surveys (façade, roof waterproofing, M&E) - Lift maintenance records and replacement timeline - Fire safety / SCDF notices, if any Red flags: - Big-ticket items due soon (lift replacement, spalling repairs, waterproofing) with no clear funding plan 4) Meeting minutes: disputes, defects, and governance Read: - AGM/EGM minutes (past 2–3 years) and council meeting notes if available Look for: - Owner factions, contractor disputes, litigation threats - Repeated complaints about leaks, facade issues, pests, noise, short-term stays - “Deferred works” due to lack of funds 5) Building condition inspection (common areas tell the truth) On-site checks (day + night if possible): - Façade: cracks, spalling, staining; roof/upper-level water marks - Basement/driveway: water seepage, pump rooms, mould - Corridors/stairwells: smells, peeling paint, poor lighting - Facilities (if any): pool tiles, filtration, gym equipment condition - Noise/traffic exposure and privacy (boutique blocks can be close to roads) 6) Unit-specific technical checks - Orientation/heat/noise (west sun, road/frontage, rubbish chute proximity) - Water pressure & drainage, especially for older projects - Signs of leakage (ceilings, window frames, bathrooms) - Aircon ledge / piping condition - Renovation history: was hacking/structural work approved? 7) Rules that affect livability and rental Obtain house rules/by-laws: - Rental restrictions (min lease period, registration requirements) - Renovation hours, pet rules, parking allocation, visitor parking - Any “no Airbnb/short-stay” enforcement posture (good for own-stay; can affect some investors) 8) Resident/owner mix (stability vs churn) - Ask/observe: % rented out, tenant profile, turnover - High investor concentration can mean more wear-and-tear and price competition on exit; high owner-occupier share often supports upkeep and community—project dependent. 9) Developer/build quality and warranty history - Developer track record across other projects - For newer condos: defects history, rectification responsiveness, any recurring issues (waterproofing, façade, M&E) 10) Legal/title checks (with your lawyer) - Tenure & remaining lease (if leasehold) - Caveats/encumbrances on the unit - Any known MCST or contractor litigation - Confirm the unit’s share value (affects maintenance fee apportionment) and carpark title (strata vs common)